Overview

The good news is that global growth has proved much more resilient than expected. The not so good news is that resilient demand has slowed the disinflationary process, forcing the Fed to keep its policy rates higher for longer than most market participants expected. Looking forward, although we expect the lagged impact of sustained high interest rates and a reduced fiscal impulse will lead to a weakening of US demand growth and inflation pressure, it now appears that rate cuts in the US will come later and be more cautious than markets were expecting earlier this year. Europe and the UK, by contrast, appear to be a an inflection point, with growth picking up at the same time as easing underlying inflation pressure is paving the way for early rate cuts.

Key trends

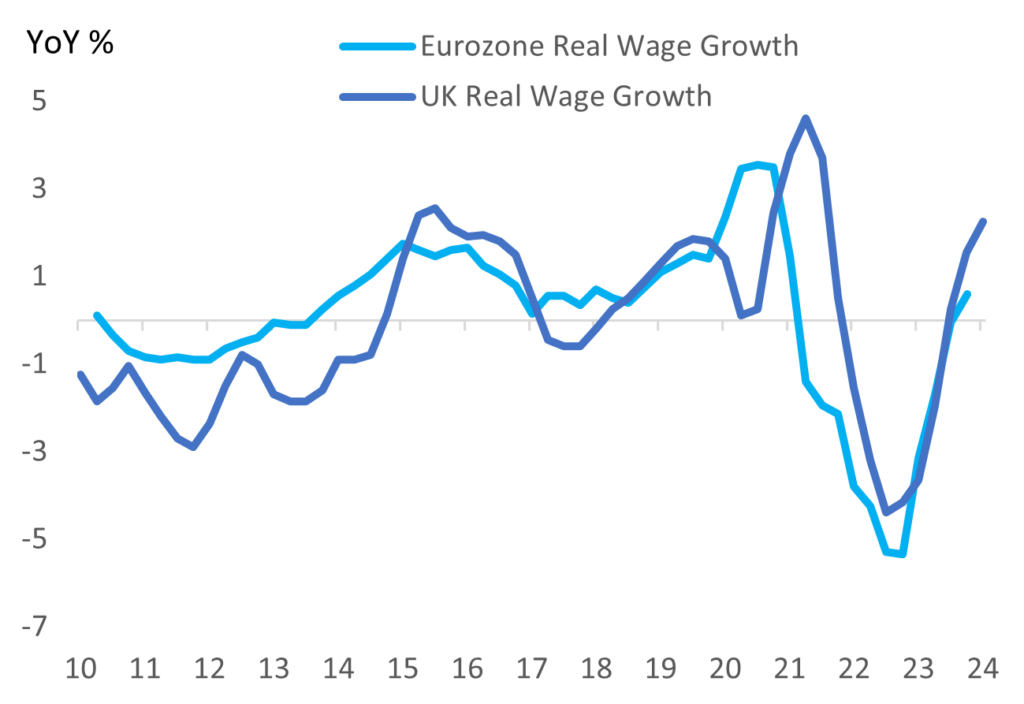

- Europe and UK economies starting to pick up. Recent macro data indicates that after over a year of lacklustre economic growth, growth momentum in continental Europe and the UK is starting to pick-up. GDP growth in Q1 rose across all major economies and purchasing manager indexes, and other high frequency data indicate the growth rebound has continued into Q2. Rising real incomes on healthy wage growth and falling prices are supporting private consumption, while a rebound in the global industrial cycle and a normalisation of energy prices and supply chains should support investment and export growth going forward. Falling interest rates should provide further growth support later this year and into 2025.

- Resilient US economy delays Fed rate cuts. The main theme of the past few quarters has been consistent outperformance of the US economy relative to Fed and consensus expectations. Some of the main drivers of this outperformance include far more expansionary fiscal policy than expected, a substantial easing of financial conditions despite Fed rate hikes, and consumers running down savings at a more aggressive pace than expected. All these factors are likely to moderate in the coming quarters, allowing the US economy to slow to a more sustainable pace and the Fed to start cutting rates later this year.

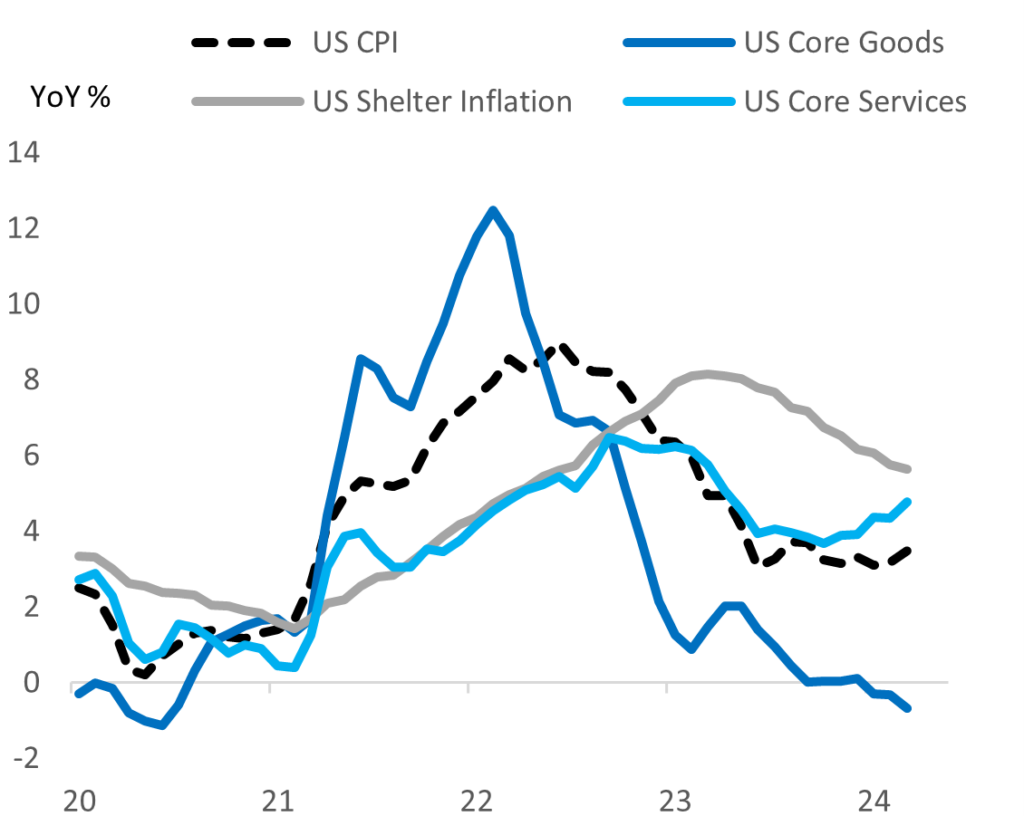

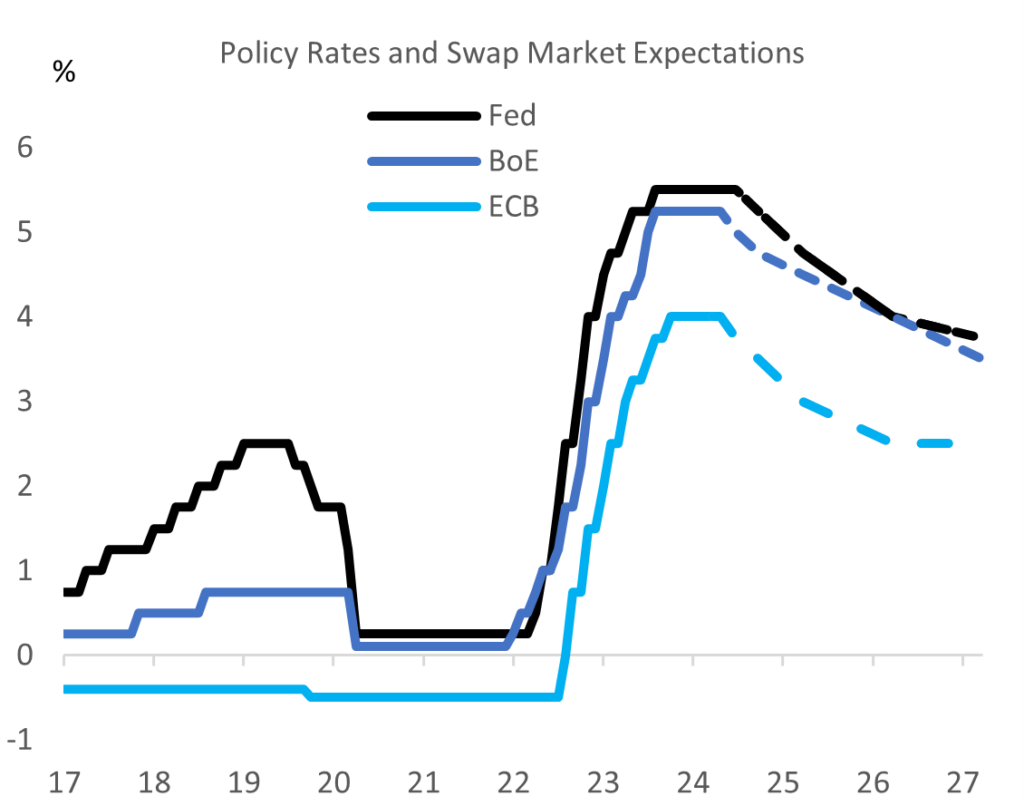

- Diverging inflation trends lead to diverging monetary policy trends. Although resilient US growth has been positive for companies’ top-lines, a negative side effect of the sustained period of above potential growth has been slower than desired progress on inflation – with services inflation proving particularly sticky due to (partial) pass-through of high wage growth. While lead indicators point to an easing of US labour market tightness, slow progress likely means Fed rate cuts are delayed until the autumn. Europe by contrast, following a period of below potential demand growth, has seen core inflation pressure ease more quickly, with ECB rate cuts likely to start in June and the BoE likely followingly shortly behind.

- Global event risk remains high. Although economies and markets have so far remained resilient, there are multiple risks that could change the current relatively benign investment landscape ranging from potential spillovers into energy markets from the Israel-Hamas war, Putin’s continued war in Ukraine, a watershed US election in November and potential for an escalatory trade war with China among many others.

- Implications for investors. In this environment of positive but sluggish growth and lower but still high interest rates, company performance dispersion is likely to continue to widen, with pricing power, cost control, balance sheet management and access to capital likely to remain key performance differentiators. In our view this should continue to favour investors with medium to long-term investment horizons, strong bottom-up analytical capabilities, the ability to provide flexible capital and work closely with portfolio companies to provide support through a continued volatile macro and geopolitical environment.

Europe and UK growth picking up

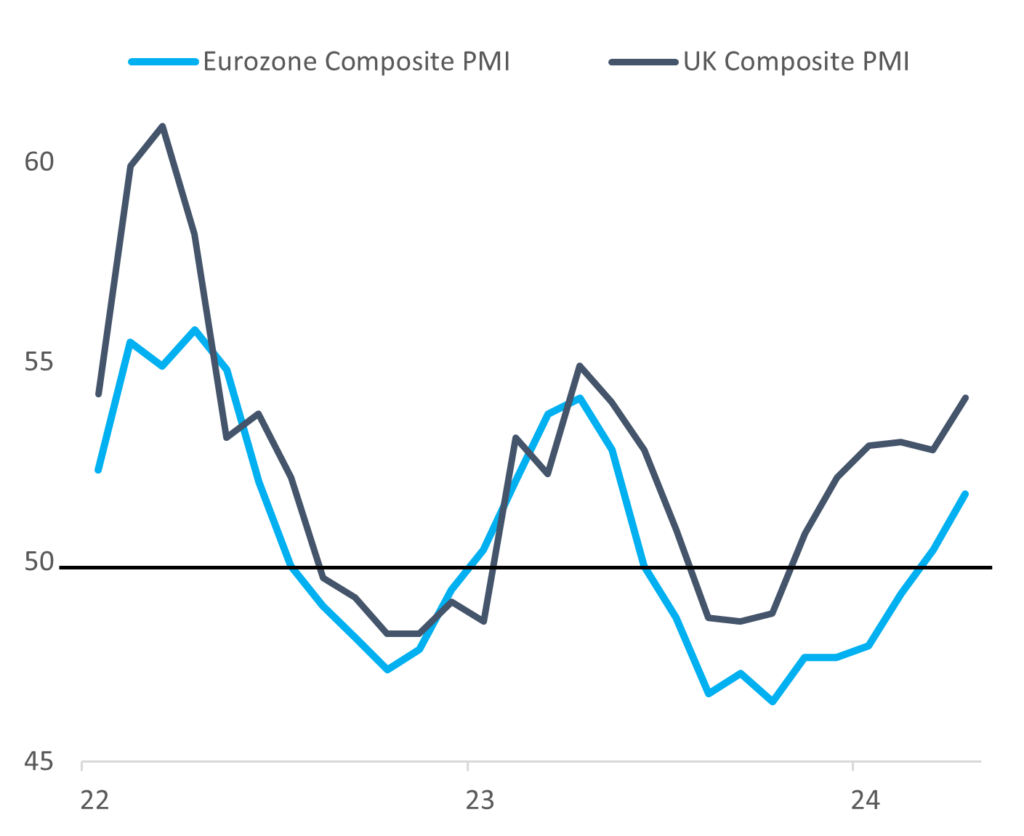

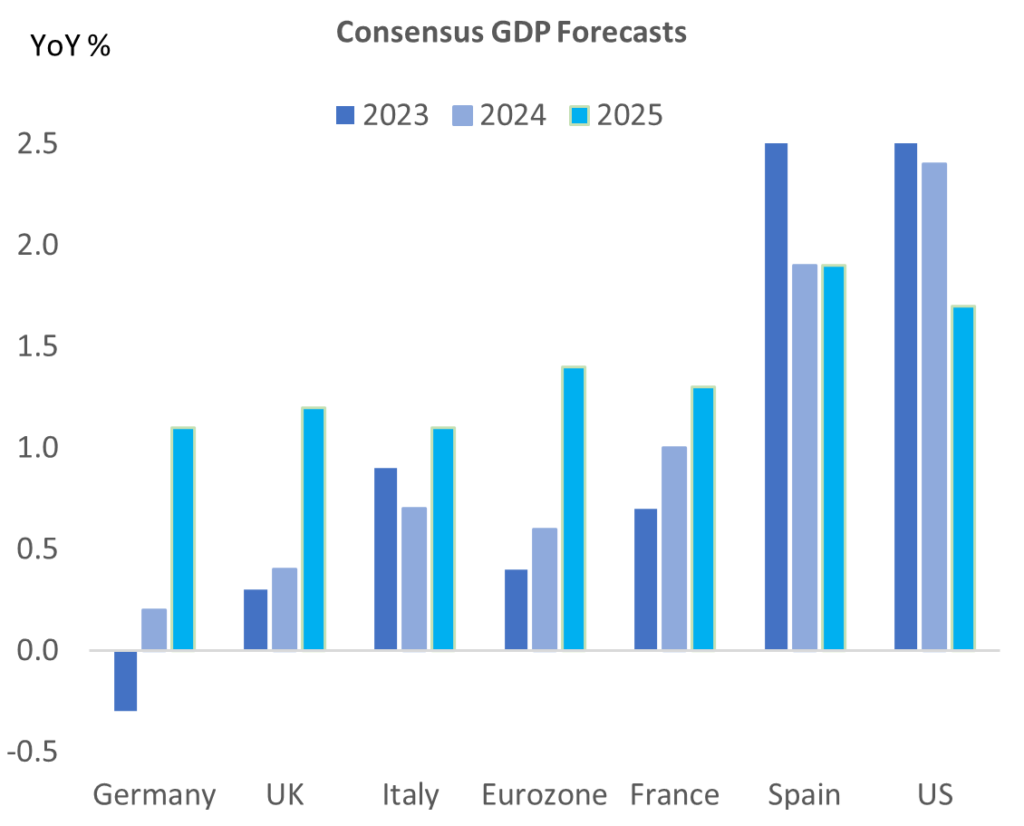

After a period of lacklustre growth, there are signs economic activity in Europe and the UK is picking up. Eurozone GDP in Q1 rose 0.3% on a quarterly basis following two consecutive quarters of negative growth in 2H 2023. Leading indicators point to further gains ahead, with the region’s composite PMI rising to 51.4 in April, its second consecutive month in expansionary territory. Services remain the main growth driver, with the services PMI on a steady rising trend since October last year. The manufacturing sector has remained weak, but leading indicators of the global industrial cycle point to a rebound in growth later this year and Europe is likely to be a key beneficiary. UK growth has started 2024 on a strong note, with GDP rising 0.6% in Q1, its fastest growth since 2021, and the composite PMI on a steady uptrend since October, rising to a strong 54.1 in April indicating the momentum has continued into Q2.

Europe and UK growth momentum picking up

Europe and UK real wage growth turn positive

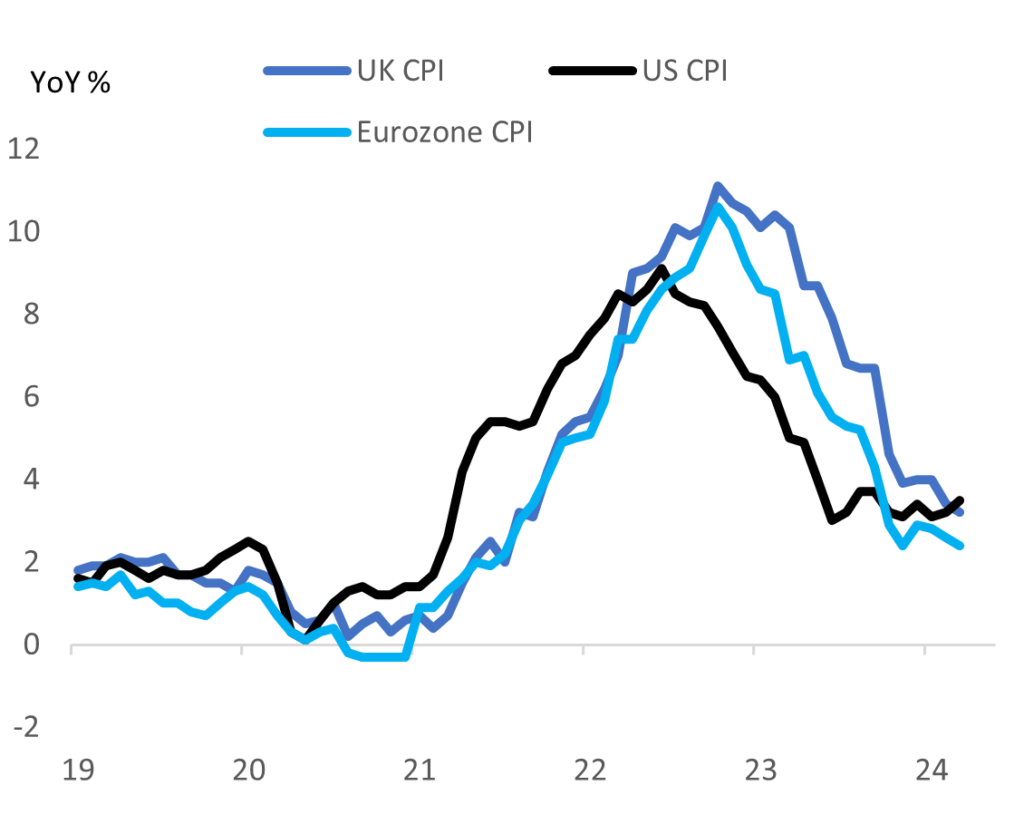

Inflation in Europe and the UK are also moving in the right direction, paving the way for rate cuts

Eurozone core HICP fell to 2.7% in April, its ninth consecutive month of decline. Likely of particular comfort to the ECB, most high frequency indicators of wage growth across most Eurozone countries have continued to show moderation through Q1 2024. This should allow the ECB to move ahead with its first interest rate cut in June, with markets currently pricing in another two 25bp cuts by year end. The UK has also seen inflation pressures ease, with core CPI falling to 4.2% in March. Further declines are expected in the coming months, likely paving the way for up to three 25bp cuts by year end, starting in June or August.

Falling inflation puts ECB in position to cut rates first

Resilient US growth delays rate cuts

The resilience of US domestic demand to the sharp rise in the Fed funds rate and heightened geopolitical uncertainty over the past two years has surpassed all expectations and is the main reason inflation has not come down as quickly as the Fed and most market participants have expected. While most commentary has focused on the negative inflation and interest rate implications of sustained strong economic growth, the silver lining for investors is that strong domestic demand has supported healthy top-line growth, allowing companies and markets to perform well despite continued high interest rates.

US services inflation proving to be particularly sticky

What’s behind the resilience of US domestic demand?

One key factor driving US economic resilience is a highly stimulatory fiscal policy. The IMF estimates the US ran a general government deficit of 8.8% of GDP in 2023, the largest deficit on record other than during periods of war or deep recession. In addition, consumers, largely protected from rate increases due to fixed rate mortgages, continue to spend as employment and real disposable income growth remains strong. Adding fuel to the fire, the easing of financial conditions in Q4 2023 and Q1 2024 as bond yields fell and risk markets discounted anticipated large rate cuts in 2024 (the “Powell pivot”), also supported growth.

Swap markets pricing relatively shallow rate cut cycle

Where do we go from here?

Barring a major shock, such as a sharp rise in oil prices or a sustained risk asset sell-off, US consumers resilience appears set to continue. Although the fiscal impulse may lessen, on IMF numbers the US is expected to run a still-sizeable fiscal deficit of around 7% of GDP in 2024 and 2025 (by contrast, Europe is expected to run deficits of less than half this level). On top of this, an upturn in the global industrial cycle may provide further growth support. Therefore, although we expect demand growth moderation and continued supply side improvements will reduce underlying inflation pressure, improvements are likely to be gradual and bumpy. This will likely constrain the Fed to one, or at the most, two rate cuts this year..

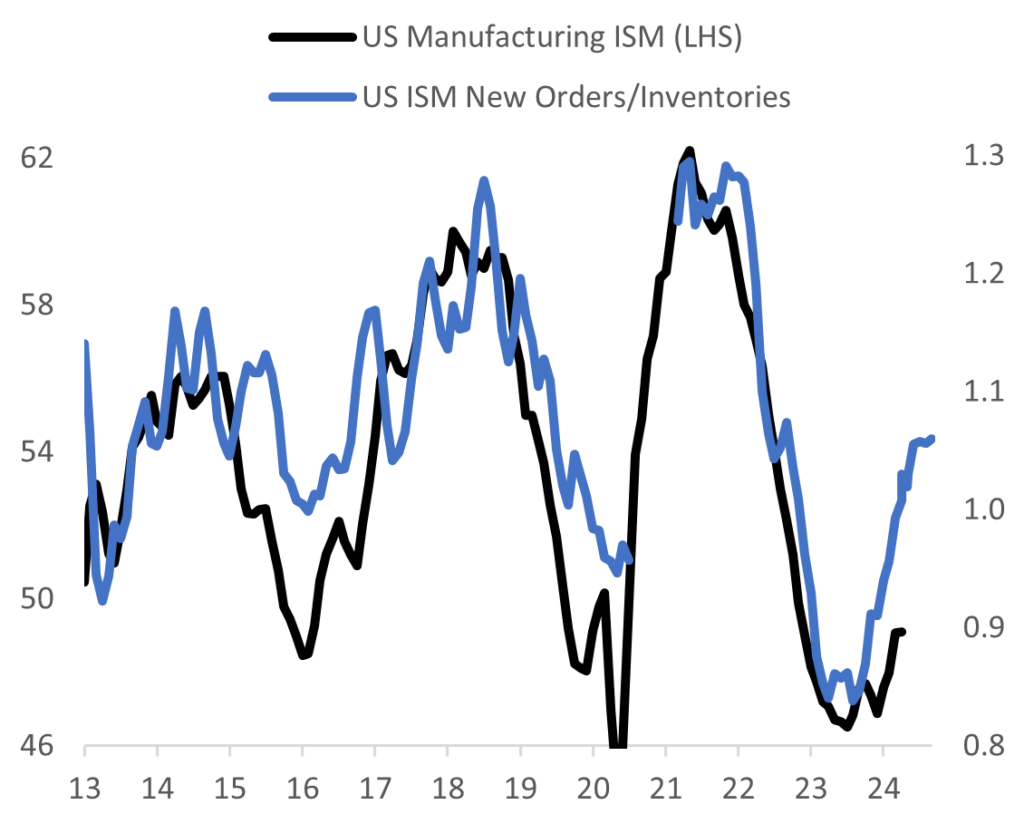

Signs the industrial cycle is starting to turn up

Gradual growth recovery expected to extend into 2025

Implications for investors

A positive consequence of a more resilient US economy and a rebound in Europe growth this year is that companies should see continued healthy top-line growth. However, with rates and input costs likely to stay higher for longer, the ability to navigate high interest rates, maintain pricing power and manage costs will likely continue to be key performance differentiators in 2024 and into 2025.