Overview

- Russia’s invasion of Ukraine has created a humanitarian crisis, driven commodity prices and government bond yields sharply higher and raised concerns about the sustainability of the global economic recovery. It is too early to assess the ultimate impact with any certainty, but it likely means investors will have to contend with continued high inflation, supply disruptions, slower growth and higher market volatility in 2022.

- Sharply higher energy and other commodity prices are driving inflation up and, together with tighter financial conditions, are likely to weigh on global growth. The severity of the impact will depend on how high commodity prices rise, for how long and, importantly, how consumers, governments and central banks respond. The EU has indicated it is likely to allow countries continued fiscal flexibility to offset the shock, and there are discussions about EU joint bond issuance to boost defence spending and diversify energy supply. Further fiscal shielding measures by other countries are likely to be announced in the coming months.

- There is likely to be large performance dispersion at a country, sector and company level. Europe and UK growth supported by activist fiscal policy, strong household and corporate balance sheets. As during the Covid-19 pandemic, performance will likely vary widely in the current economic environment. Sectors most sensitive to high energy and other commodity prices such as autos, aviation, shipping, chemicals, building materials, basic metals and food & beverage are likely to most affected. Second round effects through hits to disposable income and higher costs are likely to weigh on discretionary spending in areas such as hospitality, leisure and big ticket durable items such as autos in particular. Most companies in the healthcare, business services, financial services and technology sectors, however, are likely to be less affected.

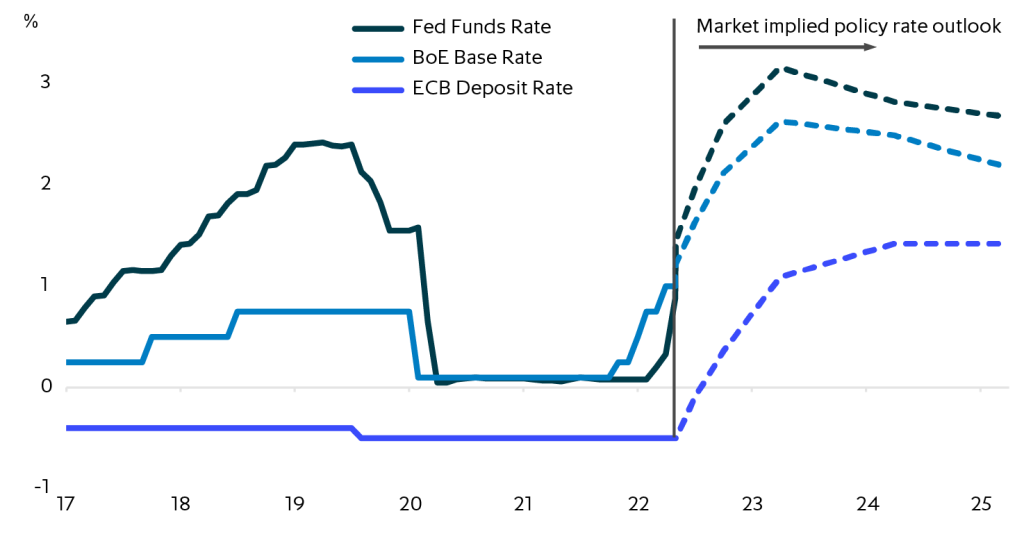

- Inflation and interest rates to rise quickly in H1 2022, but should start to stabilise H2. With inflation expected to rise at a fast pace through H1 2022, markets anticipate the Fed, BoE and ECB will front load rate hikes, with the Fed to raise its target rate to around 2.75% by the end of this year, the BoE to around 2.25% and the ECB to around 0.50%. However, if inflation begins to fall and growth slows in H2 as we expect, policy rate expectations and market rates may also start to moderate.

- Investor allocation likely to become more selective, alternatives well positioned. From an asset allocation point of view, strategies that provide inflation and interest rate hedges, downside protection and predictable cashflows, are likely to remain in strong demand. Strategies with medium to long-term investment horizons that are able to look through economic and market volatility and benefit from market dislocation are also likely to outperform in this environment in our view.

Front-loaded policy rate normalisation underway

A shock to the system

Russia’s invasion of Ukraine has created a devastating humanitarian crisis, driven up energy and other commodity prices, pushed government bond yields sharply higher and led to questions about the sustainability of the global economic recovery. The scale of the commodity price increases has caused inflation – already high – to rise to levels not seen in many countries for over forty years, and substantially accelerated investors expected timeline for central bank policy normalisation.

The commodity price shock and continued supply chain bottlenecks will likely add pressure on the margins of companies in commodity price and supply chain sensitive sectors such as aviation, autos, food and packaging, chemicals and other heavy industries. Reductions in disposable income will likely weigh on consumer discretionary spending. Companies in the healthcare, technology, business and financial services sectors and those with dominant market positions and pricing power will likely continue to perform well. Bottom up analysis will be critical in this environment. Growth and earnings are likely to slow quite sharply in 2022, with fossil fuel intensive sectors and sectors dependent on consumer discretionary spending particularly vulnerable.

Despite these headwinds, strong household, corporate and financial sector balance sheets, together with high levels of household savings, low unemployment and supportive fiscal policy will provide offsets.

Therefore, assuming no substantial further escalation of the war or a sustained large-scale cut-off of Russia’s natural gas exports, we think the global economic expansion will extend – albeit at a more moderate pace and with wide country and sector performance dispersion – into 2023.

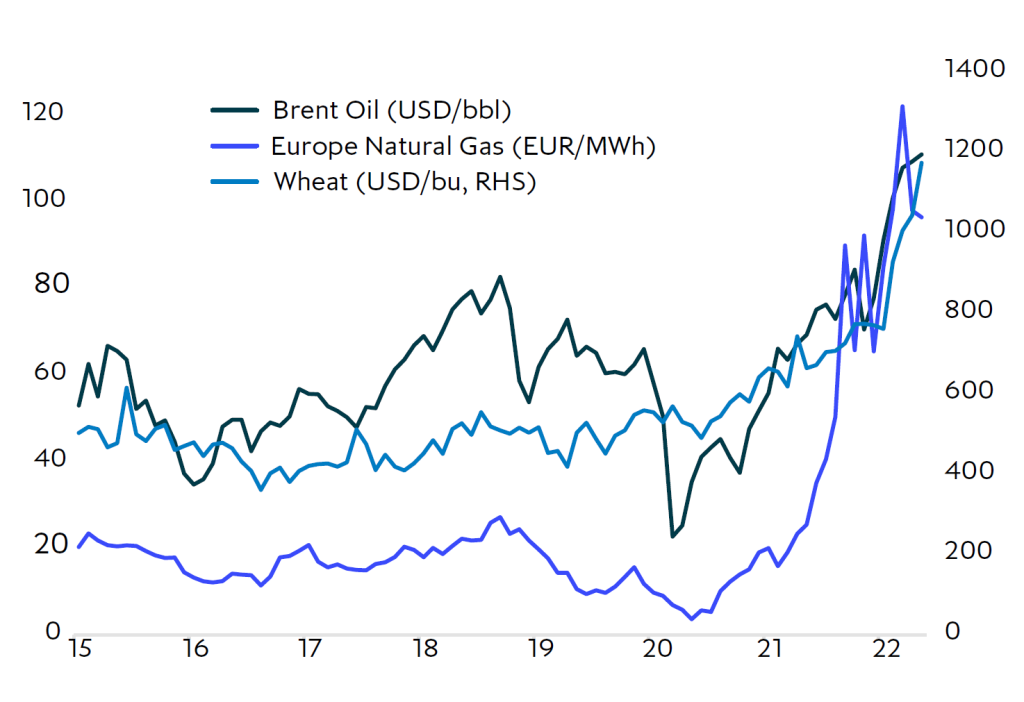

The largest energy price shock since the 1970s

Russia’s invasion of Ukraine and the economic sanctions imposed by US, UK and EU have driven energy and other commodity prices sharply higher, added to global supply chain bottlenecks already under severe strain from China’s zero Covid policies, pushed inflation higher and helped drive government bond yields and market rates back to (and in some cases above) pre-pandemic levels. The main transmission mechanism of the war to the world economy is through higher energy prices (and, to a lesser extent, other commodities) and further disruptions to already stretched global supply chains. How severe the economic shock ultimately proves to be will depend on how long energy prices stay at elevated levels; whether Russia materially reduces its natural gas exports to Europe on a sustained basis; how prolonged and severe supply chain disruptions are; and how companies, consumers and governments react to the shock.

Commodity price shock

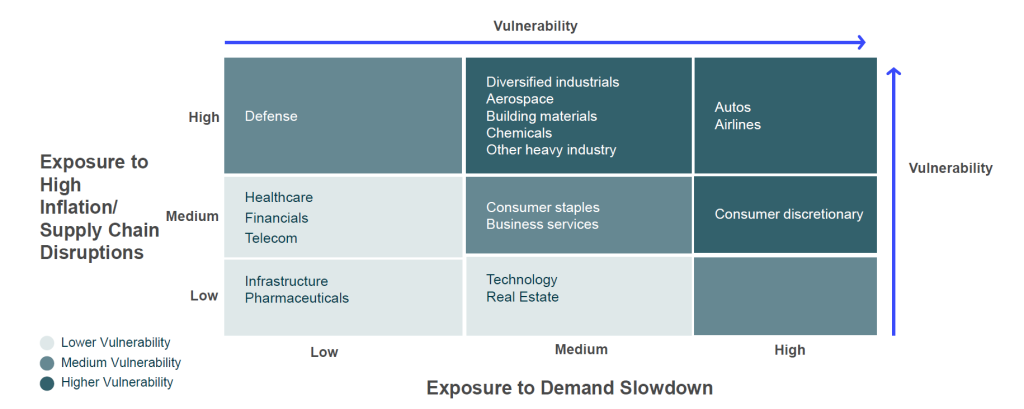

Weaker growth ahead: Sector and country performance will vary widely

While a weakening in headline GDP and earnings growth rates appears inevitable, unlike the 2008/09 global financial crisis, the impact is likely to vary widely at a sector and country level. Fossil fuel and other commodity- intensive sectors such as aviation, shipping, chemicals, cement, steel and basic metals, paper, packaging and food & beverage are likely to see the most direct negative impact. Sectors exposed to second round negative effects caused by reductions in household disposable income and higher input costs, include hospitality, leisure and big ticket consumer discretionary items. Autos and globally integrated industrials are likely most vulnerable to continued supply chain disruptions. On the other end of the spectrum, companies in the healthcare, business services, technology, infrastructure, financial and real estate services sectors are likely to see more limited impact.

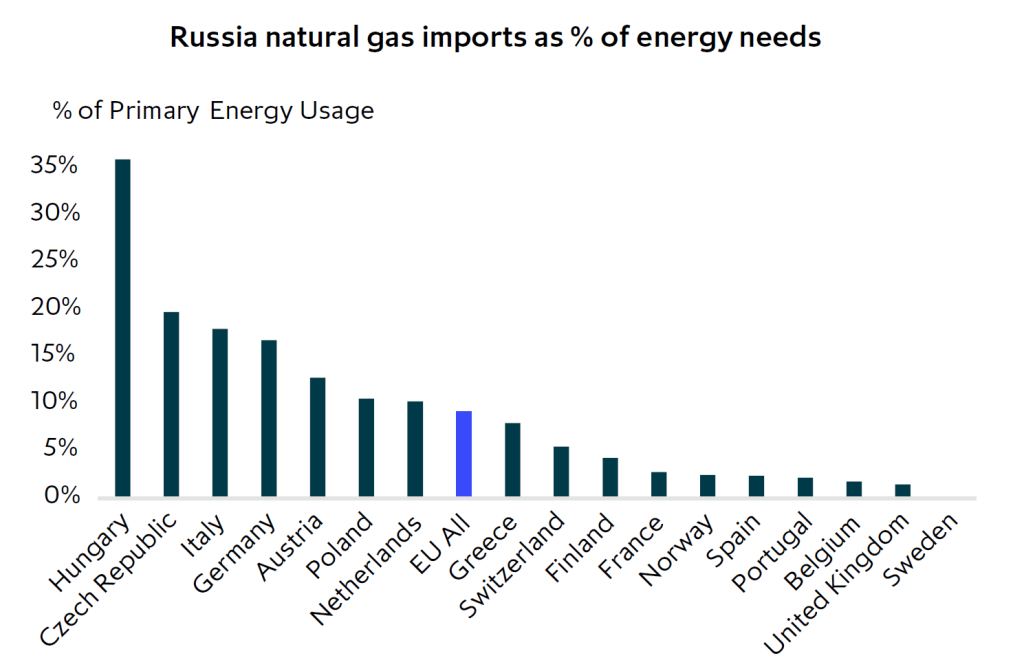

At a country level, eastern Europe, Germany and Italy are most directly exposed to a potential cut-off or reduction in Russia natural gas supplies. However, most of the rest of western Europe and the world have more limited direct exposure (see chart below). Reductions in oil and coal sourced from Russia will be easier to replace than natural gas given multiple alternative sources and more flexible delivery infrastructure.

Germany is especially affected by higher energy prices and supply chain issues due to its high exposure to energy intensive heavy industry and supply chain sensitive manufacturing, particularly the auto sector. The high weighting of these sectors in Germany’s economic mix raises the risk headline GDP dips into negative territory later this year. We anticipate that the weakening, however, will be very sector specific and will recover as global industrial supply chain bottlenecks are gradually resolved.

Sector vulnerability to high inflation, supply disruptions and demand risks varies widely

Dependence on Russia natural gas imports

Calculated as Russia share of natural gas imports as percent of natural gas share of

primary energy usage

All countries will likely see a slowdown in consumer discretionary spending as higher energy and food costs cut into disposable income. However, most countries in Europe have acted to dampen the impact on consumers through energy tax cuts, subsidies, loans, cash payments and other measures, reducing the likelihood of a full blown Europe-wide recession.

After dragging its heels initially, the UK government also recently announced substantive measures to support households, bringing total proposed support spending to around £37bn, equivalent to around 1.7% of GDP. More fiscal support measures are likely.

In the US, so far, re-opening demand for services and the spending of pent up pandemic savings have kept private consumption ticking over at a healthy pace. Tighter monetary policy and sharply higher gasoline, food prices and energy bills, however, will likely weigh on spending in the coming quarters. Most forecasts assume that growth momentum from economic re-opening will offset these drags, with the consensus forecasting US GDP will grow by 2.8% in 2022 and 2.2% in 2023 and the IMF in its April World Economic Outlook (see table below) even more bullish. Although these forecasts are likely optimistic, equally, the strength of consumer, corporate and bank balance sheets coming into 2022 makes a sustained broad- based economic slowdown of the type experienced in 2008/09 much less likely in our view.

Outside of the large developed economies, the outlook is very mixed. Oil and other commodity net exporters will benefit from the rise in prices. However, as we have recently seen in in Sri Lanka, a number of emerging markets with high dependence on food and fuel imports and high US dollar debt burdens are increasingly at risk of social unrest and potential fiscal and sovereign debt stress.

IMF GDP forecasts – downward revisions ahead

| % | 2021 | 2022F | 2023F | 2024F |

|---|---|---|---|---|

| US | 5.7 | 3.7 | 2.3 | 1.4 |

| UK | 7.4 | 3.7 | 1.2 | 1.4 |

| Eurozone | 5.3 | 2.8 | 2.3 | 1.8 |

| –France | 7.0 | 2.9 | 1.4 | 1.5 |

| –Germany | 2.8 | 2.1 | 2.7 | 1.5 |

| –Italy | 6.6 | 2.3 | 1.7 | 1.2 |

| –Spain | 5.2 | 4.8 | 3.3 | 3.1 |

| Japan | 1.6 | 2.4 | 2.3 | 0.8 |

| China | 8.1 | 4.4 | 5.1 | 5.0 |

| World | 5.8 | 3.5 | 3.1 | 2.8 |

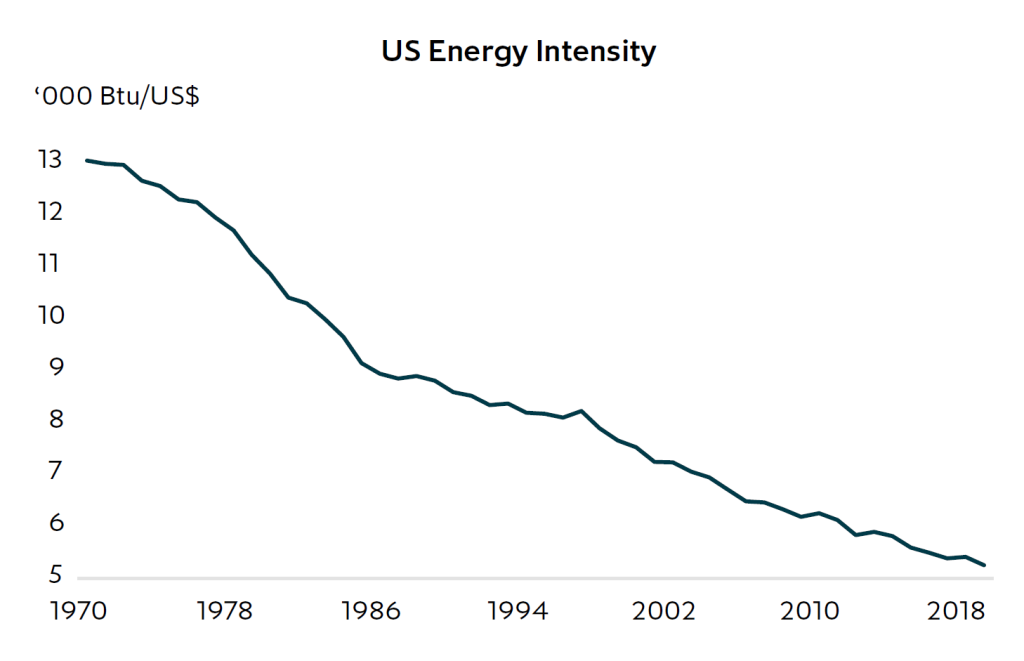

Fossil fuel intensity has declined – but it still matters

The world economy has become substantially less energy dependent than it was in the 1970s when the global economy was last hit by such a large energy price shock. US energy intensity estimated to have halved since the 1980s, with similar large drops in the energy intensity of growth in most of the developed world. However, fossil fuels are still a critical input to economic growth for most countries. Sustained higher prices, to the extent they are not offset by government policy, will take their toll on non-energy producing segments of economies by reducing consumers’ real spending power, raising input costs and acting as a general brake on domestic demand. Gauging the exact magnitude of the impact is extremely difficult given the multiple transmission mechanisms and varying sensitivities.

To give a sense of potential impact, Fed Chairman Powell in recent testimony said a rough rule of thumb is that a $10 increase in the price of a barrel of oil leads to a 0.2 percent increase in US inflation and a 0.1 percent hit to growth. The ECB has estimated that every 10% rise in the oil price in euro terms increases Eurozone inflation by 0.1-0.2 percentage points and that a 10% reduction in gas usage would reduce Eurozone output by around 0.7%.

Fossil fuel intensity half the level of the 1980s

High inflation + high interest rates + quantitative tightening = high market volatility

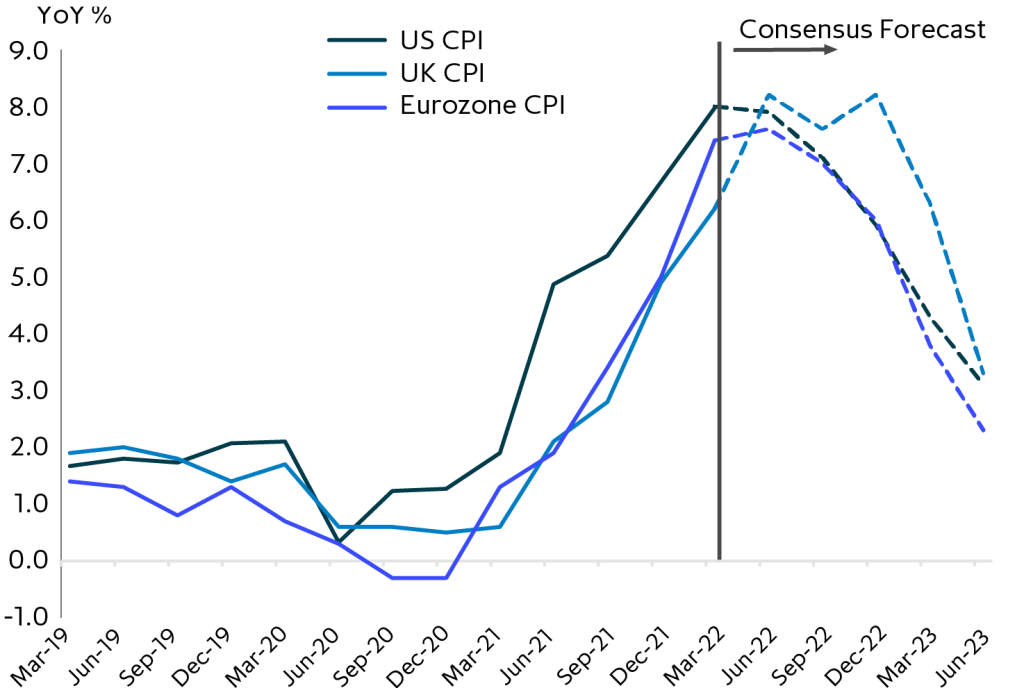

Inflation, already high due to supply and demand distortions caused by the Covid-19 pandemic and China’s zero Covid policies, has risen to levels not seen in many countries since the 1980s as higher energy and other commodities add to the price pressure. Although headline inflation rates in most countries are likely at or near their peaks as energy prices stabilise and supply chain bottlenecks slowly start to ease (the UK is an exception, with a scheduled increase in the cap on household energy prices expected to push CPI higher again in October), signs inflation is broadening into non-commodity related sectors has caused central banks to become more aggressive in trying to pre-empt a potential “un-anchoring” of long-term inflation expectations and a feared self-reinforcing wage-price spiral.

Inflation to start to fall in H2 2022

Central banks trying to pre-empt inflation expectations

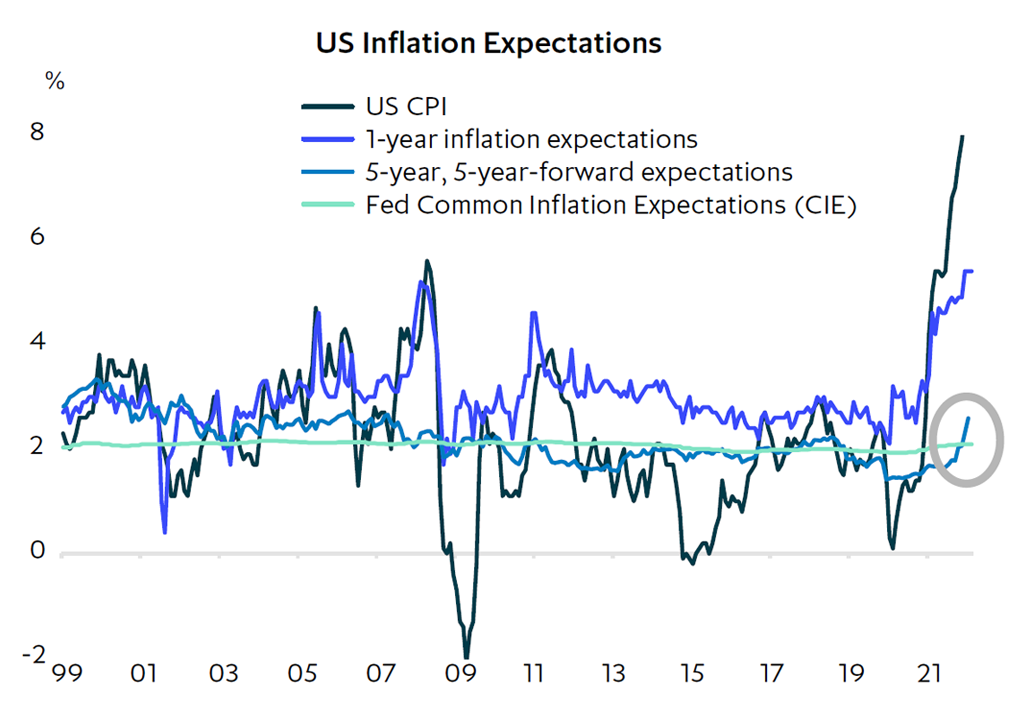

One of the main reasons for the wide ranging views on just how high central bank policy rates need to go is varying views on how sticky long-term inflation expectations are. Because current circumstances are unique and there is limited quality data on historical instances of an un-anchoring of long term inflation expectations, the truth is nobody knows how aggressively rates need to rise to keep them tethered. While short term inflation expectations have increased (for good reason), so far most measures of longer-term inflation expectations have remained well anchored. The calculation the BoE, the Fed and, more recently, the ECB appear to be taking is that near term inflation risks are higher than recession risks and therefore they are guiding markets to expect a front-loading of rate hikes to head off a potential rise in long term inflation expectations. In our view this calculus may start to shift later this year as growth and inflation start to fall more quickly, but until then the focus is likely to remain on inflation fighting.

Stable long term inflation expectations

A bumpy ride ahead

As the chart on the front page shows, higher inflation prints and – importantly – central banks reaction to them, has led to quite a dramatic shift in market interest rate expectations. Swaps markets at the time of writing imply that US, UK and Eurozone policy rates will normalise quickly, increasing by 325bp, 275bp and 200bp over the next year from their pandemic lows respectively. Quantitative easing programs are also now expected to be rolled back more rapidly than previously expected, with the BoE already in the process of reducing its balance sheet, the Fed starting in June and ECB indicating it is likely to start in July. Slower economic growth and tighter monetary policy are likely to pressure valuations and keep market volatility high through the rest of 2022 and into 2023.

Offsetting factors: Not all doom and gloom

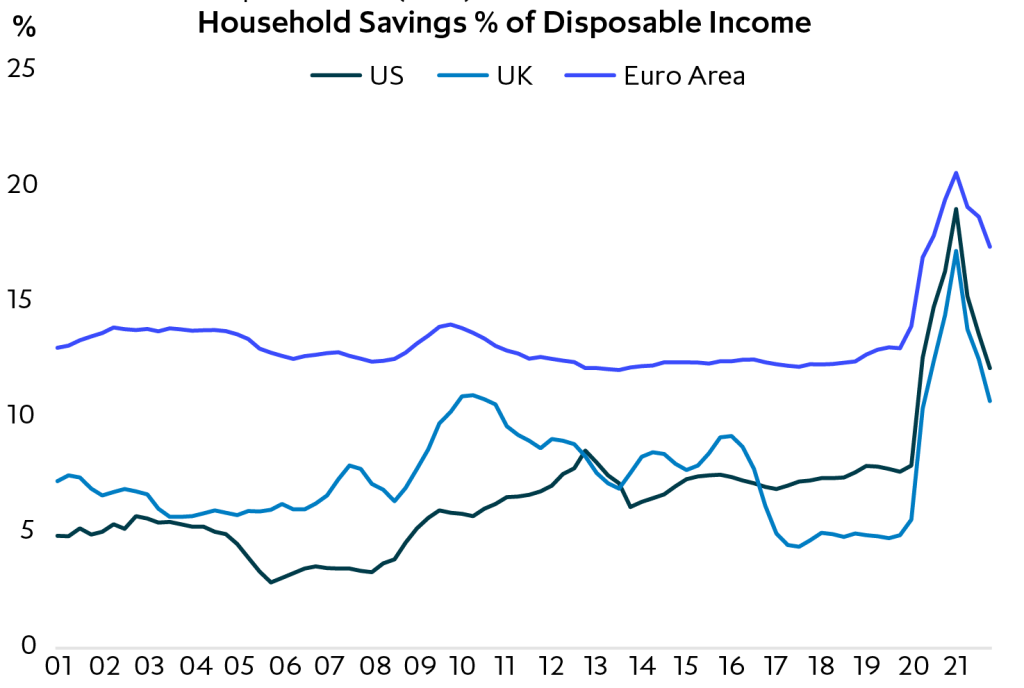

It is not all doom and gloom, however. There are a number of factors that should help to cushion economies from the blowback from the war in the Ukraine. The first is the substantial build-up of household savings and rise in net worth during the Covid-19 pandemic, with US, UK and EU household savings estimated at around 8%, 9% and 15% of disposable income respectively and house prices and most other asset prices well above pre-pandemic levels.

Household balance sheets are strong

While only a portion of savings are likely to be spent, the build-up provides consumers with short-term buffers against higher energy and other costs. Related to this, consumers come into the current difficult period with some of the strongest balance sheets in over twenty years.

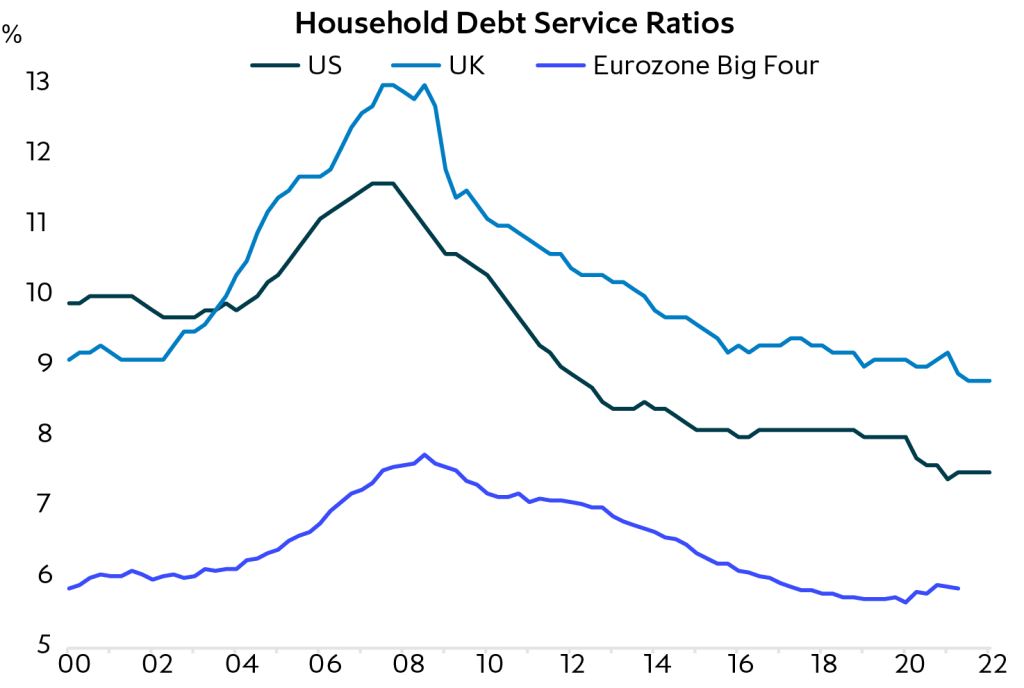

On BIS calculations, household debt service ratios at the end of 2021 in the US, Eurozone and the UK at their lowest levels since at least 2000 and substantially below the peak levels reached in the run-up to the 2008 global financial crisis.

Savings buffers still large

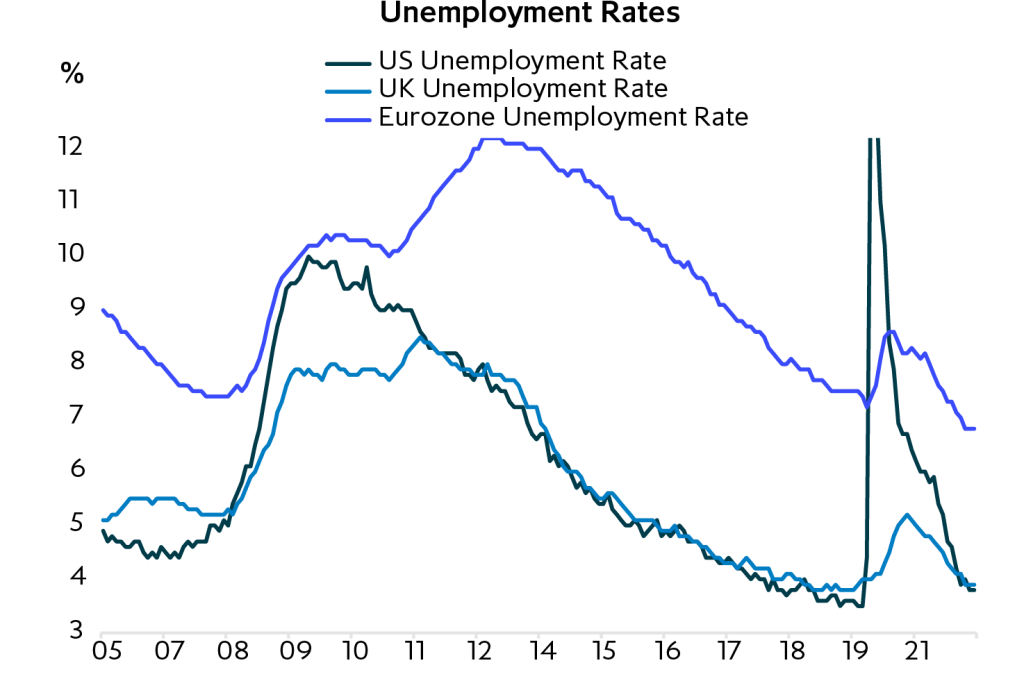

Job markets are also strong, with unemployment rates in the US and UK close to pre-Covid lows and the unemployment rate in the Eurozone its lowest on record. Tight employment markets have pushed up wage growth. While central banks have tended to focus on the risks higher wage growth pose to longer term inflation stability, the increases – which have been focused primarily at the lower end of the income scale – are having the positive effect of helping to partially offset the impact of higher energy and food prices on household budgets.

Unemployment is low

As we saw during the pandemic, when needed, governments have become nimbler at using fiscal policy to offset economic shocks. For example, Europe is expected to extend the suspension its fiscal rules on government debt and deficits to provide countries the flexibility to support their economies during the current cost of living crisis.

Already a number of governments in Europe have acted to shield households from higher energy costs through varying combinations of energy tax cuts, subsidies, direct payments and price caps. There are also discussions about potential EU joint bond issuance to boost defence spending and diversify energy supplies and reports the ECB is working on a new crisis financing tool to backstop against potential debt market stress caused by external shocks.

More announcements on fiscal support packages to protect households from the energy and food price shock are likely in the coming months. Depending on the size and scope of the packages of course, they should help support confidence and consumer spending.

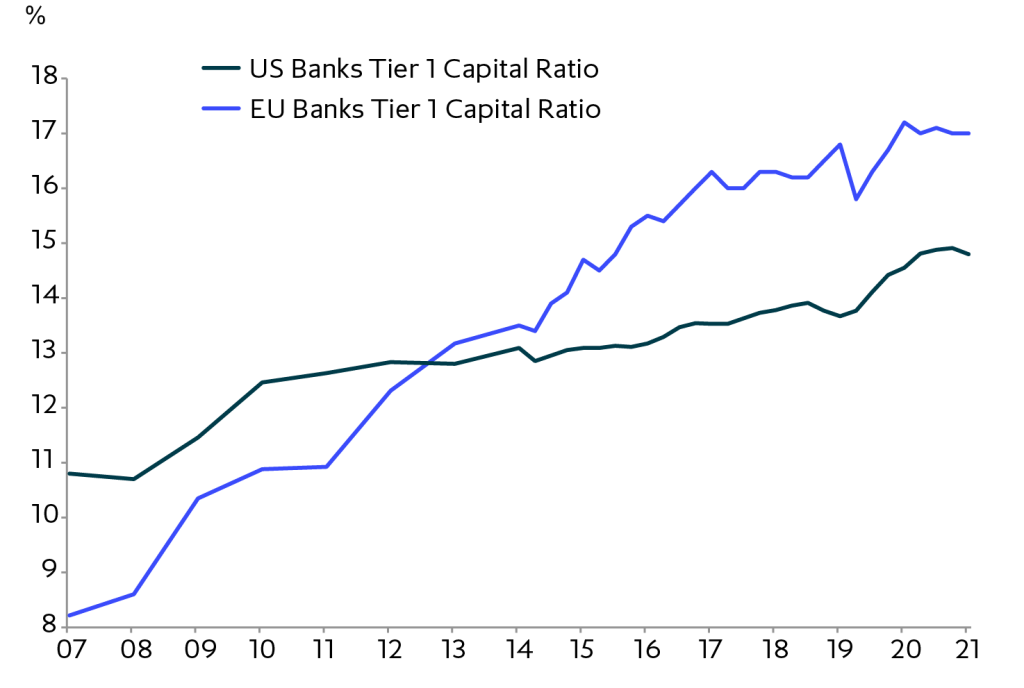

Finally, and perhaps most importantly, banking systems are much stronger and are much better regulated now than they were in the period running up to the 2008/09 global financial crisis, reducing the risk of a systemic financial crisis. Banks tier one capital ratios are now substantially higher than they were in 2008 and, together with regular stress tests, mean that the risk of a repeat of the self-perpetuating global credit and liquidity withdrawal that hit all sectors indiscriminately during the 2008/09 period is unlikely.

Bank balance sheets are strong

Investment Implications

Therefore, similar to the situation during the Covid-19 pandemic, careful sector selection and bottom-up company analysis should allow investors with medium to long-term investment horizons to continue to find interesting and rewarding investment opportunities.

From an asset allocation point of view, strategies that provide inflation and interest rate hedges, downside protection, predictable cashflows and can take advantage of dislocation, are likely to remain in strong demand.

Companies in sectors benefiting from longer-term structural tailwinds such as healthcare and biosciences, technology and digitisation, logistics, infrastructure and green transition as well as the business and financial services that support them are likely – at a broad level – to outperform in this more challenging environment. Opportunities will also likely emerge in the more negatively affected sectors as stronger, well managed and financed companies take advantage of market dislocation to increase market share and long term pricing power.