FY26 was a strong year for ICG. We reinforced our scaled competitive position, established a strategic relationship with Amundi, and built on our track record of strategic and financial growth. We surpassed our fundraising expectations by some margin, putting us on track to deliver our four-year fundraising target potentially a year early. At a time when areas of the alternative asset management industry are under pressure, the consistency of our investment discipline and performance stands out, and is increasingly recognised by our institutional clients.

0

bn

Periods of heightened uncertainty and volatility seem increasingly structural rather than episodic. Importantly, two of the challenges facing the industry today — liquidity strains within evergreen structures and exposure to businesses at direct risk of Al disruption — have limited direct impact on ICG. Our software exposure across the Group portfolio is approximately 10%, and even then only in highly cash generative businesses; while in private debt specifically, we do not have evergreen funds.

FY26 was a strong year for ICG. We delivered high-quality investment outcomes for clients and continued to grow flagship and scaling strategies.

Against this backdrop, I believe the managers who will succeed and gain market share are those with a long track record of proven investment discipline; who offer clients access to a breadth of asset classes; and who have built multiple levers of growth, while being flexible and suitably resourced to execute on new opportunities as they arise.

ICG possesses these characteristics.

Our culture is unequivocally focused on investment performance: this will drive long-term shareholder value

Steadfast investment discipline and consistency of investment performance through cycles will drive long-term growth and shareholder value, rather than AUM gathering at the inevitable expense of returns. The current challenges in parts of the alternative asset management industry are making this very clear.

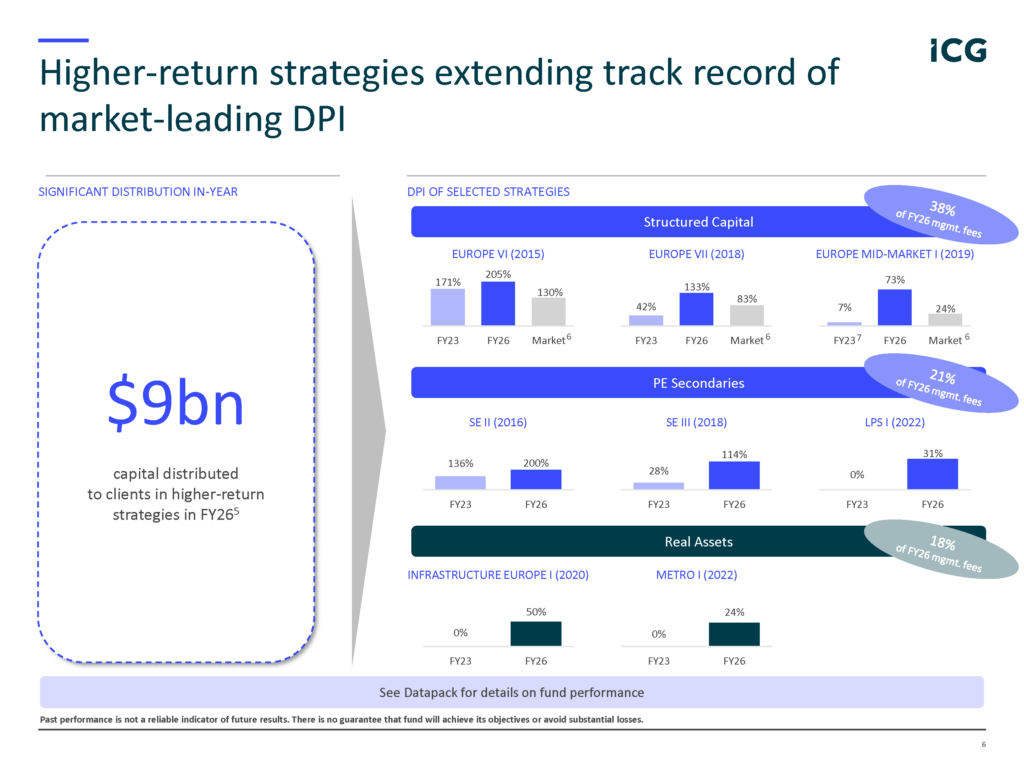

Investment performance starts with deployment and realisation discipline. The industry’s overall poor track record for returning capital, as measured by DPI metrics, in particular in recent years, has investors justifiably placing a high value on realised performance rather than potentially-optimistic NAVs. ICG’s industry-leading DPI performance across multiple strategies underpins our successful fundraising campaigns throughout this period.

Our investment committees drive this culture, and during the year these discussions have been some of the hardest in my memory. I continue to think pockets of equity valuations have more downside than upside risk, and credit terms remain very borrower friendly in most cases. Second- and third-order AI risk for many companies is likely to remain challenging to value for some time, and ongoing geopolitical conflicts add to the uncertainty of the economic outlook. Our downside-focused structuring expertise and our strong local origination capabilities ensure we can continue to deploy adequately while never compromising on risk.

Focus on long-term quality growth

We have deliberately built ICG as an engine for organic growth. This is only possible with a strong balance sheet and a long-term strategic vision.

Well executed, it is a powerful source of long-term per-share value creation. SDP (European direct lending) and Strategic Equity (GP-led secondaries) were both launched over a decade ago. Today they are large and highly profitable strategies, and we are looking forward to launching the sixth vintage of both in the coming months.

Today, Real Estate, Infrastructure and LP Secondaries represent emerging drivers of future growth for our firm, building on our flagship strategies within Structured Capital, GP-led Secondaries and European Direct Lending. Our scaling strategies are increasingly visible in our financial results, accounting for 19% of our management fees in FY26 compared to 13% in FY21. This year we have launched the second vintage of LP Secondaries, which has a strong fundraising pipeline, and we closed Infrastructure Europe II and Metropolitan II above their targets. This was no small feat in the current environment, and is a critical milestone: the success of second vintages is vital to cementing the reputation and position of a strategy and as a result, we can look confidently to meaningful growth in both strategies in the coming decade.

The opportunities for growth within ICG have never been as large or as diverse.

Address large investable markets to be relevant to all asset allocators globally

Strong and sustained institutional demand continues to underpin ICG’s growth. With $126bn AUM, we are large enough to be meaningful to all asset allocators while being nowhere near at capacity from the institutional market.

In the last 24 months, we have closed six funds at or above target against a sector-wide backdrop in which the total AUM raised in private markets globally is down 21% compared to 2021 and the number of funds raised has halved over the same time period1. Europe IX is on track to surpass its €10bn target which, would make it ICG’s largest ever commingled fund and the largest European structured capital fund ever raised globally at final close2. This underlines how ICG is gaining share in a sector that is continuing to consolidate inorganically and organically.

Today we serve over 870 institutional clients globally, up 11% over the course of the year. Among these we are proud to count six of the largest ten US pension funds and seven of the ten largest sovereign wealth funds, as well as hundreds more institutions who invest on behalf of their clients, customers, pensioners and employees to build wealth and financial security.

0

bn

The wealth market represents a large potential source of capital for private markets, but events in real estate in 2022 and in credit in recent months have made clear the challenges involved in designing and selling products that are intrinsically illiquid. I remain convinced that, adequately structured to preserve investment performance, alternative strategies can and should form an integral part of long-term wealth allocation.

For ICG, wealth capital accounts for 4% of our AUM today3. The partnership we signed with Amundi and our relationships with global private banks constitute an incremental source of long-term upside potential where investment strategies and product structures are aligned with our investment approach.

Ensure you have the necessary resources to withstand any market headwind and execute on value-creating opportunities

The financial results we are reporting today reflect the consistency of our approach. A clear focus on investment performance and a commitment to building scaled and relevant strategies have enabled us to grow organically in a profitable and cash generative fashion.

For the year ended 31 March 2026 we generated fee-related earnings (FRE) of £350m, equivalent to 120p per share and up 23% in the year. Over the last five years our FRE has grown at an annualised rate of 30%. We also recognised £127m of performance fee income in the year and generated £861m of operating cash flow.

With £1.5bn of available liquidity and net debt of £113m, our balance sheet has never been stronger, and it puts ICG in an excellent position to weather market uncertainties and to take advantage of opportunities that will inevitably arise.

This combination of performance, scale and financial strength positions ICG to continue to compound FRE per share by expanding the breadth and scale of the solutions we provide to our clients.

Even more important than financial resources, however, are our people and culture. Volatility and uncertainty are never comfortable in the moment, but history shows us that it is in these conditions that ICG’s teams do their best work: having the discipline to step back when risk is poorly rewarded, and the confidence to lean in where long-term value can be created.

I would like to thank all our colleagues for their commitment and judgement during the year. We continue to build ICG with a long-term perspective, focused on serving our clients and delivering sustainable value for shareholders. I am excited about the opportunities ahead and confident in our ability to execute on them.

Benoît Durteste

CIO and CEO

Notes

- Source: Bain Global Private Equity Report 2026.

- Source: WithIntelligence as of 7th May 2026.

- By % of third-party AUM, excluding CLOs and listed vehicles.

Authors