Article published with the permission of Secondaries Investor.

The secondaries market is at an inflection point in its evolution. As GP-led processes become more widely adopted, fi rms are increasingly fine-tuning their fund strategies to match.

Blackstone Strategic Partners, AlpInvest Partners and LGT Capital Partners are among firms that have launched or raised specific vehicles dedicated to GP-led processes, as a desire for strategy differentiation and eschewing concentration limits on exposure to single companies held in main funds runs through the market.

One firm that stands out from the pack is ICG‘s Strategic Equity team. The group has backed some of the largest and highest-profile single-asset continuation funds in recent years, including writing a €500 million cheque for a process involving nuclear medicine company Curium Pharma, managed by CapVest; investing $1 billion in a process on software company DigiCert, managed by Clearlake Capital; underwriting between $500 million and $600 million of a process for Waterland Private Equity portfolio company United Petfood, as well as other processes with TPG and Providence Equity Partners.

ICG’s predilection for taking highly concentrated bets of between $500 million and $1 billion on single companies has led some market sources to question how the group’s returns will fare.

“They are either going to be extremely right or extremely wrong,” says a lawyer who structures secondaries transactions and who has experience with the Strategic Equity team.

ICG is an exception in a market populated by firms that either initially focused on acquiring portfolios of LP stakes and then branched out into GP-led processes, or that are part of a recent crop of spin-out firms focusing solely on such transactions. The Strategic Equity team closed its debut fund in 2017 with a sole focus on GP-leds – this in a year when GP-led volume was just $14 billion, according to data from Jefferies, compared with $52 billion in 2022. The group’s fund went against the grain in a market traditionally characterised by the acquisition of highly diversified, passive portfolios of LP stakes.

The team’s initial incarnation comprised Andrew Hawkins, Ricardo Lombardi and Christophe Browne, who had all worked together at direct secondaries pioneer Vision Capital and who spun out, under Hawkins’ leadership, to form NewGlobe Capital in 2012.

In 2014, the trio joined ICG at the same time as it executed a GP-led transaction to acquire private equity assets from Diamond Castle IV, a vehicle managed by US-based private equity fi rm Diamond Castle.

ICG had spent “a couple of years” wanting to develop in-house capabilities to execute fund recapitalisations and structured deals, Benoît Durteste, now ICG’s chief investment officer and chief executive, told Secondaries Investor at the time.

“We didn’t see the benefit in duplicating a plain vanilla strategy, and there aren’t that many players in this space because it’s still emerging in the secondaries market,” Durteste said in 2014. “We were looking for an angle in the market where we could bring something different.”

Bring something different they did. When rumours began circulating in 2016 that ICG was attempting to raise $1 billion for a dedicated fund focusing on GP-led processes, numerous market sources expressed doubt to Secondaries Investor that LPs would back such a novel strategy.

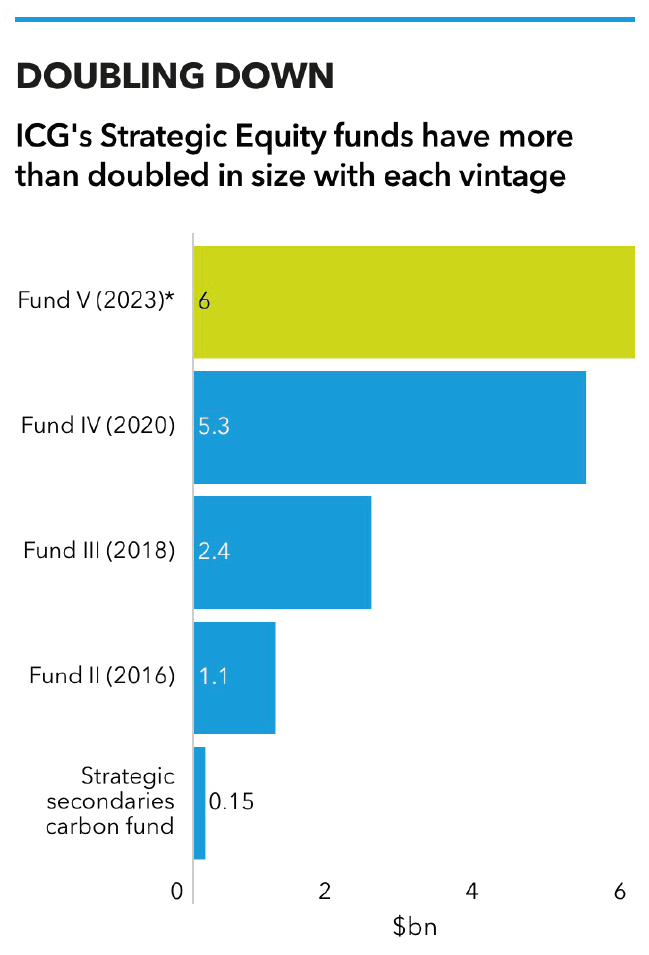

On the fundraising front, ICG has proved doubters wrong by more than doubling the size of its funds over successive vintages. Its debut offering, ICG Strategic Secondaries Fund II, beat its $1 billion target by closing on $1.07 billion, attracting commitments from investors including Royal County of Berkshire Pension Fund and Syracuse University, according to Secondaries Investor data.

Its follow-up fund, Strategic Equity III, raised $2.41 billion in 2020, taking it 50 percent higher than its $1.6 billion target, according to Secondaries Investor data. SE III delivered a 2.3x gross multiple on invested capital and a distributed to paid-in capital return of 27 percent as of September, according to ICG earnings documents.

Last year, the group raised $5.3 billion for its latest vehicle, Strategic Equity IV, beating its $5 billion target. The fund remains the industry’s largest dedicated pot of capital for GP-led secondaries and focuses solely on single-asset deals. It had a 1.6x MOIC as of September, according to the same earnings documents, and is understood to have been 86 percent committed as of November.

The group has now brought on a former Blackstone Tactical Opportunities managing director, Andrea Serra, to lead Strategic Equity in Europe. Serra, who joined last year, spent 15 years at Blackstone and worked on deals including the acquisitions of sustainable materials manufacturer Sustana Group and International Market Centers, an owner and operator of premier showroom space.

Secret sauce

ICG is wasting no time getting back to market. On its earnings call in November, Durteste identified Strategic Equity V as a fund that could launch before the end of the financial year, noting that the vehicle “finds itself in a sweet spot of the market, with very significant supply-demand imbalance”. Secondaries Investor understands that Fund V is targeting $6 billion.

A spokesperson for the firm declined to comment on fundraising.

How did a team with a direct investing background go from raising the industry’s first $1 billion GP-led focused fund, to managing the world’s largest dedicated pool of capital for sponsor-initiated processes? From conversations Secondaries Investor has had with secondaries market sources, ICG’s strategy appears to be based on a combination of being an outlier by fund size, having a risk appetite for highly concentrated deals, and having figured out a formula for processing and executing on deals that’s irresistible to the gatekeepers of dealflow: the market’s intermediaries.

“Their secret sauce is: ‘Give us two weeks to run due diligence and prepare a term sheet’,” says another lawyer familiar with how ICG operates. “After that, you’ll have a clear no or a clear yes. If it’s a yes, we’ll take the whole thing.”

This strategy, which Secondaries Investor understands ICG refers to as the ‘sole buyer’ concept, appears to have struck a chord with advisers.

“Bankers love it because they have execution certainty,” says the second lawyer. “Instead of every buyer saying ‘we’ll take $150 million’ and having to do that six times, they just have the one buyer.”

This approach has created a situation that appears to be beneficial for both ICG and intermediaries. Advisers bring deals to ICG first because they know they can get a clear answer within days, and if ICG wants the deal, it will back the whole transaction, resulting in less work for time and resource-restrained intermediaries, according to multiple sources. In turn, ICG benefits from being the first buyer that intermediaries call when they have a large single-asset transaction, and this gives ICG the upper hand when structuring and negotiating terms, the lawyer sources say.

Source: Secondaries Investor

Leading the Strategic Equity team is Lombardi, 40, whose conviction and belief in ICG’s strategy is palpable. Over breakfast with Secondaries Investor at a London restaurant last year, Lombardi was so focused on discussing his team’s history and strategy during an hour-long meeting that he left without having touched his meal.

Lombardi became global head of the group last summer, with former global head Hawkins moving to a vice-chairman role and North America co-head Browne stepping down to spend more time with his family.

“From day one, our plan has been to build the category killer for GP-leds, and to do that we knew we had to build a team with buyout backgrounds, and have a fit-for-purpose mandate from our LPs,” Lombardi tells Secondaries Investor.

“The model is very simple,” he adds. “Is it a quality asset in a quality industry? Is the valuation attractive and is the GP strong and truly aligned? Quality asset in a quality industry and an attractive valuation, plus a strong and aligned GP – if you don’t have all those things, move on.”

While the group’s initial funds did back multi-asset GP-led deals, it shifted to single-asset processes because it feels that it’s via these processes that it can generate buyout-like returns with a shorter time duration. The group tells its LPs its target returns are a 2x money multiple and a 25 percent internal rate of return, both on a net basis, according to a source familiar with the unit’s strategy.

“We thought that trade-off [single-asset versus multi-asset deals] made a lot of sense, because you’re prioritising quality over number of assets,” Lombardi says. “We thought that from a competitive point of view, you had to really be a specialist because you’re effectively underwriting a buyout.”

When Secondaries Investor puts to Lombardi what it has heard about the group’s strategy of attempting to monopolise deals, he confirms it.

“If you’re the GP, you’re dealing with ICG Strategic Equity, and we are delivering the transaction as a one-stop solution. That is different from having to assemble one or two lead buyers and then having to go and find multiple additional buyers to build a syndicate, which is still standard practice in the market for large transactions where we are not involved.”

This isn’t to say that ICG will ultimately speak for all the equity capital needed to back a single-asset transaction – the firm does offer co-investment on the deals it backs to its LPs.

The group has won accolades from readers of affiliate title Private Equity International’s PEI Awards for its Icon continuation fund processes with Clearlake – of which ICG backed the Santa Monica-headquartered firm’s first three iterations.

The unit has also backed transactions that some may consider to be on the more exotic side of the spectrum. In 2018, it closed a deal to restructure a 2006-vintage Central and Eastern Europe-focused fund managed by PineBridge Investments spin-out ForeVest Capital Partners; that same year, it invested in a near-$1 billion spin-out of an Asia and emerging markets portfolio from Standard Chartered Private

Equity.

In 2021, it backed a GP-led transaction with Ukraine’s Horizon Capital, in which select assets were moved out of the Kyiv-headquartered firm’s 2008-vintage Emerging Europe Growth Fund II and into a continuation fund named Horizon Capital Growth Fund II. The European Bank for Reconstruction and Development, which invested $10 million in the continuation fund, has published details of the transaction.

As of February, the Strategic Equity team, which takes board seats on the companies it backs – sometimes in a purely observational role – is understood to have never lost money on a transaction, including the Horizon GP-led.

The road ahead

The ICG Strategic Equity team of today looks somewhat different to the team of yesteryear. If recent deals are a guide, the group is focusing on sectors such as education, healthcare, cybersecurity and pets in the developed markets of North America and Western Europe. Its original leadership trio now comprises just Hawkins and Lombardi, with the latter at the day-to-day helm. And while parent organisation ICG has built a separate team to invest in LP portfolios, its Strategic Equity team is doubling down on concentrated GP-leds.

For how long will Lombardi’s group enjoy its first-mover advantage in large single-asset GP-leds? Most likely until one of its competitors truly scales. Already, the market’s second- and third-largest dedicated GP-led funds have been raised, both this year: in January, Blackstone’s secondaries unit closed on $2.7 billion for its debut GP-led focused fund as part of a total $25 billion programme for secondaries, while in February, Morgan Stanley Alternative Investment Partners said it had raised $2.5 billion for its sophomore GP-led focused fund, Ashbridge Transformational Secondaries Fund II.

For now, Strategic Equity appears to occupy a relatively uncrowded part of the market both by strategy and fund size, underwriting six or seven deals per year with little direct competition.

As former North America co-head Browne told Secondaries Investor in 2020: “Our peers in the traditional secondaries market really thrive on diversification. We’ve never shied away from complexity or concentration.”

LPs considering backing the group’s next vintage will be weighing up its ability to deliver on a secondaries strategy in which picking winners is more important than ever.