Solid foundations

In this 8th bi-annual edition of the ICG Private Company Trends report, we provide an in-depth view of the key fundamental trends we are seeing across this historically opaque segment of the market and assess the outlook for the rest of 2022 and 2023.

Email [email protected] to request a copy of the full report.

Key findings include:

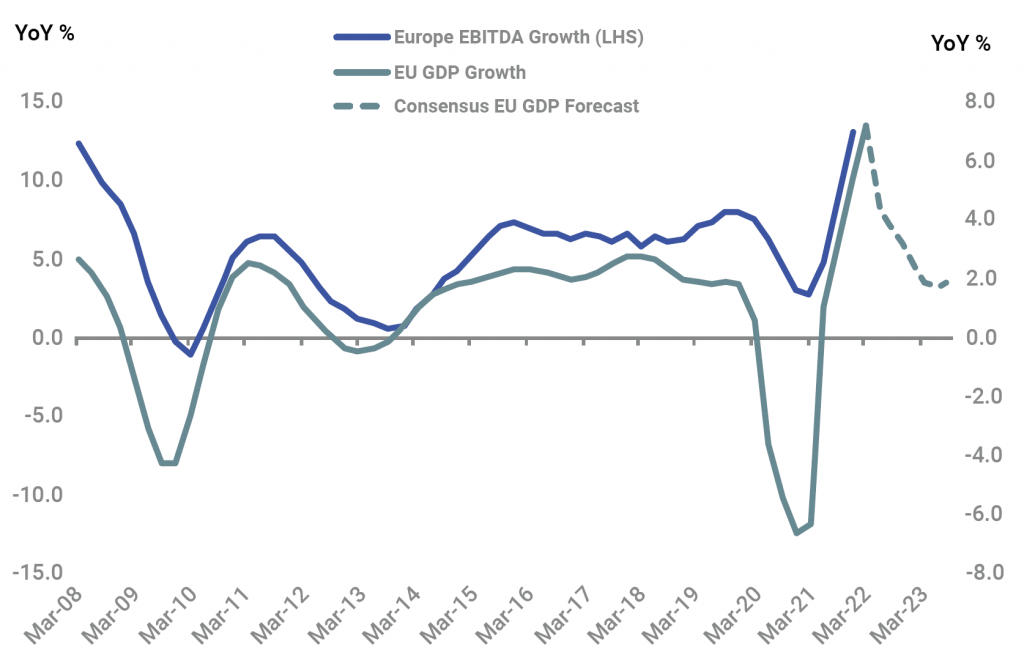

- Private companies had their strongest year on record in 2021, as re-opening boosted revenues and earnings, leverage fell and interest coverage rose

- All sectors performed strongly, with consumer discretionary seeing the strongest rebound as consumer demand for hospitality and leisure related activities surged

- The operating environment going forward is likely to become more difficult as slower growth, higher interest rates, continued high input costs and supply chain bottlenecks provide challenges

- Performance dispersion is likely to remain high with healthcare, technology, business and financial services likely to be less negatively affected than energy and supply chain-sensitive heavy industry, aviation, autos, building materials and big-ticket consumer discretionary

- Solid foundations should help offset the coming headwinds. Reduced leverage, comfortable interest coverage, large equity cushions and strong earnings momentum should help buffer private companies. Strong consumer and bank balance sheets, high household savings and more activist government fiscal policy should also provide support in the coming quarters.

Slower growth ahead