- Web page edition updated 18 December 2023

- Go to original PDF edition

Overview

- The global economy and markets have been remarkably resilient in the face of tightening financial conditions and geopolitical upheaval over the past few years, with economic growth holding up better than most analysts’ expectations.

- Global growth likely to slow in 2024 as the lagged impact of higher interest rates, waning tailwinds from economic re-opening, fiscal tightening, and dwindling Covid “excess” savings weigh on domestic demand.

- However, structural strengths, including strong household balance sheets, robust banking systems and healthy private company balance sheets, should protect against sustained deep downturns in our view.

- On our base case scenario, the most likely outcome is a period of sluggish growth, with interest rates staying high relative to history as wages and core inflation take time to fall back towards major central banks medium- term targets.

- Two key potential upside surprises to the growth and earnings outlook are 1) a bottoming of the global goods de-stocking cycle and a related pickup in manufacturing activity and 2) more proactive monetary and fiscal easing in China providing a boost to the global economy.

- Geopolitical risk, however, remains a wild card, with spillovers from ongoing conflicts in the Middle East and Ukraine, US-China tensions and an exceptionally busy pipeline of national elections having the potential to quickly and dramatically alter the economic and investment landscape.

A sluggish growth environment

Geopolitical risks abound

Geopolitical risk always lurks in the background. However, risks appear particularly high at present, with numerous conflicts having the potential to escalate, tensions between major powers high and potential watershed elections scheduled for 2024.

The Israel-Hamas war has so far had limited spillover effects on the global economy and markets because the war has remained mostly contained to Gaza and Israel. However, the risk of escalation and enlargement is high – with the oil price the likely main conduit of the crisis to the global economy and markets.

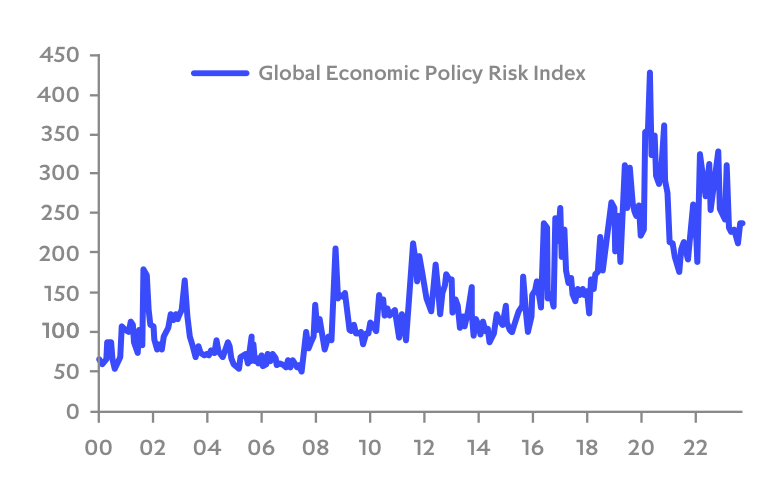

Global policy risk remains elevated

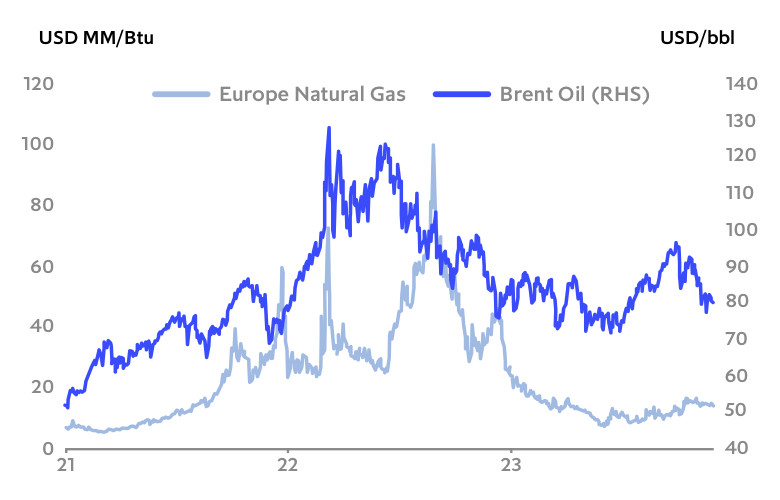

The war in Ukraine also remains a key macro risk. Europe’s rapid diversification of its sources of energy supply and its adept management of energy demand has blunted the economic impact on Europe’s economy to a few key sectors – with Germany’s energy-intensive heavy industry the main casualty. While wider economic damage as been contained so far, further disruptions to energy and food markets and supply chains remain a real risk. A rebound in natural gas and food prices would undermine the recent good progress made in containing inflation and provide a blow to recently improving real consumer disposable income.

Energy markets unfazed by geopolitical risk – so far

An exceptionally full political calendar

In addition to the ongoing and unpredictable economic spillover risks stemming from the Israel- Hamas war and Russia’s aggression in Ukraine, the political calendar is full of potential market moving events next year.

The Economist magazine dubbed 2024 the “biggest election year in history”, with 76 countries scheduled to hold elections and of those they estimate around 43 will see fully free and fair votes [1]. While most of the elections are unlikely to have a major impact on the global economic outlook or major markets there are a few that may.

Key Elections in 2024

| Country and Type of Election | Date |

|---|---|

| Taiwan General Election | 13 January 2024 |

| Indonesia Presidential Election | 14 February 2024 |

| India General Election | April-May 2024 |

| European Union Parliamentary Elections | 6-9 June 2024 |

| US Presidential Election | 5 November 2024 |

| US Senate Elections | 5 November 2024 |

| US House of Representatives Elections | 5 November 2024 |

| UK General Election | Before end Jan 2025, with May or Oct 2024 viewed as most likely timing |

The US is facing a watershed presidential election on 5 November, with a number of recent polls showing likely Republican nominee Donald Trump running ahead of current incumbent Joe Biden in key swing states.

The UK has the potential to see a major shift in policies, with the incumbent Conservative Party currently well behind the Labour Party in most polls and the next general election due to be held before end January 2025.

Europe also faces elections next year, with its five-yearly parliamentary elections scheduled for June. Recent polls indicate right-wing parties are in the ascendence, with the recent election results in the Netherlands a worrying example of this trend.

Two of the world’s most populous countries, India and Indonesia will be holding national elections.

Taiwan will be choosing between incumbent pro- China independence and pro-China unification parties, with a likely pro-independence party win potentially further heightening tensions in the South China Sea.

Conflict, terrorist and cyber risks are high

In addition to key elections, continued high tension between major powers will keep geopolitical risk elevated. Despite recent moves to improve relations, including the recent face-to-face meeting between US President Joe Biden and China President Xi Jinping, US-China relations remain tense and the risk of further tit for tat trade and investment restrictions remains high. While most experts believe the near-term risk of an invasion of Taiwan by China is low, China’s continued push to expand its influence in the South China Sea increases the risk of military accidents. Russia and Iran are also likely to continue to use proxies to increase political instability in the Middle East and the risk of terror and cyber-attacks remain high. Therefore, while the global economy has weathered the many geopolitical shocks thrown at it over the past two years, policy and political risk levels are likely to remain high going forward and will need to be monitored closely given their potential to quickly and dramatically change the economic and investment landscape.

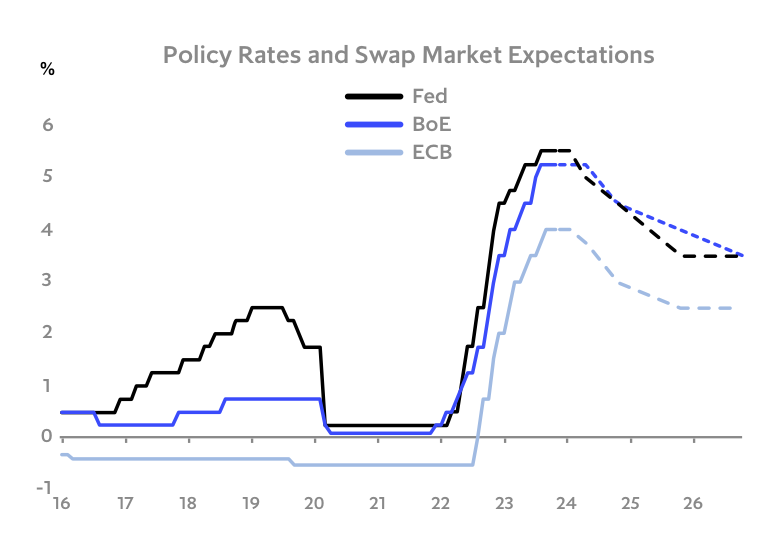

Lower interest rates in 2024

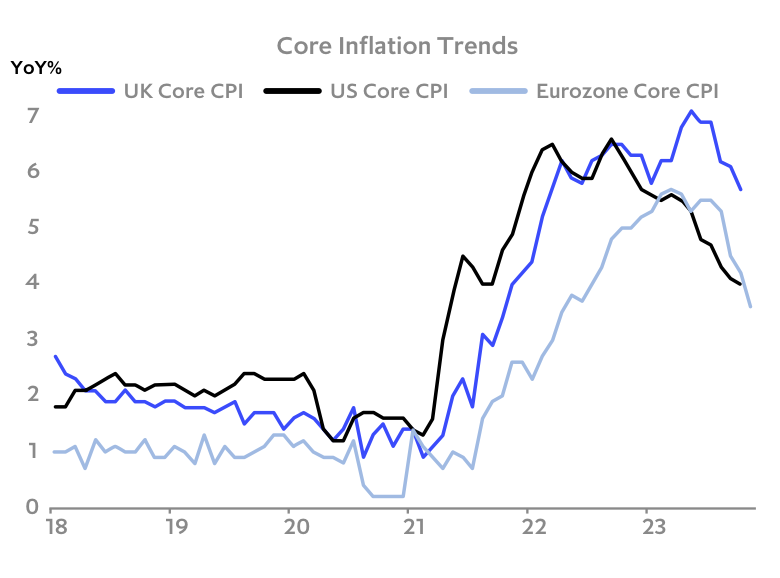

With labour markets remaining tight relative to history and wage growth and core inflation still well above medium term targets, the Fed, ECB and BoE have been pushing back on market expectations of sharp near term rate cuts.

Inflation tamed?

In the first 10 months of 2023, longer term government bond yields adjusted upwards to reflect a “higher for longer” scenario, as well as anticipated large upcoming government net bond issuance. The resilience of US consumer spending and labour data together with the ramp up of US government net debt issuance and move by the BoJ to relax its yield curve control policy added to the upside impetus. However, on our base case scenario of slower growth in most major economies in the coming quarters, we think bond yields have likely seen their peaks for the cycle and will fall further in 2024.

Higher for longer

Resilient Europe growth

Headline Europe growth has been slowing in the second half of 2023 and is likely to remain sluggish in early 2024 on the back of the lagged impact of higher interest rates, tighter fiscal policy and lacklustre external markets growth.

Although the ECB has indicated it is at or near the end of its rate hikes, with labour markets still tight and core inflation taking its time coming down, the most likely scenario in the near term is one of weak economic growth and interest rates near current levels.

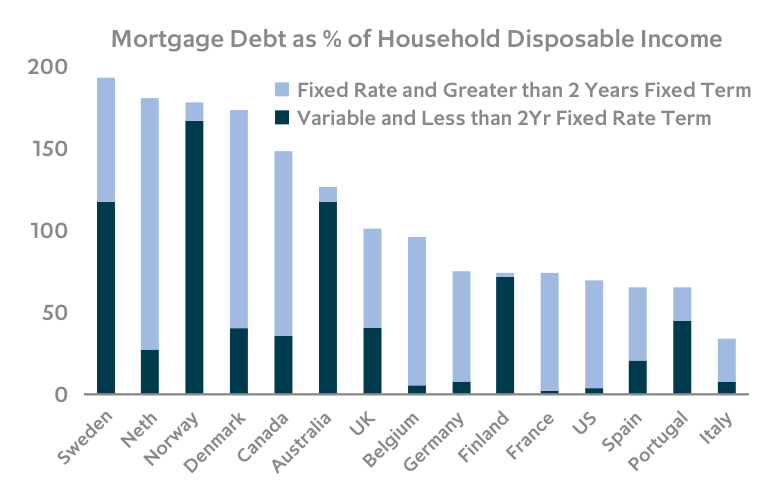

Mortgage rate rise impact varies widely by country

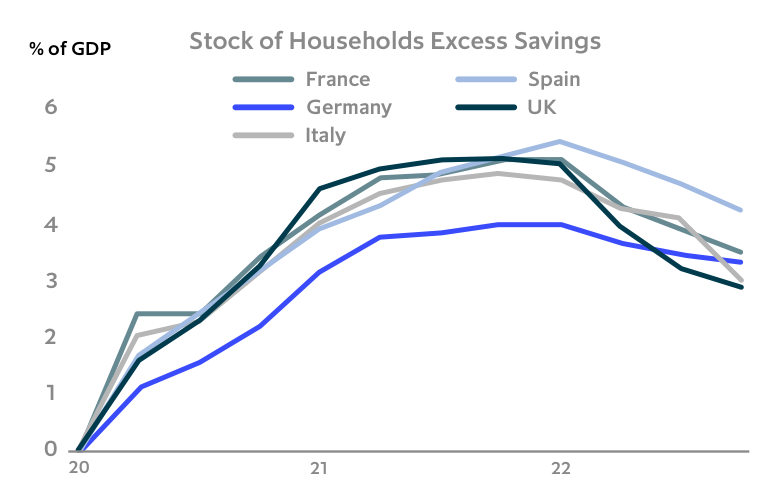

However, a sharp downturn is unlikely and there are a number of factors that will support growth in 2024. On most estimates, Europe still has substantial excess savings accumulated during the Covid period and in most countries fixed mortgage rates have limited the impact of higher interest rates on household income. Exceptions in Europe have been Sweden, Norway, Finland and Portugal.

Large, accumulated savings from the pandemic, continued low unemployment relative to history and rising real disposable incomes as wage growth outpaces inflation should provide structural support to private consumption. Europe’s banking system is strong, with Eurozone banks’ Tier 1 capital more than double 2008 levels and, learning from previous crises, the ECB has created new powerful tools, such as the Transmission Protection Instrument (TPI) and others, to support financial systems if needed.

Large stock of excess savings supports households spending

As the drag from monetary tightening fades and the industrial cycle bottoms, Europe’s growth prospects should improve later in 2024.

Potential upside surprises include 1) a pick-up in China growth as monetary and fiscal easing feed through the economy and households continue to gradually normalise their spending and 2) a potential upward turn in the global industrial cycle as the global inventory cycle bottoms and manufacturing demand picks up afer an extended period of weakness. While these are not part of our base case scenario, both have the potential to provide upside surprises in 2024.

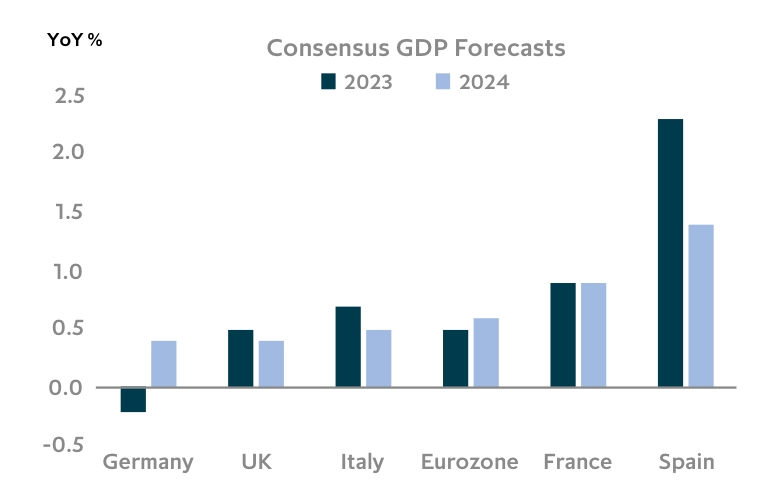

Positive growth forecasts for Europe and UK

A more complicated situation in the UK

The situation in the UK is more complicated. With around 20% of fixed rate mortgage deals coming to an end in 2023 and 2024, the rate hikes of the past two years are still feeding through the system and will likely weigh on private consumption in 2024.

The dilemma the BoE faces is that wage growth and core inflation have remained much higher than in Europe or the US even as economic growth slows.

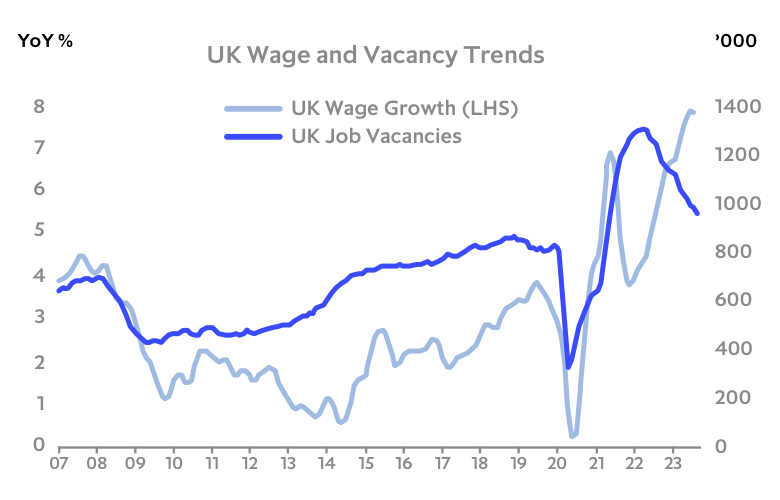

A key problem in the UK has been a lower labour participation rate since Covid, with workers reporting long-term sickness the main factor behind the drop. Skills mismatches as the UK’s migration flows have shifted since the Brexit vote are another factor cited for the high job vacancy rate. While the vacancy rate, wage growth and core inflation will likely start to fall more quickly in the coming months, they are likely to remain elevated relative to history through the first part of 2024, potentially forcing the BoE to maintain tight monetary policy into an economic slowdown.

UK wage growth has remained stubbornly high

US growth is slowing, but structural strengths limit downside

The US economy is also slowing, perhaps more than headline expenditure side GDP numbers indicate, but strong household balance sheets, long-term fixed mortgage rates, low unemployment and healthy money centre banks reduce risk of sharp downturn.

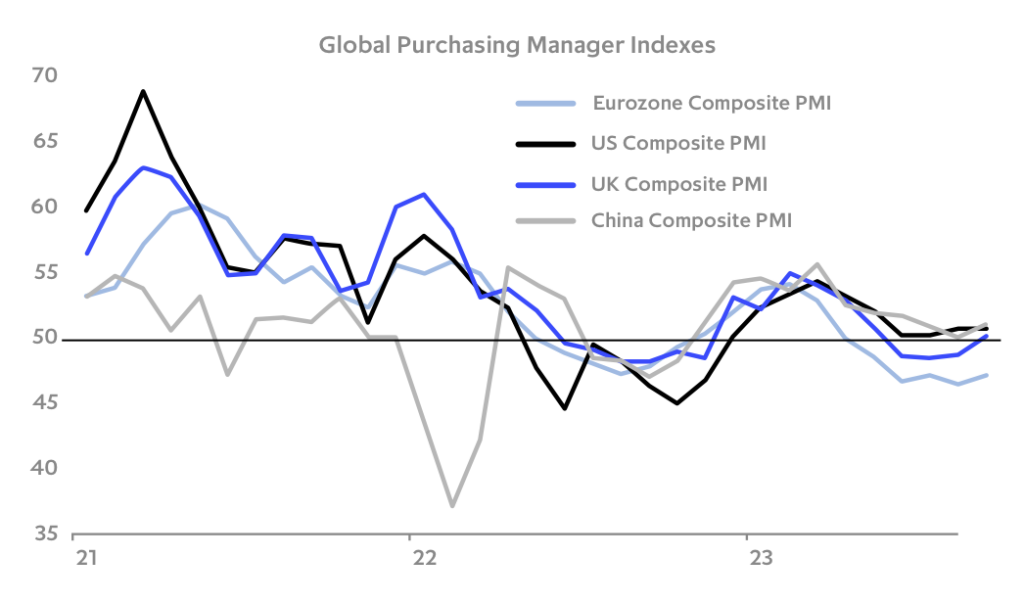

The US composite PMI, usually a good indicator of economic growth momentum, has outperformed Europe’s year-to-date but has been hovering near 50 since August, indicating growth momentum has flattened out. However, because of the supportive factors mentioned above, the most likely scenario is a period of sluggish economic growth rather than the kind of deep downturn that generally precedes a large, generalised rise in corporate distress.

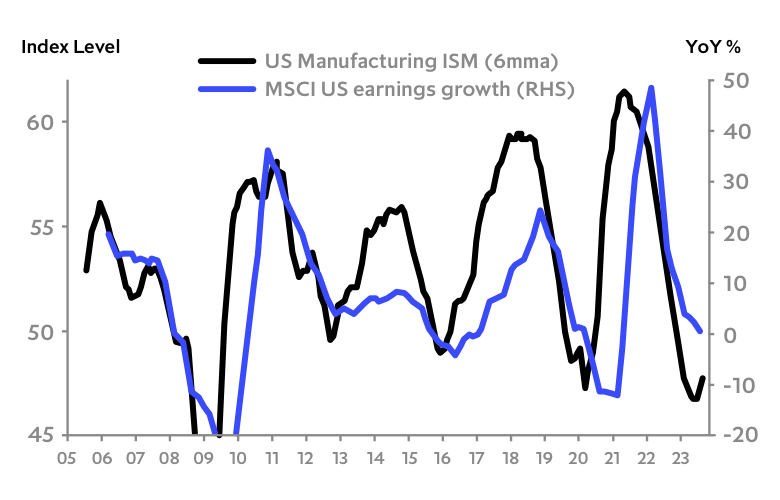

It is interesting to note that public company earnings growth has slowed quite sharply in 2023 despite the relatively strong headline GDP growth numbers. Historically US benchmark equity earnings growth has correlated well with the US industrial cycle (proxied in the chart below by the US manufacturing ISM). If the global goods de- stocking cycle has run its course, a potential upside surprise in 2024 is a turn in the industrial cycle and earnings downcycle. Something to watch as we move into 2024.

Potential turn in the industrial and earnings cycle in 2024?

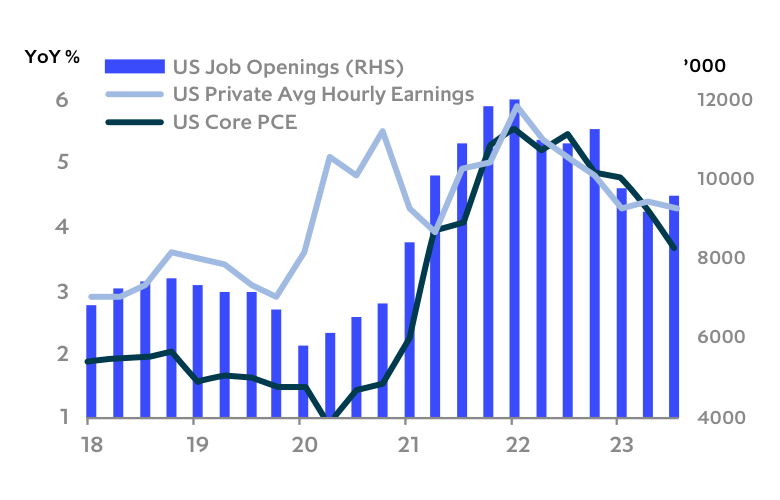

In terms of inflation, the US is now seeing a steady decline in the core inflation measures most closely watched by the Fed, and an easing of labour market tightness and other lead indicators point to further declines in the coming months. On our base case of weak growth in the coming quarters and a continued easing of inflation pressures, Fed rates have likely peaked and have scope to be cut as soon as Q2 2024.

US inflation cooling as labour market eases

Developed Asia to continue to outperform

China growth has disappointed, weighed down by its highly indebted property sector. However, likely further policy easing and post-Covid economic normalisation provide potential upside surprises in 2024. Developed Asia experienced far less of an inflation and interest rate shock than the west, with most economies seeing steady recovery from Covid lows. With sound public finances and less entrenched inflation, policy makers are in a good position to support growth if needed. If China continues its gradual easing policy as we expect and its domestic activity and international tourism outflows normalise back to pre-Covid levels, Asia should see a further acceleration of growth in 2024.

China economic activity continues to normalise

Asset allocation implications

Performance dispersion to remain high

A key feature of the economic landscape is there will likely continue to be wide performance dispersion at a sector level. The most vulnerable sectors in our view are cyclical and interest rate sensitive industries with limited pricing power. Heavy Industry and basic materials are particularly vulnerable, with chemicals, steel, many of the materials sub sectors likely to see intensified pressure on top lines and margins. Parts of the real estate sector, particularly the office sector are likely to remain under pressure. Consumer discretionary spending is likely to slow, with a number of retail sub-sectors and big-ticket consumer durables such as autos most at risk.

However, less cyclical sectors should fare relatively well in our view. Many technology sub-sectors should continue to see strong demand. While some traditional healthcare providers have had to contend with high input costs that have been hard to pass on, there are numerous sub-segments of the healthcare sector that are performing strongly and should continue to provide interesting investment opportunities. Education, communications, parts of the business and financial services sectors, infrastructure, and companies supporting the green energy transition, are all areas we think should continue to perform well.

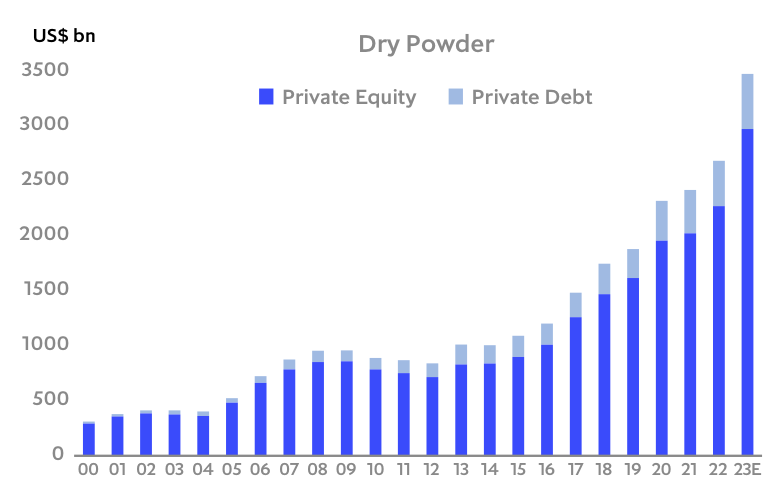

Private markets well positioned to fill funding gap

Private credit in a sweet spot

In terms of asset classes, private credit remains in a sweet spot in our view, with a combination of high contractual returns and seniority in the capital structure well-suited to the current environment of greater interest rate growth and geopolitical uncertainty.

Opportunistic medium to long-term strategies that are able to deploy flexible capital are also likely to perform well as traditional sources of capital from banks and public markets remain constrained.

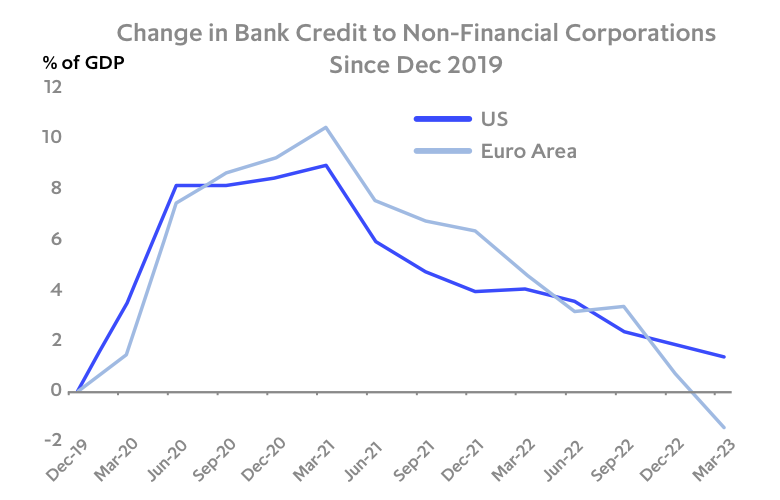

Banks continue to pull back

Strategies backed by real assets with inflation- linked pricing and predictable income streams such as parts of the infrastructure and real estate sectors are also well positioned, with inflation trends still unpredictable and consensus expectations it will remain elevated relative to pre- Covid levels for the foreseeable future.

A focus on free cashflow and pricing power

Looking forward, private markets investors are well positioned for what we think will likely be a more challenging economic and operating environment in 2024. Limited exposure to cyclical sectors, an emphasis on companies with strong recurring cashflow, large stores of dry powder, medium to long-term investment horizons and the ability to provide flexible capital and work closely with portfolio company managements should continue to provide strong competitive advantages in our view.