Overview

- A sharp fall in energy prices back to pre-Ukraine invasion levels, large and effective fiscal support programs, strong labour markets and tailwinds from economic re-opening following the Covid-19 pandemic have combined to support growth. While the business operating environment is likely to become more difficult, weakness is expected to be very sector and company specific, with companies in less cyclical, less energy intensive sectors continuing to perform well.

- Europe builds near record level of natural gas supplies, driving prices back to pre-invasion levels and substantially reducing the economic impact of cut off of Russian natural gas. More successful than expected moves to secure alternative energy supplies, more efficient use of existing resources and a warmer than usual winter all played a role. Floating LNG terminals, new pipelines, increased build out of alternatives and more efficient use of energy remain a key focus of policy.

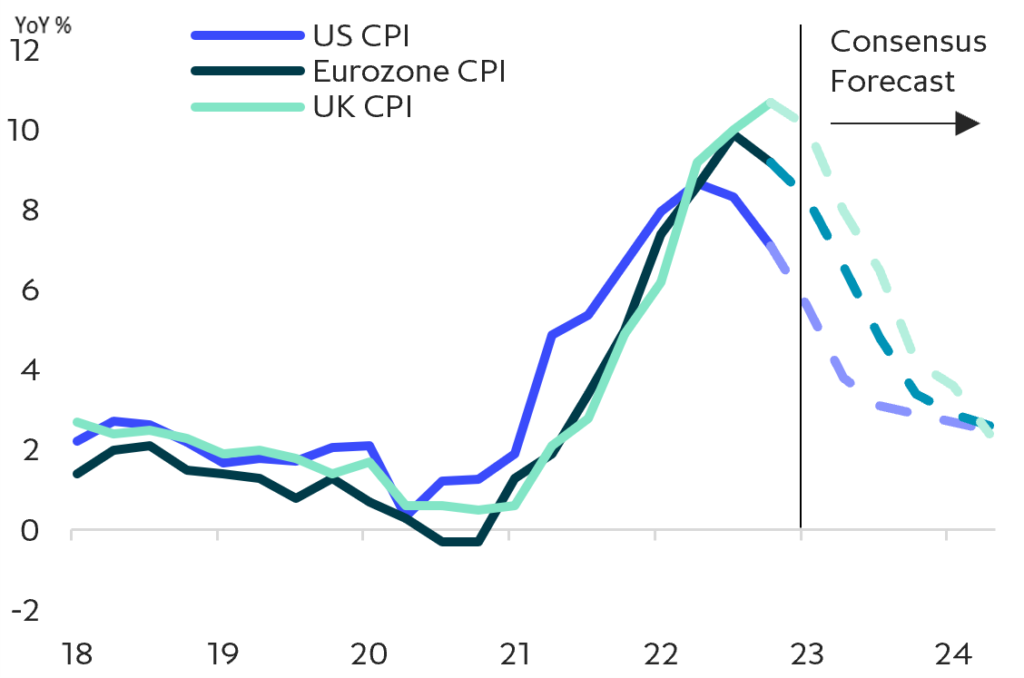

- Inflation should fall sharply in the coming months. Falling energy and food price inflation should lead to a sharp drop in headline inflation rates over the next few months. Core inflation should also fall as supply chain bottlenecks ease and property markets cool. The wild card is wage growth, with pandemic-driven distortions to labour market supply and demand keeping labour markets tighter for longer – though there are now signs wage growth is starting to ease in most countries.

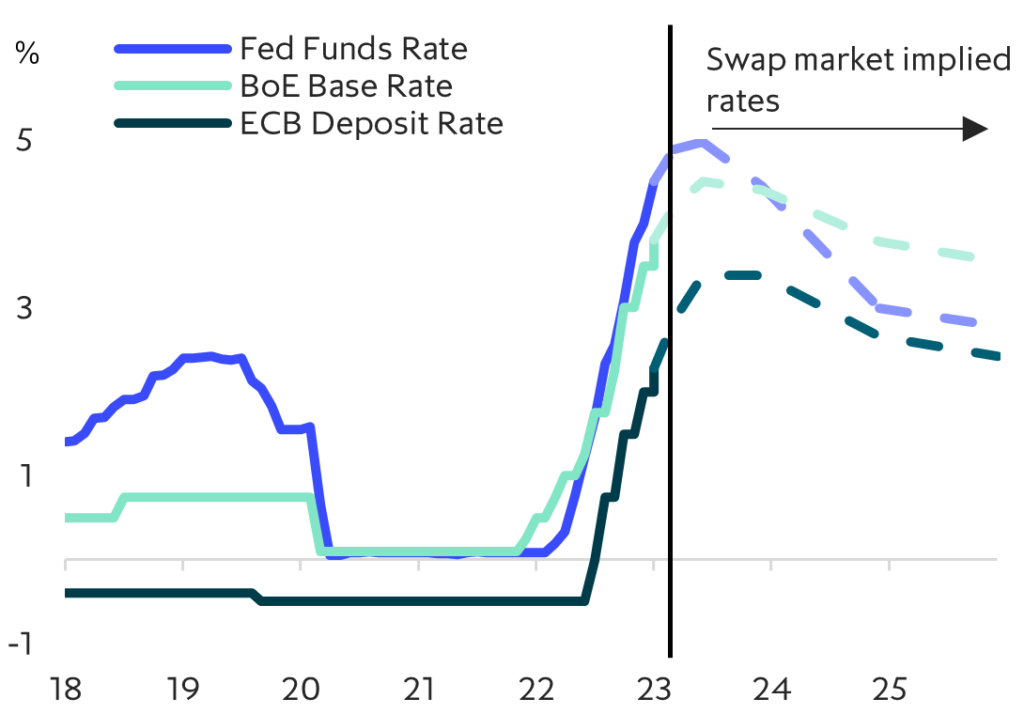

- Interest rates higher for longer? The fall in inflation should allow the Fed, ECB and BoE to halt rate increases in the next few months, but a swift shift to rate cuts by central banks is unlikely. Swap markets are currently pricing peak rates of 5.0%, 3.5% and 4.5% respectively. More resilient than expected growth and still tight labour markets indicate central banks may feel the need to hold rates higher for longer – particularly in the US and Eurozone.

- China reopening to boost global growth in H2 2023, with Europe and Asia key beneficiaries. China’s move to dismantle its zero-covid policy and allow its economy to reopen will likely lead to a strong rebound in private consumption and investment and a rise in tourism outflows. As the world’s second largest economy, the rebound in growth should support global growth, with Asia and Europe key beneficiaries.

- The slowdown in growth in 2023 is likely to be highly sector specific, with less affected sectors continuing to outperform despite a broader slowdown. Less cyclical and less energy-intensive sectors such as healthcare and biotech, technology and software, business and financial services and education are likely to hold up relatively well over the next quarters. Businesses directly involved in or facilitating the acceleration of the green energy transition are likely to continue to see significant tailwinds.

Mild and highly sector specific slowdown ahead

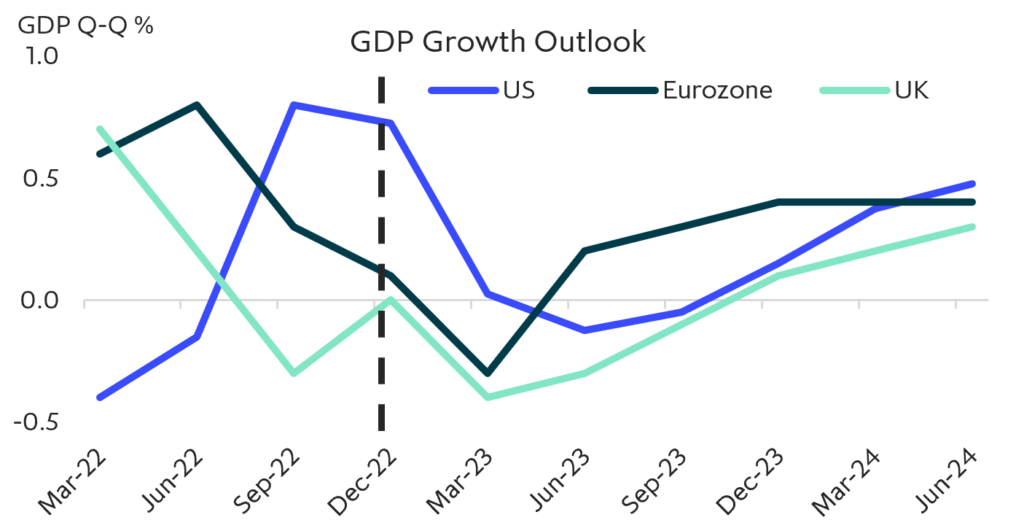

Growth in Europe and the US surprised consensus to the upside in 2022, with most economies maintaining positive growth throughout the year despite sharply higher energy prices and interest rates. There are a number of reasons for the better expected growth, including sizeable government fiscal intervention to support households and businesses, the run-down of record levels of savings, near full employment and continued tailwinds from post-pandemic economic re-opening. A sharp fall in natural gas prices in the latter part of the year has provided additional support, as warmer weather, more efficient consumption and rising use of alternative energy sources allowed Europe to raise its natural gas storage to record levels. Lower oil and gas prices have added upward impetus to growth and sentiment in early 2023. Looking into the rest of 2023, as the lagged impact of the rise in interest rates and input costs starts to bite and tailwinds from post-pandemic re-opening and lockdown savings rundowns start to wane, it is likely the business operating environment will become more difficult. However, as we highlight in our latest Private Company Trends report, private companies come into this period in healthy shape. Leverage is down from pandemic highs, interest coverage remains high and equity cushions are still at comfortable levels. China reopening following the dismantling of its zero-covid policies will likely support global growth later this year – with Asia and Europe key beneficiaries. While it is likely company fundamentals at an aggregate level will weaken, we think the deterioration will be relatively modest. Performance will also vary widely at a country, sector and company level, with companies in the less cyclical, less energy-intensive sectors that private markets investors tend to be exposed to continue to perform well.

Europe proving more resilient to energy shock than expected

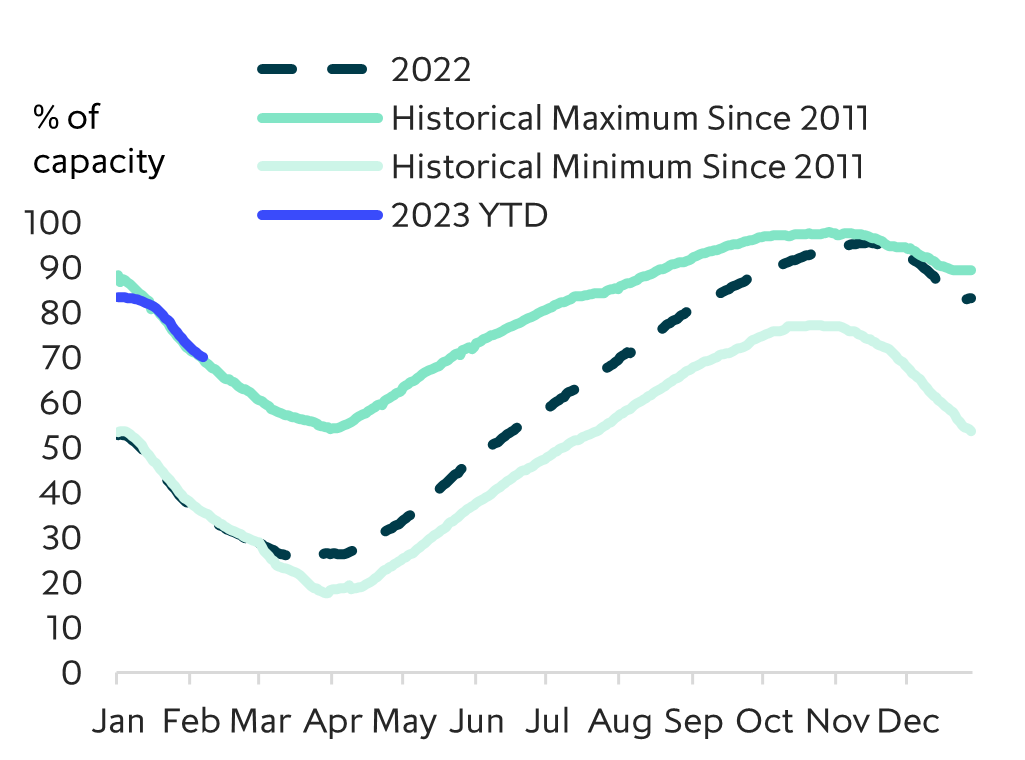

Recent economic data shows that the economic health of Europe and the US through to the end of 2022 has been much better than most expected earlier in the year. Europe in particular has surprised to the upside, with strong fiscal responses to the energy shock providing support to households and businesses, and tailwinds from post-pandemic reopening keeping demand for services strong. More successful than expected moves to secure alternative energy supplies, more efficient use of existing resources and a warmer than usual winter helped push Europe’s natural gas supplies to near record levels, allowing natural gas prices to return to pre-invasion levels.

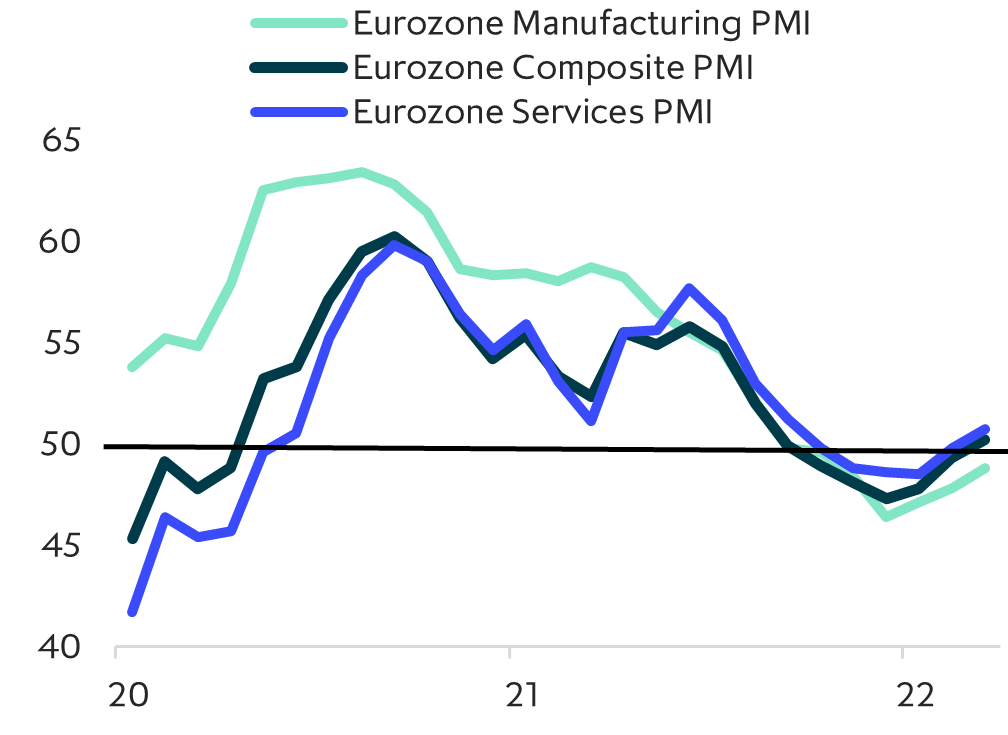

Europe’s purchasing manager indexes, one of the better coincident indicators of growth momentum, rebounded in January, with the Eurozone composite index rising above 50, an indication of expansion. Services growth has been particularly robust, with entertainment, recreation, retail, travel and food services seeing the strongest demand as consumers released pent up demand built up during the pandemic. A strong jobs market helped boost consumer confidence, which together with high saving, supported consumption despite falls in disposable income as inflation increased. Consumer and business confidence indicators across most of Europe bounced quite strongly at the end of 2022 and into early 2023.

While there is still substantial uncertainty about the global outlook, on current trends it is looking increasingly like Europe will avoid recession in 2023. While the lagged impact of higher interest rates and reduced tailwinds from re-opening are likely to weigh on growth, the region is also likely to be one of the biggest beneficiaries of China’s economic re-opening following the removal of its zero-covid policies. As always, there will likely be substantial performance variation at a sector and country level, bringing opportunity for investors with strong local and sector expertise.

Europe cyclical indicators have steadied

Europe gas inventories holding near record high

Growth in Europe and the US has been much more resilient than most expected, with Europe in particular surprising to the upside

US benefiting from strong services demand

Like Europe, the US has proved to be more resilient to higher interest rates, energy and other input costs than many expected. US preliminary Q4 GDP came in at a healthy 2.9% annualised pace with consumer spending on services the main driver of growth. A breakdown of the data show that housing, health care, recreation services, food services and accommodation saw particularly strong demand.

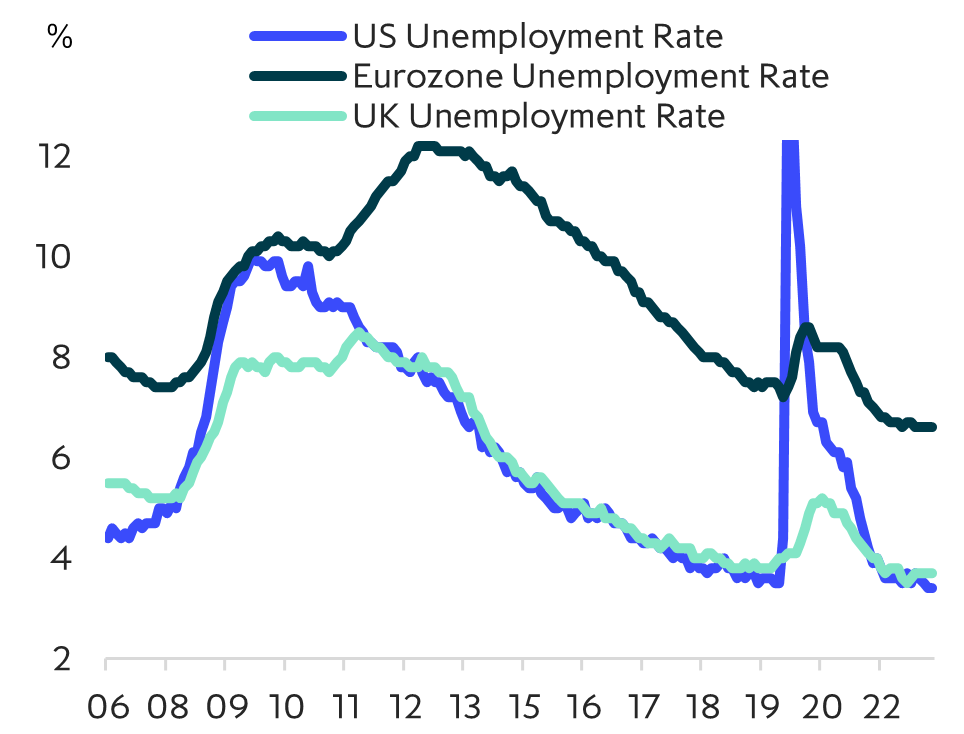

The US labour market has been remarkably resilient to Fed tightening so far, with the unemployment rate in January falling to its lowest level since 1969 and the ratio of unemployed people to job openings at a record low of 0.5. However, as the Fed has noted, there are signs wage growth is starting to moderate, with payroll average hourly earnings growth slowing and the employment cost index trending down for the past two quarters.

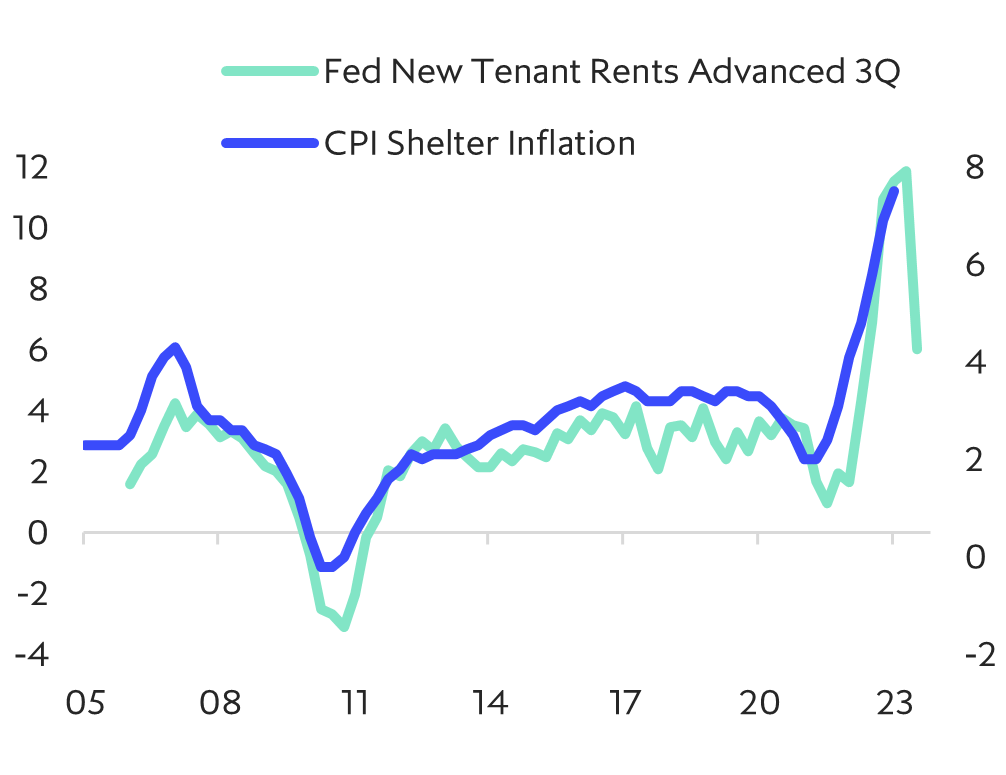

In addition, the housing market has continued to weaken, putting downward pressure on residential investment and likely leading to a fall in shelter inflation (one-third of CPI basket) later this year.

The big question for 2023 is whether the resilience of the labour market and wages to higher rates so far continues and forces the Fed to tighten further in 2H 2023, or if the full impact is still to come.

Current swap market pricing puts the Fed’s peak rate at around 5% in June, implying two more 25bp increases, with its first cut coming in December. However, unless there is quite a quick easing of current labour market tightness and/or a sharp fall in core inflation excluding shelter, rate risks in the US are biased to the upside in the near-term in our view.

Inflation in major markets is trending down

US shelter inflation should start to fall soon

In 2023 the business operating environment is likely to become more difficult, but weakness is expected to be very sector and company specific, with companies in less cyclical, less energy intensive sectors continuing to perform well.

Mild UK recession ahead, but systemic risks remain low

The UK economy underperformed its peers in 2022, with consensus, IMF and BoE forecasts anticipating mildly negative growth through most of 2023. UK households have experienced a particularly sharp energy price shock as around 80% of heating and around 40% of electricity is generated from natural gas. Due to energy pricing mechanisms, a large part of the price increases were quite quickly passed through to end users. It has not just been energy and food prices hitting consumers, with core inflation holding at higher levels than most of the rest of Europe.

Mortgage rates have also risen sharply as the BoE has raised rates (with PM Truss “mini budget” debacle adding to the turmoil) and with around 20% of mortgages on variable rates (with most of the rest on 2 to 5yr fixed rates) the impact has come through more quickly than Germany, France and the US where longer term fixed rates make up the bulk of the market.

Despite the relative weakness of the UK economy, strong consumer, financial and corporate balance sheets mean systemic risks are low and the recession should be mild. As energy prices fall and core inflation and wages moderate the BoE should be in a position to start lowering rates in the latter part of the year, helping to start the healing process.

Therefore, while the business operating environment for many companies in the US, UK and Europe will likely become more difficult in 2023, barring another large external shock, severe recession of the likes of 2008/09 is likely to be avoided. While there are likely to be pockets of distress, as during the pandemic, well managed companies in less cyclical sectors with access to flexible capital are likely to continue to perform well in our view.

But labour markets are still tight

Central bank rates: higher for longer?