Updated on 11 November 2025, adding a video: Why have markets and economies been so resilient and is this likely to continue?

Corporate balance sheets at an aggregate level remain strong, corporate default rates have been trending down and are forecast to continue to decline, global economic growth remains healthy, systemically important banks are well ring-fenced, and household balance sheets as a whole are strong (see charts below).

Most indications are that the recent company bankruptcies and losses faced by a few US regional banks are idiosyncratic in nature (i.e. company and bank specific), with limited broader implications for the systemic health of credit markets. It appears that fraud may have played a key role in driving the First Brands and Tricolor bankruptcies, with both companies operating in niche sectors (auto parts and subprime auto loans) known to be under stress.

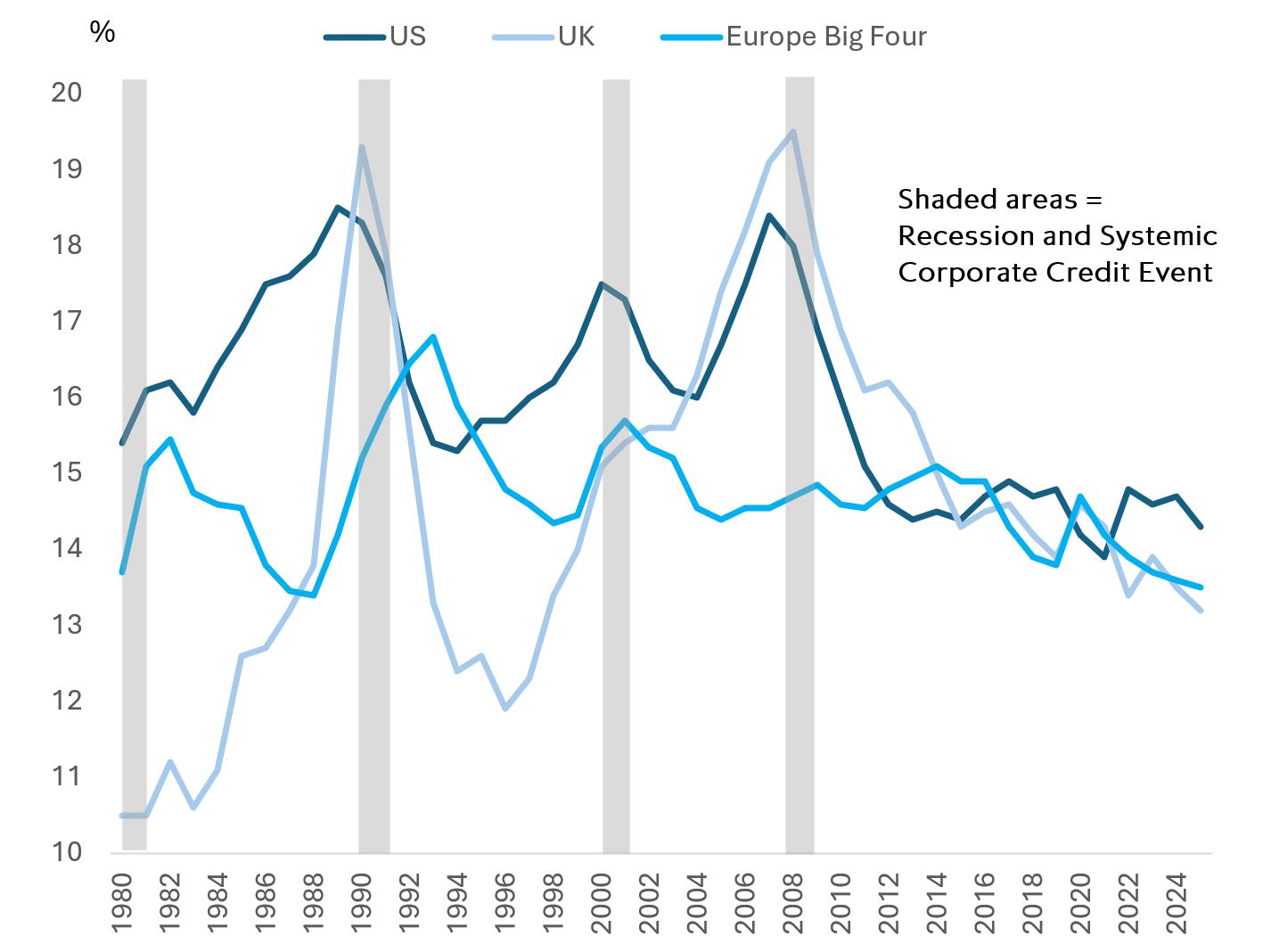

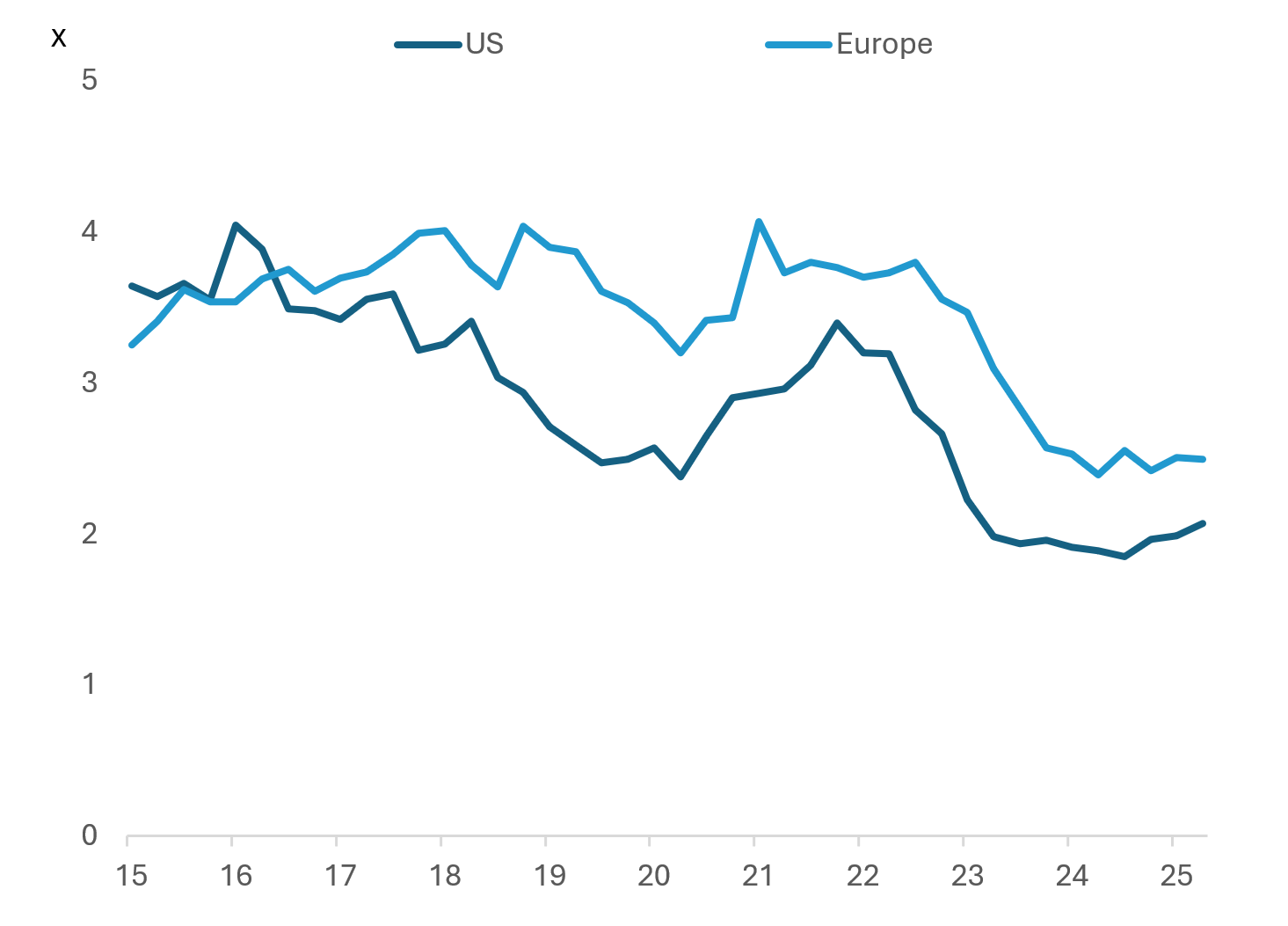

Aggregate corporate debt service ratios in the US, Europe and the UK are falling and are well below 2008 levels, indicating limited systemic risk in the sector.

Aggregate data from the Bank for International Settlements (BIS) shows that corporate debt service ratios (interest and principal payments as a percent of income) in the US, Europe and the UK are falling and remain well below 2008 levels. On their analysis (“Aggregate debt servicing and the limit on private credit”), corporate debt service ratios provide “highly accurate early warning signals” for systemic financial crises. On their most recent data this risk appears low (see chart below). In addition, household debt service ratios are also well below 2008 levels and have been declining, indicating household balance sheets remain strong, which should help keep a floor under private consumption.

Corporate debt service ratios low and falling

Systemically important banks are protected and economic growth is resilient

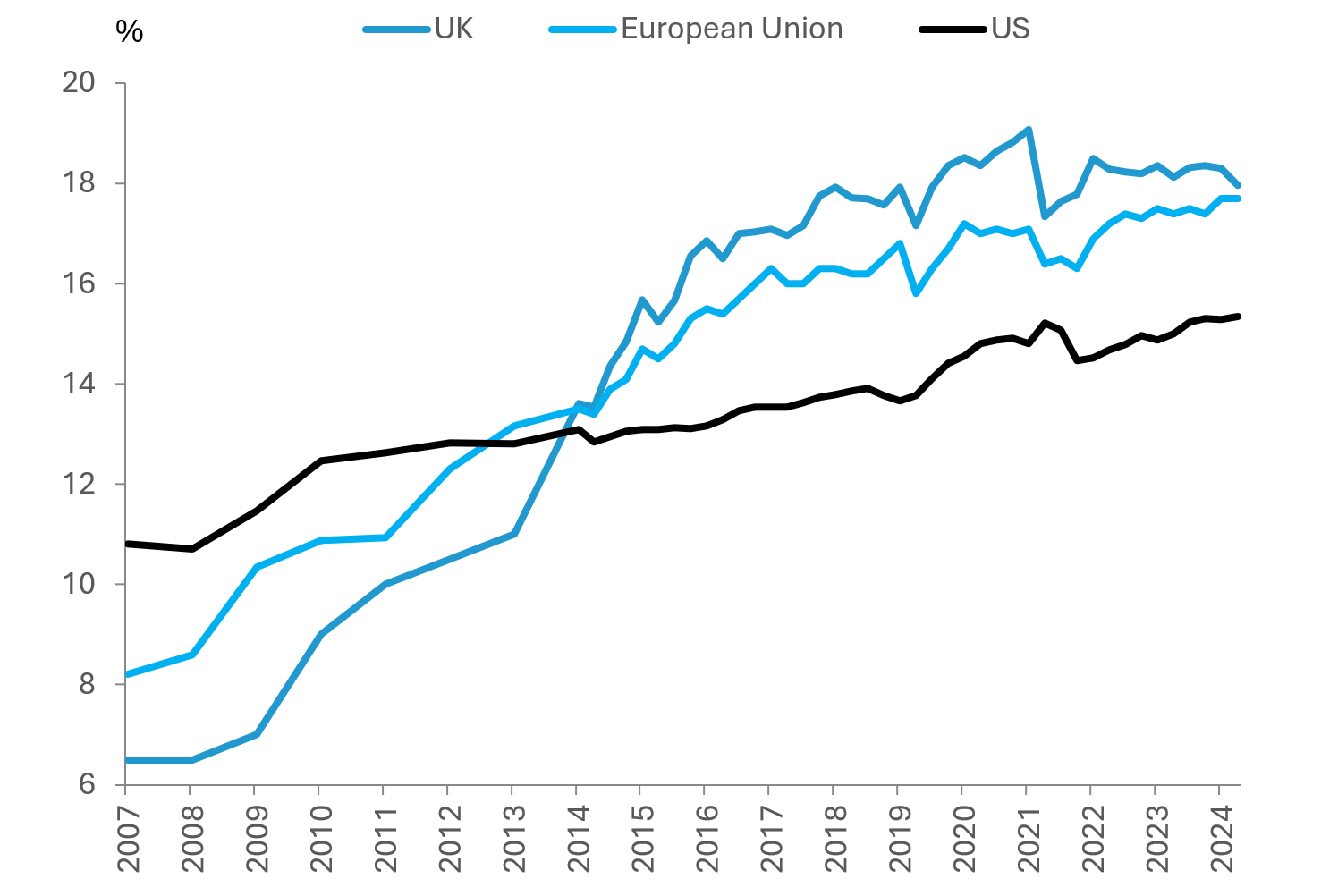

Systemically important banks remain well protected, with banks’ tier one capital ratios significantly higher than in the run-up to the 2008 global financial crisis and regular stress tests ensuring they are well buffered from potential external shocks. Tier one capital for the systemically important banks in the US, Eurozone and UK currently stand at around 15%, 18% and 18% compared to 10%, 8% and 6% in 2007.

Banks’ Tier One Capital Ratios highlight balance sheet strength of systemically important banks

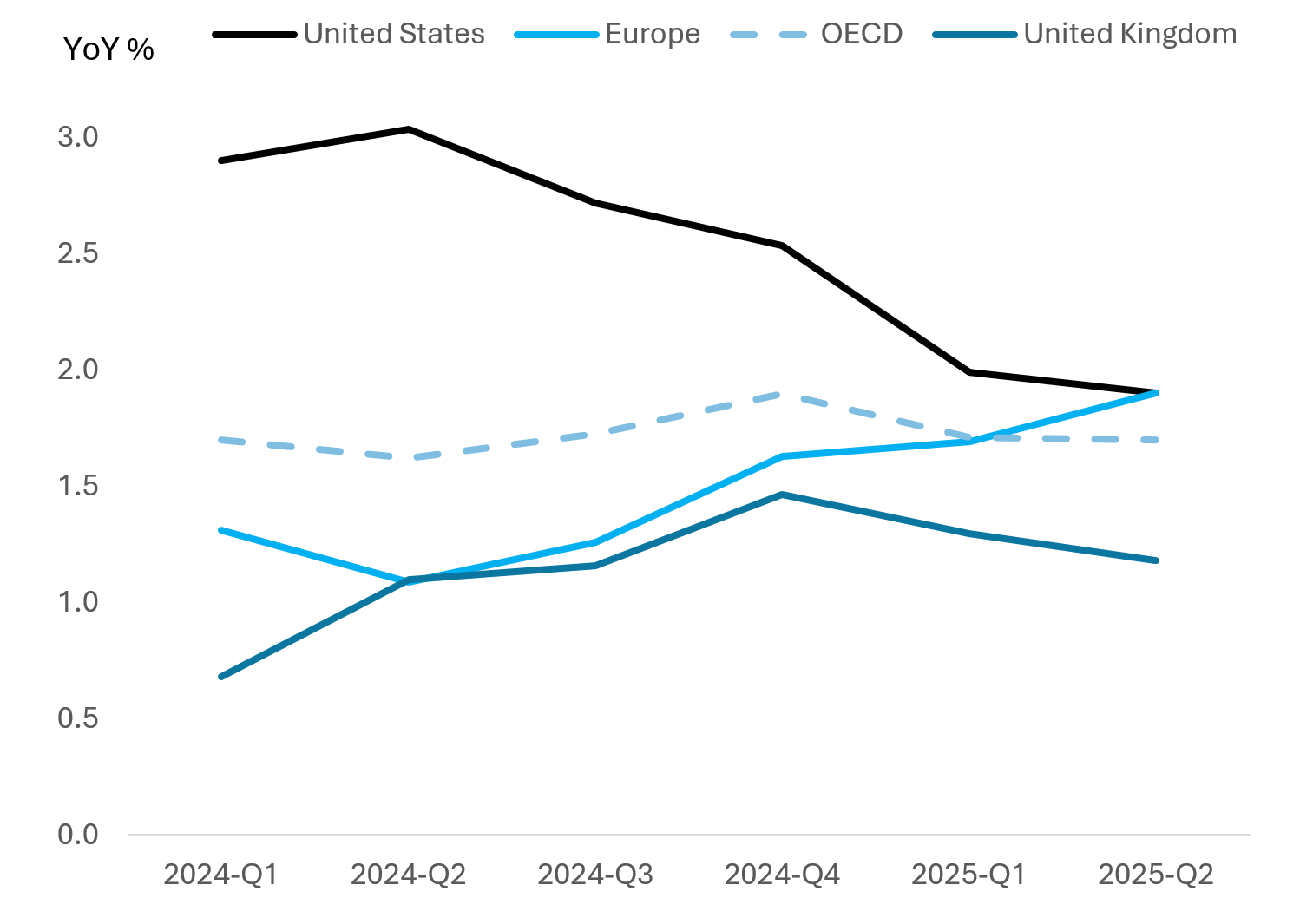

The US economy has continued to grow at a healthy pace despite political and policy uncertainty, with US GDP expected to grow by 1.8% in both 2025 and 2026 according to consensus estimates. Europe, UK and other major developed economies also continue to show positive growth. This should provide a continued constructive operating environment for businesses.

Global economic growth remains resilient, with the US and other major developed economies continuing to grow at a healthy pace despite political and policy uncertainty.

Resilient global GDP growth

In addition, the US Fed has cut its benchmark rate 125bp from its high in 2024 and the swap market is pricing a further 125bp of cuts to 3% over the next twelve months. The ECB has more than halved its benchmark interest rate to 2% over the past year and the swap market is pricing around 50bp of rate cuts from the Bank of England over the next twelve months. Rate cuts should support growth and further reduce companies’ funding costs.

Declining default rates and robust debt service ratios

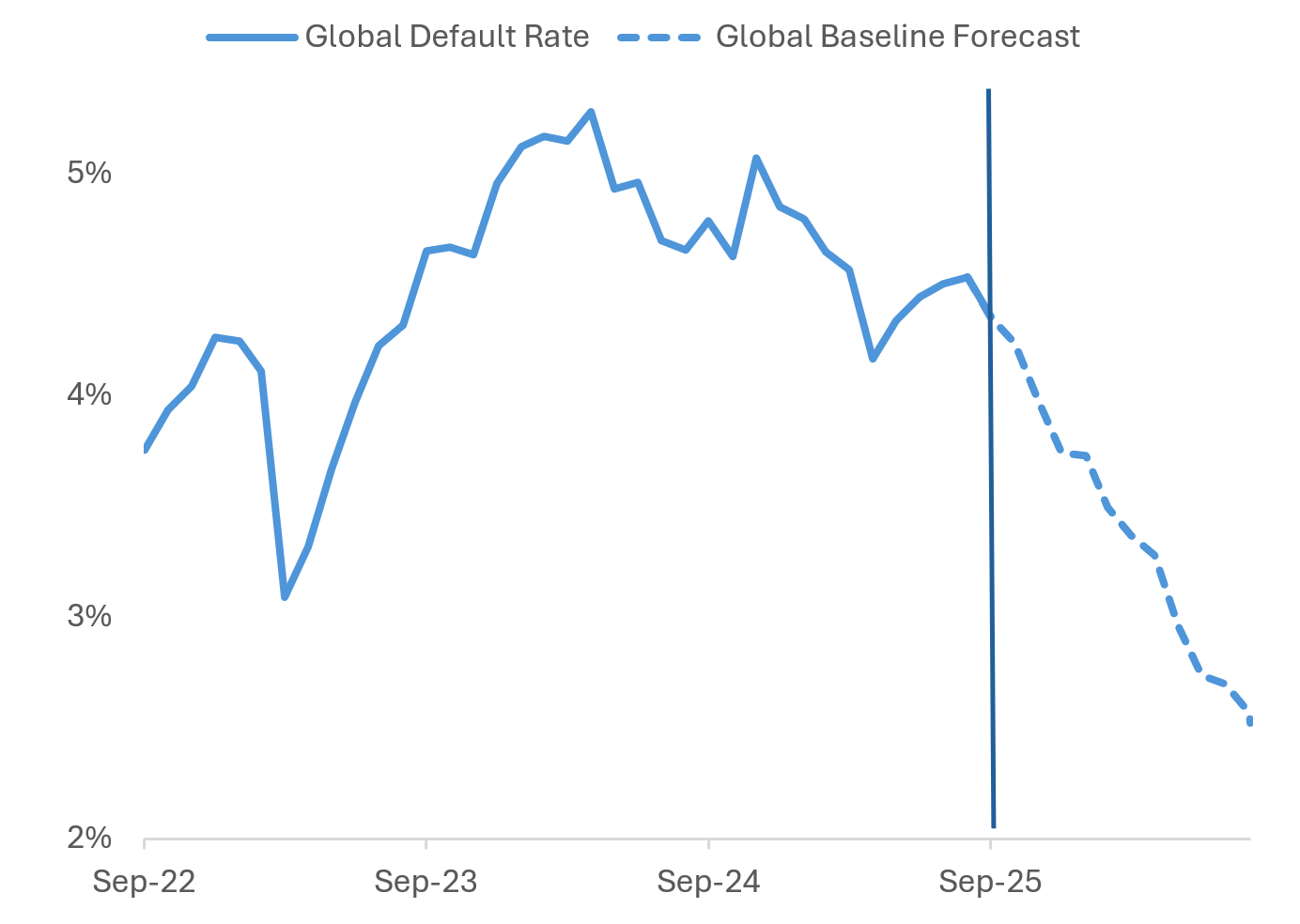

Moody’s data shows that the global speculative grade default rate has been declining over the past year and Moody’s baseline forecast is for the default rate to decline from around 4% currently to around 2.5% over the next year (see chart below).

Moody’s global speculative grade default rate and baseline forecast

Strong private company fundamentals

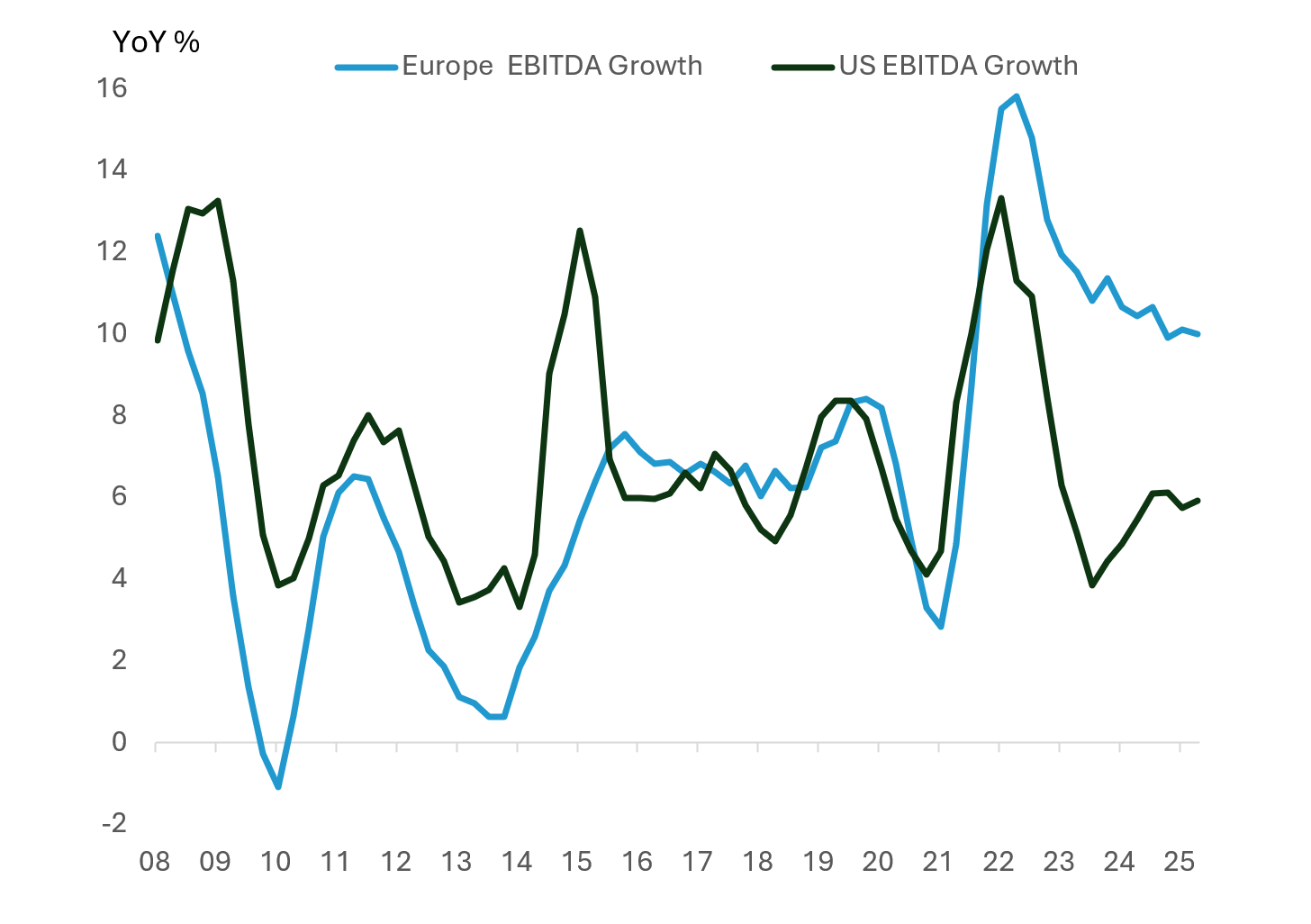

Data from ICG’s proprietary private company database indicate that private company fundamentals at an aggregate level remain strong, with median EBITDA growth of both Europe and US companies growing at a healthy pace and interest coverage ratios stabilising at comfortable levels.

US and Europe EBITDA growth holding up well

US and Europe Interest Coverage Ratios at comfortable levels

Therefore, while there is always scope for further idiosyncratic problems at a company and bank-specific level, macro conditions and measures of systemic risk indicate recent concerns about the broader financial system are overblown.

While there is always scope for further idiosyncratic problems at a company and bank-specific level, macro conditions and measures of systemic risk indicate recent concerns about the broader financial system are overblown.

Watch video

Why have markets and economies been so resilient and is this likely to continue?

In this short film recorded on 29 October 2025, Nick assesses current structural macro and credit market fundamentals, key risks to the outlook and what current conditions may mean for investors broadly and private markets investors in particular.