In this quarterly report, Nicholas Brooks, Head of Economic and Investment Research at ICG, gives an update on how we see the economic landscape evolving during 2022 and what it means for companies.

Overview:

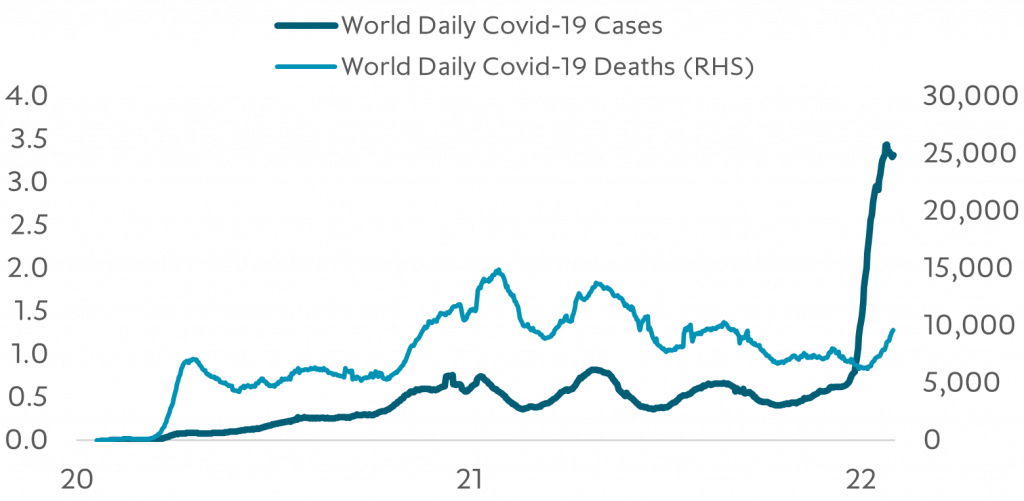

- The Omicron variant of Covid-19 is disrupting, but not derailing, the economic recovery. The rapid spread of the Omicron variant has led to reductions in economic activity in some countries, but lower hospitalisation and death rates relative to previous waves of contagion has meant less severe and earlier relaxation of containment measures in most countries. China’s zero Covid policy, however, indicates supply chain disruptions are likely to remain a problem through most of 2022.

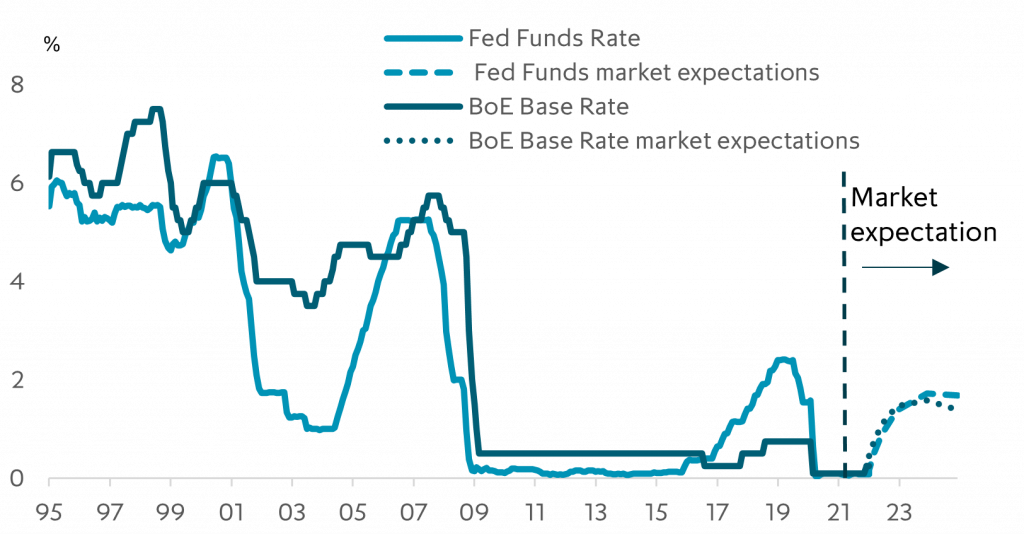

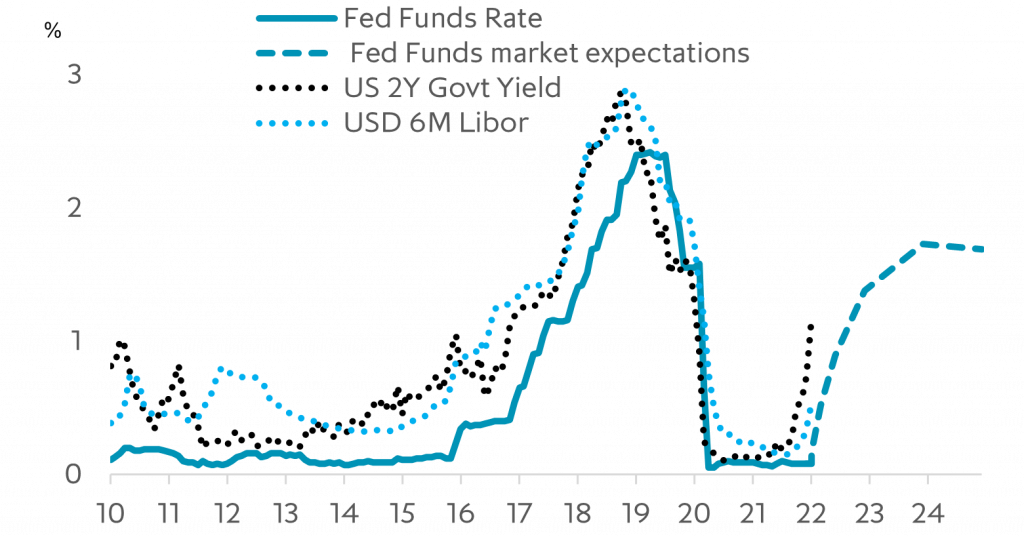

- The hawkish shift by the Fed and BoE has driven short rates sharply higher and flattened yield curves, but rates should remain low relative to pre-Covid levels. With inflation proving more persistent and employment markets tightening more quickly than expected, both central banks have indicated they plan to speed up the normalisation of monetary policy. Markets are currently pricing nearly five rate hikes by both the Fed and the BoE in 2022, with the Fed’s first rate hike expected in March.

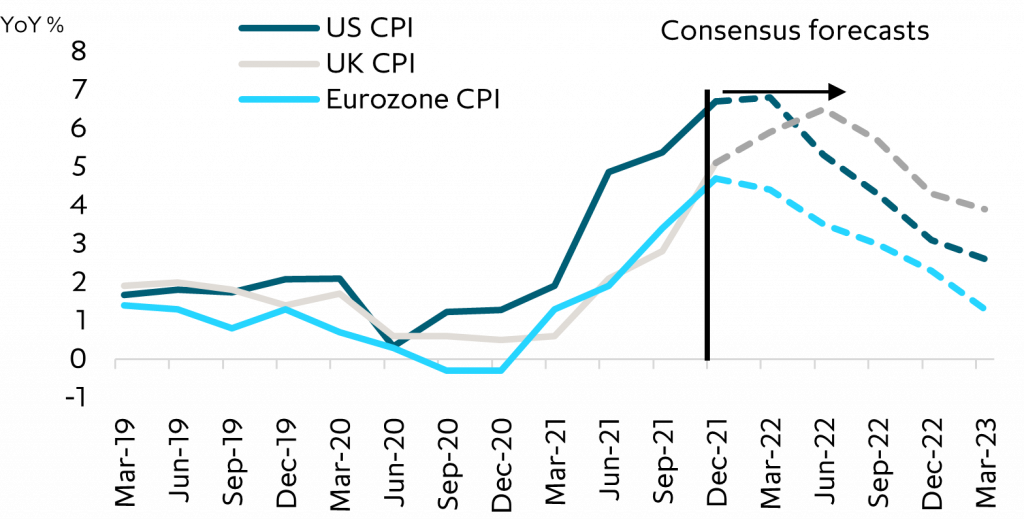

- Inflation has proven more persistent than expected, but is likely fall in 2022. More entrenched supply chain disruptions and a strong rebound in demand and wages as economies have re-opened have kept US and UK inflation, most notably, higher then expected. However, there are early signs supply disruptions are easing which, together with slowing demand and base effects, should push inflation lower later in 2022. This may temper rate expectations later in 2022.

- Slower but still above trend economic growth in 2022 should drive continued healthy earnings growth. With the bulk of growth normalisation done, signs the industrial cycle is past its peak, and fiscal and monetary policy less stimulative, most developed market economies are likely to slow in 2022. Growth, however, should remain positive, supported by the release of pent up household savings and wealth, continued low rates and high government spending relative to pre-Covid levels. The Eurozone is looking particularly well placed in our view, with rates expected to remain near historic lows, fiscal spending strong and normalisation in a number of countries and sectors still not complete.

One of the most significant economic developments over the past quarter has been a dramatic shift in perceptions of how quickly the Fed and Bank of England will tighten monetary policy.

Short rates have moved sharply higher, sovereign yield curves have flattened and market volatility has increased.

Interest rates on the rise

With inflation rising on a more sustained basis than expected and growth and labour markets still strong, both central banks have accelerated monetary policy normalisation plans, with markets now pricing in nearly five hikes each by the Fed and BoE in 2022.

Inflation to subside in 2022

Although the ECB at its February meeting opened the door to possible rate hikes in 2022, it continues to emphasise that underlying inflation pressure remains muted and it will maintain low rates for an extended period. By contrast, with underlying inflation pressure much higher in the US and UK, the Fed and BoE will likely remain under pressure to accelerate policy normalisation in the first part of the year. However, if, as we expect, growth moderates and inflation starts to fall later in 2022, some of this pressure should abate.

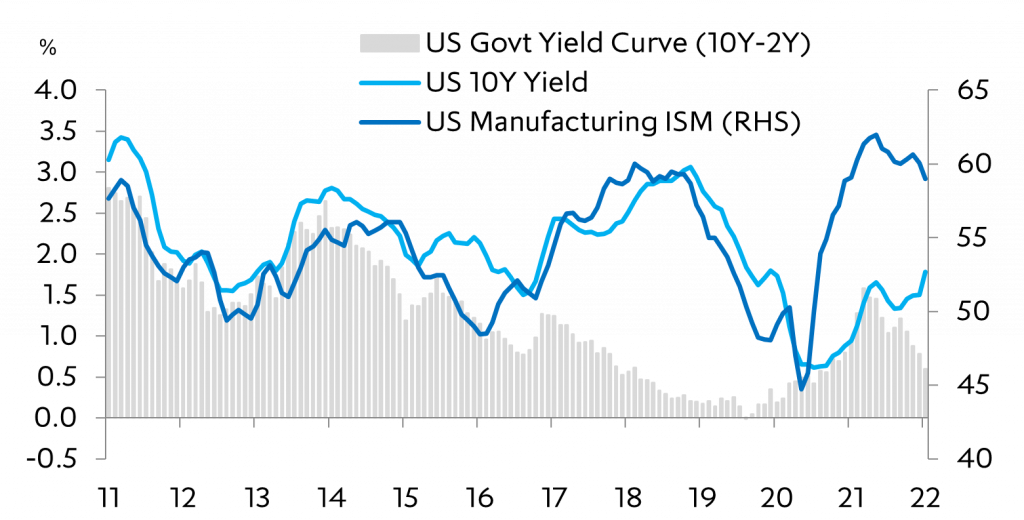

US long yields tend to track the business cycle, indicating curve may flatten further

Therefore, while policy rates and bond yields will likely rise in the near term (potentially pressuring risk assets), we think the ultimate end point for rates will still be low by historical standards and manageable for most companies.

In summary, while risk assets may go through a period of volatility, the operating environment for most non Covid-sensitive companies should remain positive in our view.

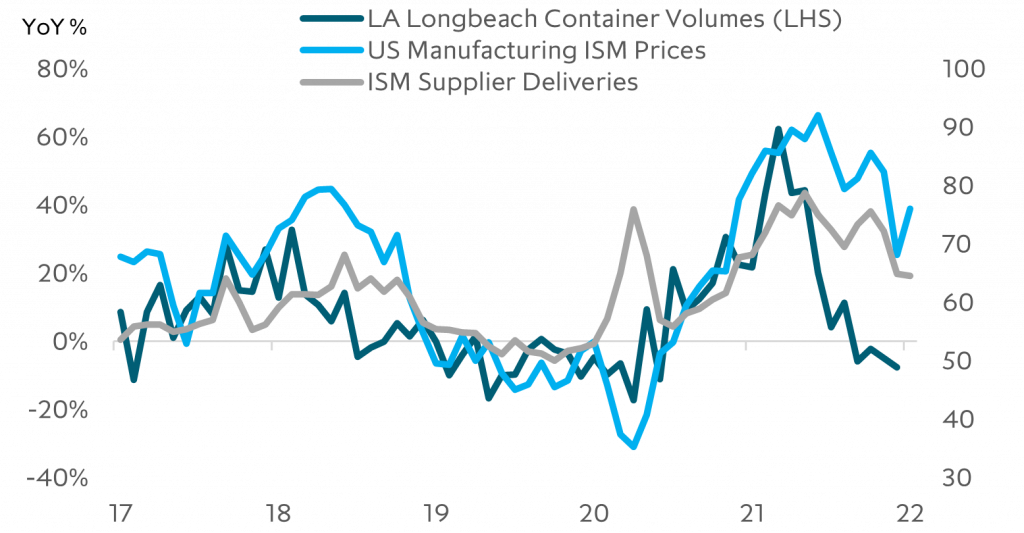

There are early signs supply disruptions are easing.

US: The Fed moves to normalise policy

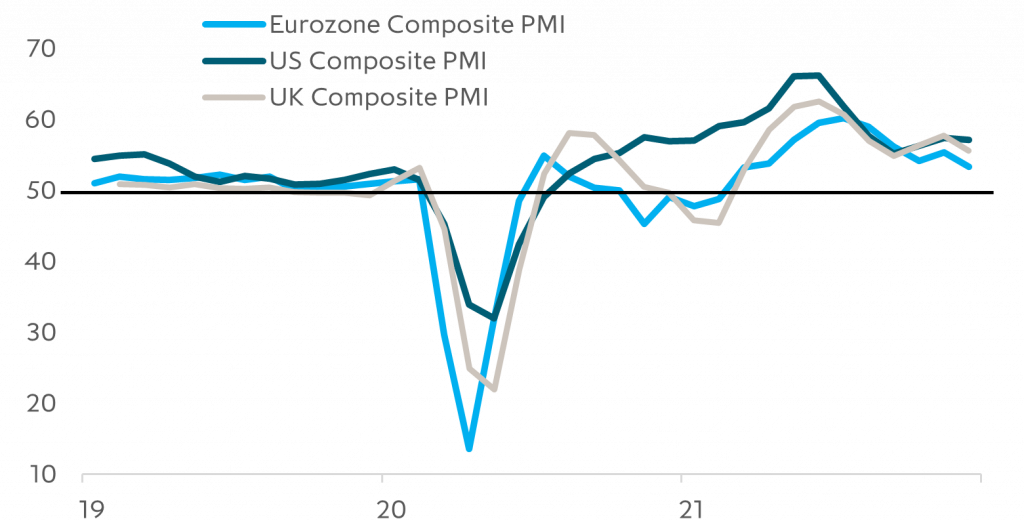

One of the most significant developments in the final months of 2021 was the dramatic policy turn by the Fed. At the Fed’s December policy meeting FOMC members raised their median projected “dot plot” forecasts to imply three 25bp rate increases in 2022, up from zero at their September meeting. The Fed also announced the acceleration of the tapering of its QE programme, likely ending new asset purchases in March and indicating it may start reducing its balance sheet in the second half of the year. The change in stance has helped drive short duration government bond yields sharply higher. The main reasons for the shift in Fed stance are more persistent than expected inflation (7% YoY in December, its highest level in 40 years), faster than expected labour market tightening (unemployment fell to 3.9% in December, nearing its pre-pandemic low of 3.5%) and continued solid economic growth, with both manufacturing and services PMIs still in elevated territory (December manufacturing and services ISM 58.7 and 67.6 respectively).

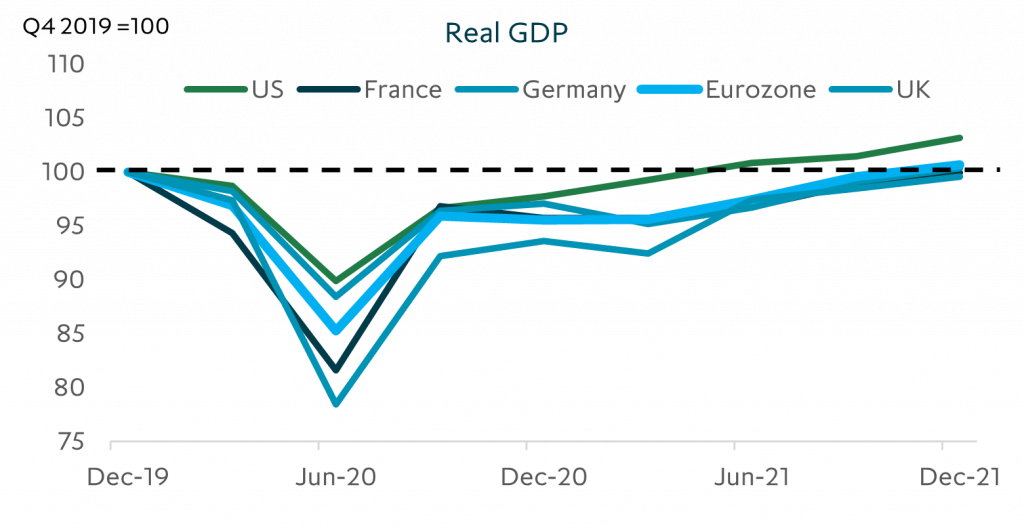

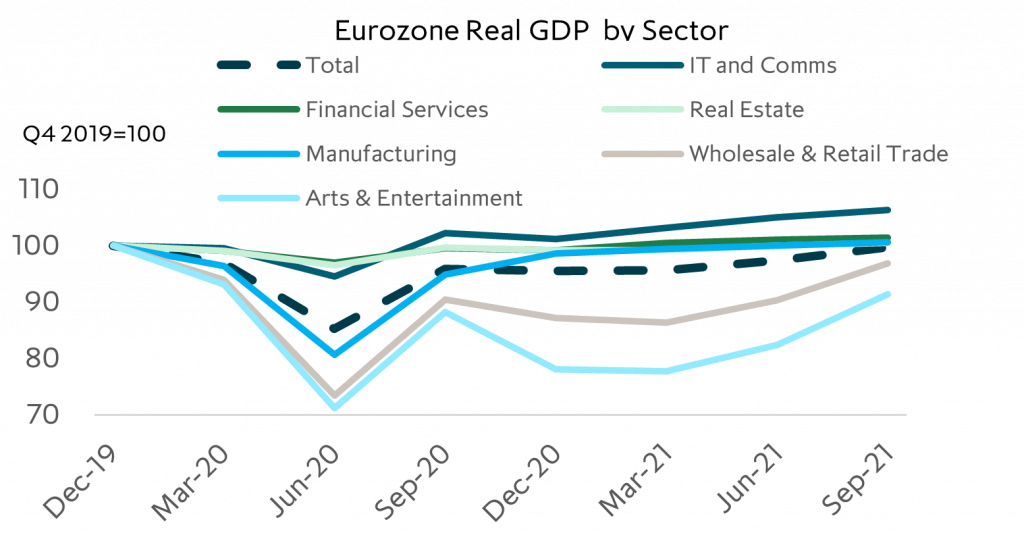

Most major economies recovered to pre-pandemic levels by end 2021

It is interesting to note that longer dated bond yields have shown more muted moves, leading to a flattening of the yield curve, possibly indicating investors question how sustained the growth and inflation rebound will be.

The futures market appears to have already digested much of the change in the Fed’s stance, pricing in nearly five hikes by the end of 2022 and around two more in 2023. If correct, shorter maturity government bond yields likely still have more upside (see chart ‘interest rates on the rise’, above), with spill-over effects into other developed bond markets.

Current Covid-19 wave has been less lethal than previous waves

The longer term outlook for rates will depend very much on the persistence of inflation and the growth outlook. While supply chain disruptions are likely to continue as long as China maintains a zero Covid policy, supplier delivery times, port congestion and shipping costs have recently eased, indicating some reductions in supply bottlenecks may be taking place.

Signs that manufacturing bottlenecks are easing, but China shutdowns remain a risk

Energy prices are a wild card – particularly given uncertainty around a potential Russian invasion of Ukraine. However barring a sustained crisis there, the energy impact on inflation should also dissipate in 2022, allowing inflation to trend down. If, as we expect, demand growth moderates as fiscal policy becomes less stimulative, the industrial cycle weakens and higher interest rates begin to bite, the Fed may start to take a more cautious approach to monetary tightening later in 2022 and keep rates below pre-Covid levels in our view.

Europe and UK: Winter lull, with catch-up in the spring

Europe’s economy continues to recover from its pandemic low in Q2 2020, with Eurozone manufacturing and services PMIs coming in at an expansionary 58.0 and 53.1 in December and unemployment falling back to 7.2%, a fraction off its pre-pandemic low.

Slower growth ahead

Despite the recovery, inflation pressure remains more muted relative to the US and UK, allowing the ECB to maintain a more supportive monetary stance than the Fed or BoE. Eurozone fiscal policy is also expected to be more stimulative than in the US this year, with the funds from the EUR750bn Recovery Fund expected to be disbursed on top of a more expansionary Germany fiscal policy, following the change in government last year, and continued disbursements from France’s Recovery and Resilience Facility on top of other national programmes. Germany is suffering, however, with supply chain disruptions affecting its large manufacturing (particularly autos) sector and the spread of the Omicron variant hampering services during the winter months. These factors are likely to weigh on other European economies this winter.

While risk assets may go through a period of volatility, the operating environment for most non Covid-sensitive companies should remain positive.

We expect, however, that as we emerge from winter Germany and most of the rest of the Eurozone will reaccelerate as high vaccination rates allow for rapid re-opening, fiscal stimulus kicks in and monetary policy continues to be supportive. The January re-election of President Mattarella in Italy bodes well for stability there. Looking forward, April and June elections in France and spill-over effects of a potential Russian invasion of Ukraine are key risks to watch.

Recovery remains uneven at a sector level

We expect as Europe emerges from winter, Germany and most of the rest of the Eurozone economies will reaccelerate as high vaccination rates allow for rapid reopening, fiscal stimulus kicks in and monetary policy remains supportive.

Short rates likely have more near-term upside as Fed and BOE normalise policy

The UK is expected to follow a similar growth trend to the Eurozone, though inflation will likely stay high through April due to lagged energy price pass through. Three factors that have the potential to weigh on the recovery are tighter policy from the BoE (though we think market expectations of nearly 125bps of hikes in 2022 are overdone), growing supply chain frictions caused by Brexit, and rising energy and other living costs (CPI up 5.4% in December) eroding real spending power. Although we don’t think these factors are likely to be sufficient to derail the recovery, they are risks to monitor.