Key findings of US and European private companies analysis by ICG's Head of Economic and Investment Research Nicholas Brooks

In this 9th bi-annual edition of the ICG Private Company Trends report, we provide an in-depth view of the key fundamental trends we are seeing across this historically opaque segment of the market and assess the outlook for 2023.

Email [email protected] to request a copy of the full report.

Key findings include:

- Private companies across Europe and the US performed strongly through the first half of 2022, and most evidence indicates performance held up into the second half of the year.

- All sectors performed strongly, with consumer discretionary continuing to benefit from economic re-opening and IT, healthcare, industrials and materials maintaining strong growth.

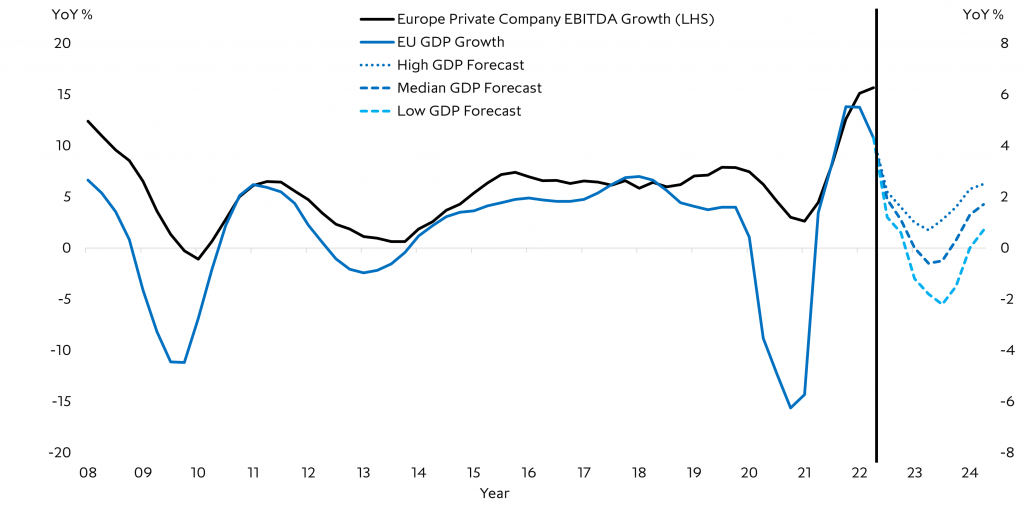

- While revenue growth hit record high levels in Europe and the US, EBITDA growth slowed modestly in the US, indicating not all input costs are able to be passed on.

- Looking into H1 2023, as global growth slows, and the lagged impact of higher interest rates and input costs increases start to bite, it is likely that the operating environment will become more difficult.

- However, as was the case during the Covid-19 pandemic, it is likely that performance will vary widely at a country level, and even more so, at a sector and sub-sector level.

- Looking at the composition of the ICG Private Company Database, there is relatively limited exposure to cyclical sectors and other sectors that are likely to be most affected by the coming slowdown in our view.

- While fundamentals at an aggregate level are likely to deteriorate as growth slows and input costs become more difficult to pass on, limited exposure to the most vulnerable sectors, comfortable leverage, high levels of interest coverage and large equity cushions should hold most private companies in good stead through this more difficult operating environment in our view.

Where to from here?

Key: LHS = left hand axis

Source: ICG Private Company Database, median 4QMA EBITDA data to Q2 2022, GDP growth forecasts based on Bloomberg Consensus high, low and median YoY GDP forecasts as of November 2022