Economic and Private Markets Update from our Head of Economic and Investment Research, Nick Brooks

In this short video, Nick considers three key questions: Will economies face a hard, soft, no landing or something else? When will inflation and interest rates fall? What does this mean for private market investors?

In brief

- “Bumpy” economic landings ahead

- Deep recessions are likely to be avoided

- Wide performance dispersion at country, sector and company level

- Consumer discretionary, heavy industry and other cyclical sectors most at risk

- Companies in less cyclical sectors with structural tailwinds to outperform

- The price of more resilient growth is continued elevated inflation, and interest rates having to stay higher for longer

- Asset allocation implications

Watch analysis

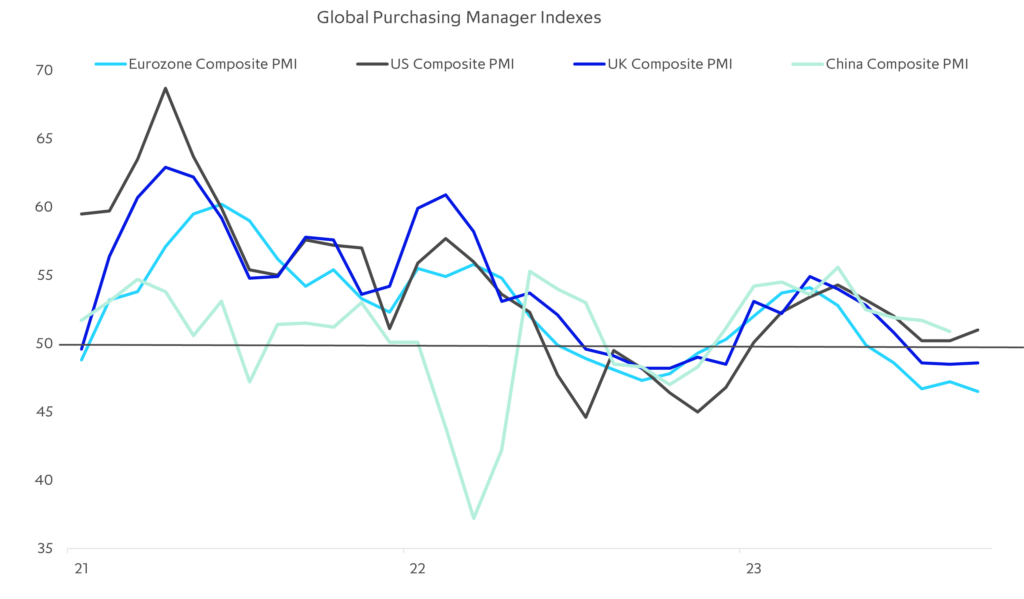

Global growth is slowing – geopolitical issues add to downside risks

Purchasing manager surveys show growth is losing steam across most major economies.

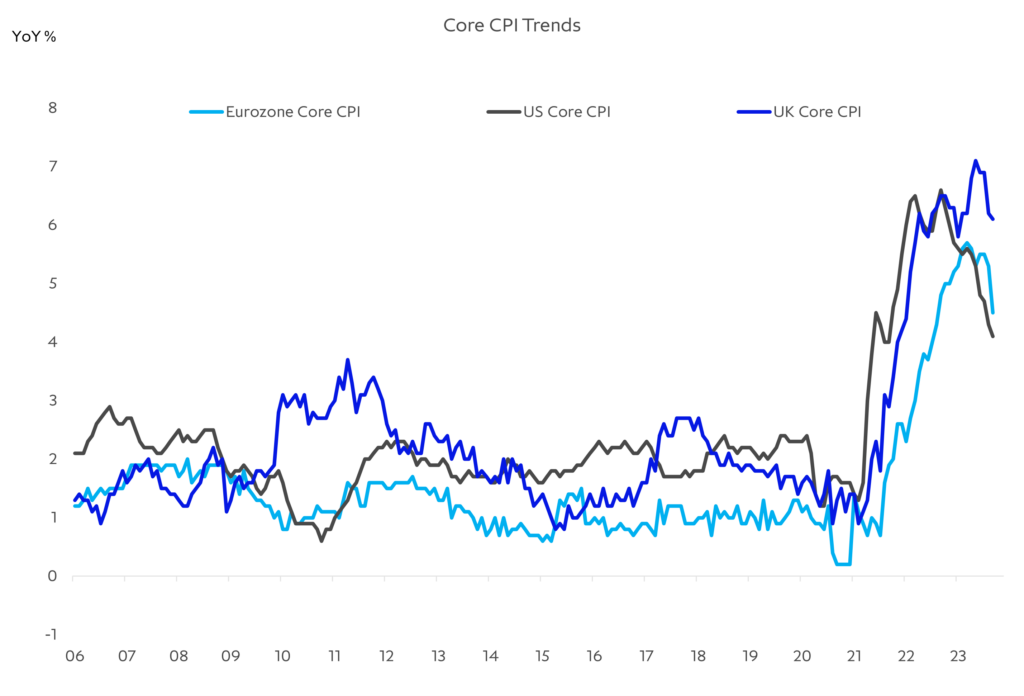

Core inflation is falling, but only gradually . . .

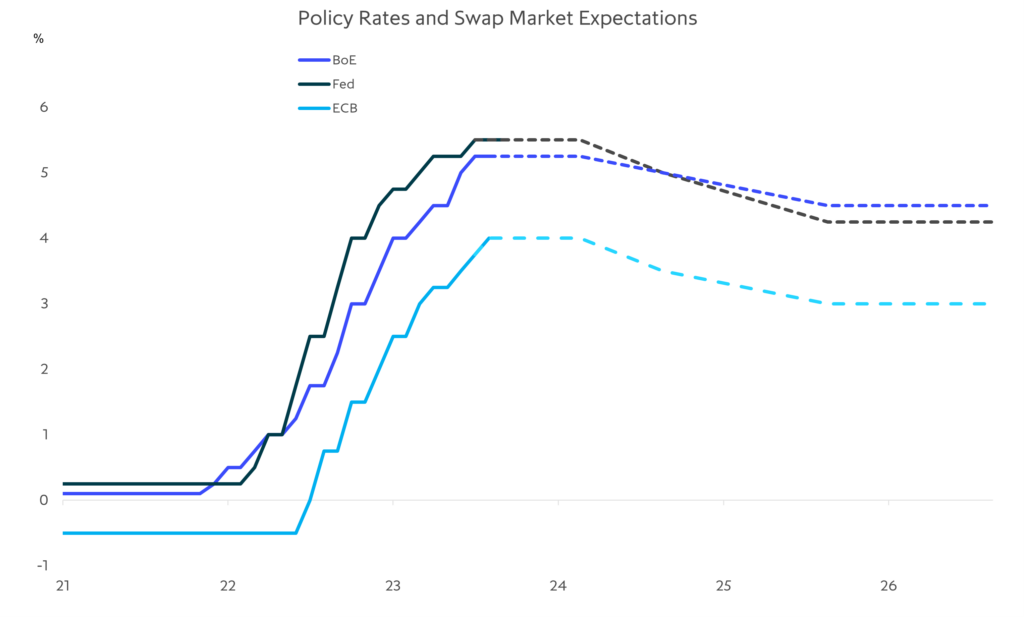

. . . keeping policy rates and bond yields “higher for longer”

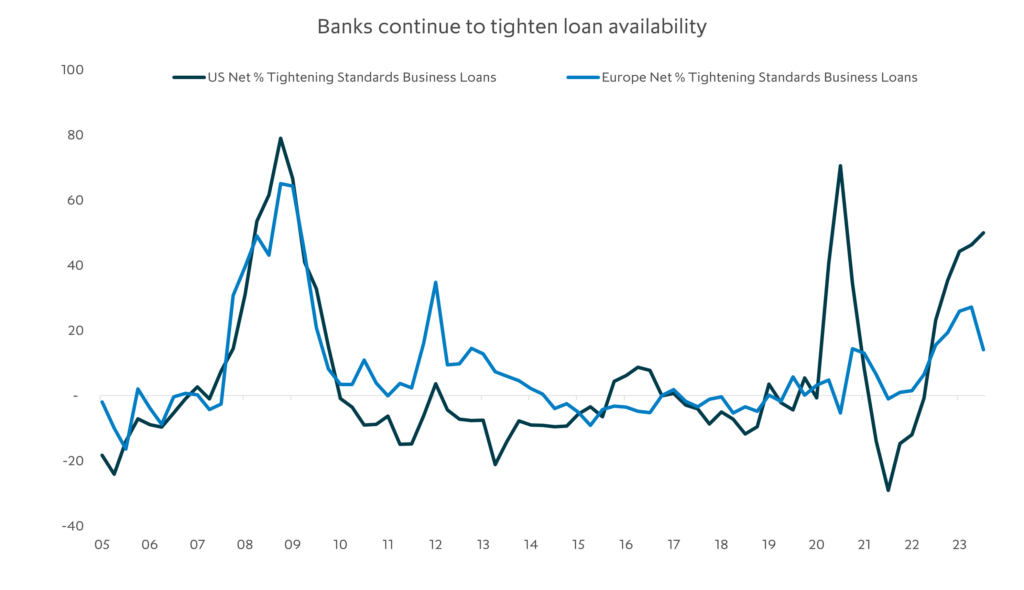

Banks continue to retrench – boosting demand for alternative capital

Banks have substantially tightened lending standards.

Go deeper

- Find out what we do

- Subscribe to our monthly newsletter

- Follow us on social media