Developed economies and markets outperformed expectations in 2025 despite geopolitical shocks and higher US tariffs, with growth holding firm, inflation falling and major central banks cutting policy rates. With the war in the Middle East and the closure of the Strait of Hormuz continuing to drag on, the question is whether this resilience will continue.

Highly resilient financial markets – so far

Oil prices up sharply, natural gas prices less so

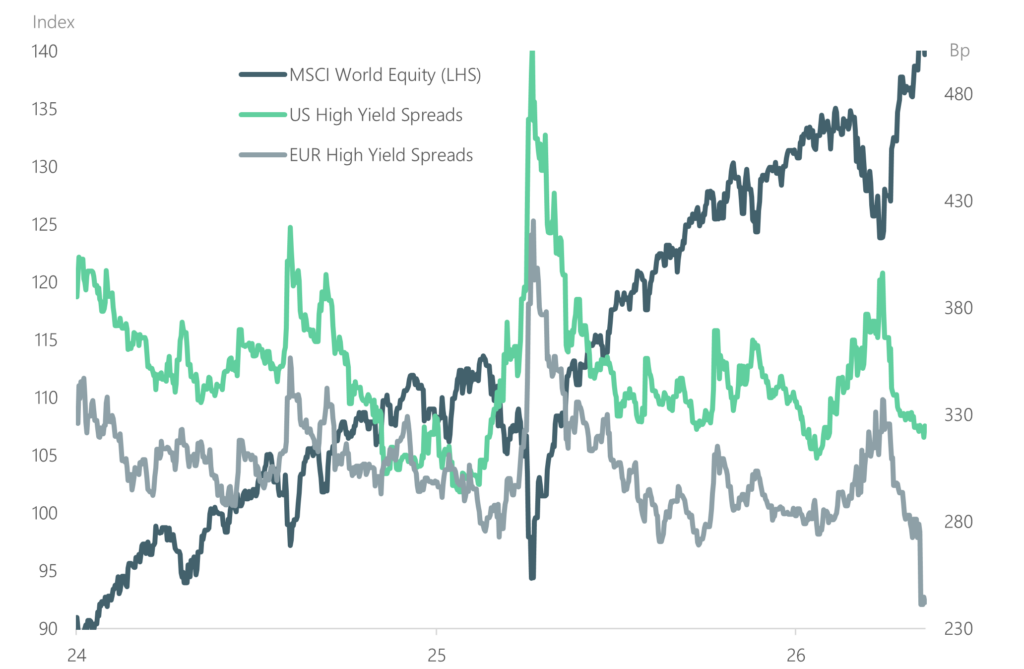

Markets have so far shrugged off the surge in energy prices

Risks to the outlook have risen as energy prices have surged on the back of the war in the Middle East. In addition, recent concerns about the potential for AI to disrupt the business models of a number of sectors, software in particular, have added to the uncertainty.

So far, markets have mostly shrugged off the surge in energy prices, with the S&P 500 hitting new all-time highs and most other major equity benchmarks and high yield spreads back near pre-war levels.

Risks rising as stalemate drags on

The likely main reason for the resilience is the general belief that both the US and Iran have strong incentives to end the war sooner rather than later, most hard economic data has held up well so far, and company earnings through Q1 2026 have been strong. There are, however, risks to this benign scenario.

While it is clear President Trump wants the war over and energy prices down as quickly as possible with US mid-term elections scheduled for November, the Iranians are harder to read.

With the US naval blockade now cutting off the regime’s main source of revenue, the risk of renewed attacks by the US and Israel rising, and having proven to the world that attacking Iran is not costless, the regime also has strong incentives to end the war. However, it appears there are competing factions within Iran with a range of views on acceptable terms for a peace agreement. The main risk to energy prices, and therefore the economic and market outlook, is that the Iranians cannot agree amongst themselves on acceptable peace terms, or they decide it is worth taking more pain in order to inflict more global economic damage and thereby increase their bargaining power and deterrence against future attacks.

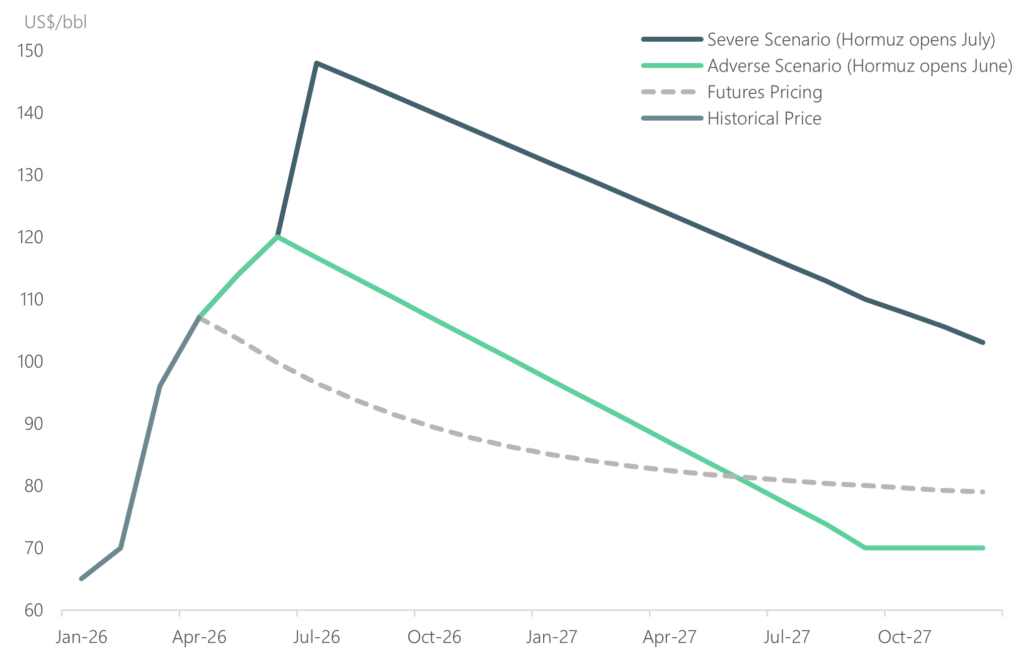

Quantifying the potential impact of a “severe” scenario

This then leads to two connected questions: 1) What impact will a longer closure of the Strait of Hormuz have on energy prices (and related products); and 2) What will different levels of energy prices have on the global economy? In an attempt to try to quantify the potential impact (to the extent it can be quantified), we’ve taken analysis from a variety of sources. Firstly, linking Hormuz closure times to oil inventory drawdowns and price scenarios and then secondly, using estimates from the ECB and other sources, try to quantify the potential impact various levels and durations of high energy prices may have on economic growth and inflation.

Oil price scenarios based on timing of Strait of Hormuz reopening

Clearly there is a lot of uncertainty around these estimates, but it gives a framework for trying to gauge how different scenarios may affect major economies.

On these analyses, even in a “severe” scenario where the Strait of Hormuz is not reopened until July, the analyses indicate the impact on most major developed economies would be relatively mild compared to the major economic dislocations of recent history and relatively short-lived, with growth rebounding and inflation forecast to fall in 2027.

Of course, the impact on some sectors and companies has the potential to be more severe.

Macro impact of a “severe” scenario

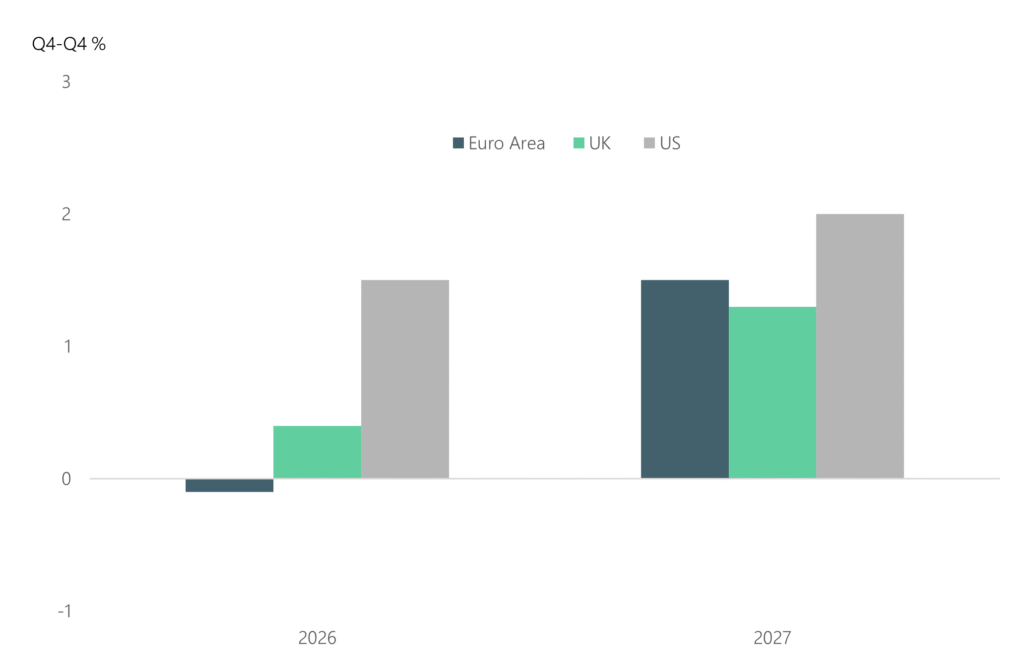

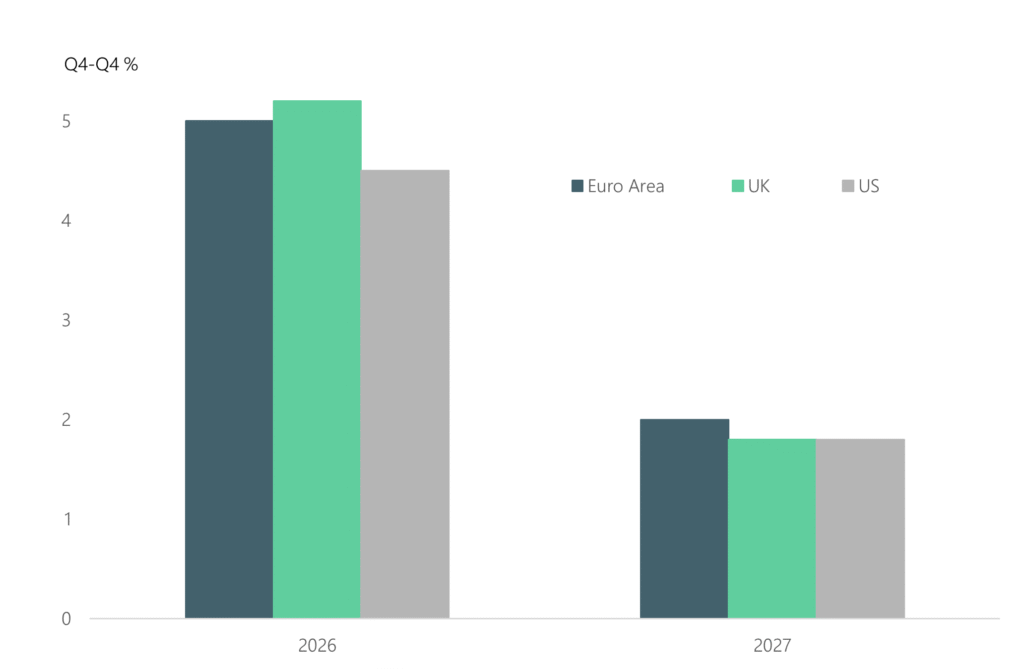

Estimates by the ECB indicate that even if the Brent oil price rises to near $150/bbl and stays above $100/bbl in 2027 and the natural gas price peaks at €106 per MWh (price is currently around €47), the Eurozone economy would see only two quarters of modestly negative growth before bouncing back in 2027. Most investment banks and other private sector modelling indicates that in a similar oil price scenario, both the US and UK would see slower but still positive growth (see charts below).

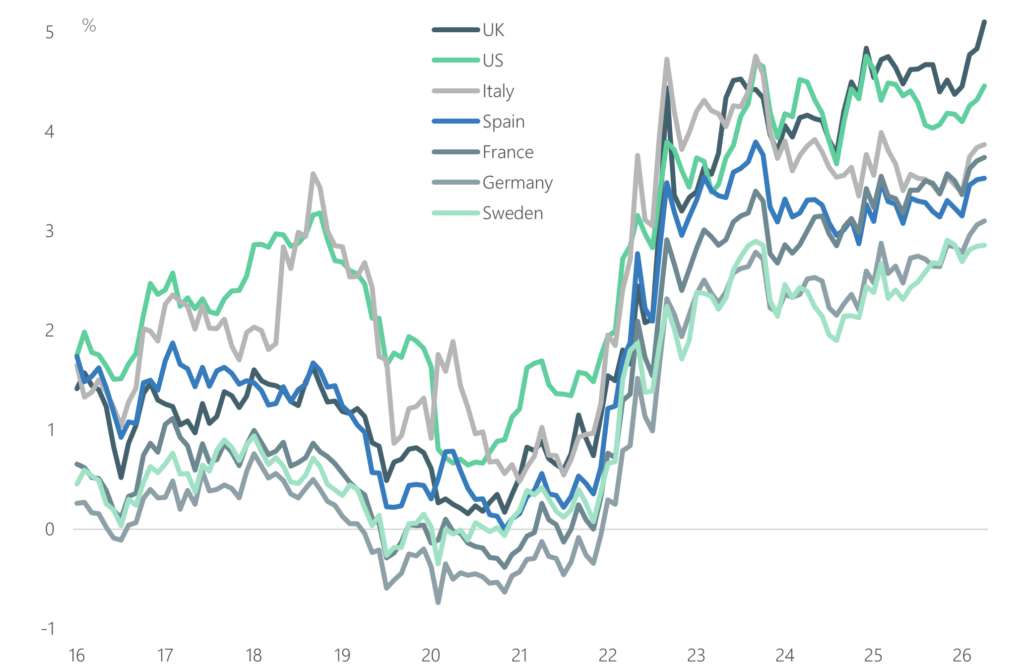

Under the more severe scenario, headline inflation would rise sharply but, unlike the situation in 2022, slack labour markets, lack of monetary accommodation and less scope for companies to pass-on price increases, is forecast to limit core inflation increases and make it less likely there is a repeat of the 2022 sustained inflation surge scenario.

GDP under “severe” scenario, forecast to rebound in 2027

Inflation under severe scenario forecast to normalise in 2027

Not a repeat of 2022: Central banks are not accommodating price increases

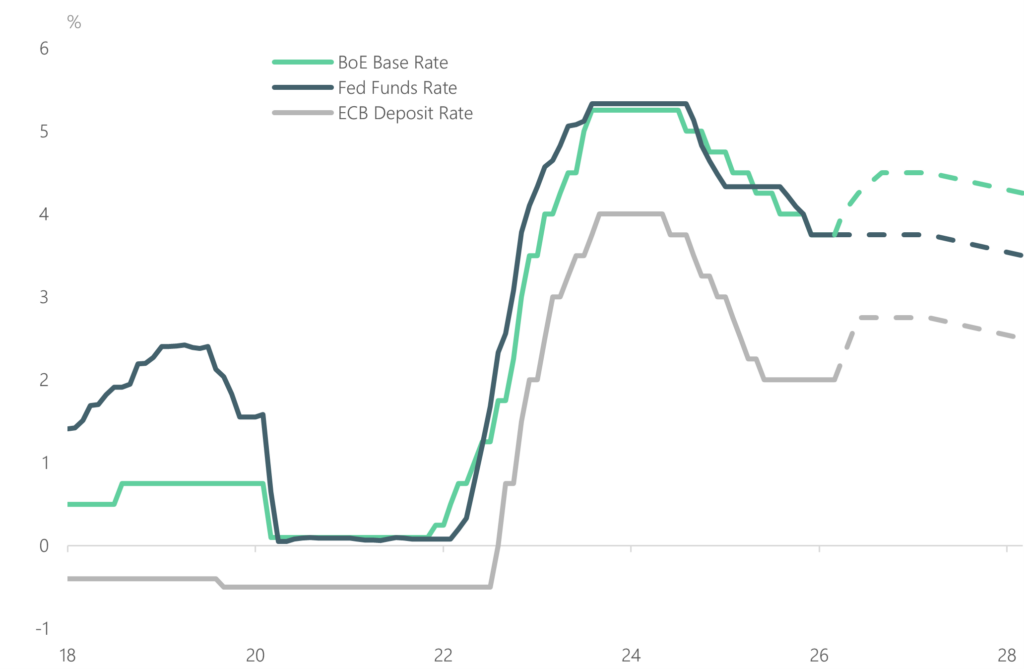

Therefore, while central banks will likely lean hawkish in the coming months to try to keep inflation expectations under control, rate hikes of the scale of 2022 are unlikely. Swap market pricing is for the Fed to keep rates flat through 2026 and the ECB and BoE to raise their policy rates by 25bp three times each in 2026. Even on the severe scenario outlined above, rate hikes of this magnitude would seem unnecessary. Assuming energy prices start to normalise in 2H 2026, it is likely that central banks will be in a position to start cutting rates again later in 2027. Longer maturity government bond yields, however, are likely to stay high given growing fiscal funding needs and a higher inflation risk premium. In our view the US is particularly at risk given the size and current trajectory of its government debt burden.

Policy rates may rise, but not by much

Government bond yields likely to stay high

Implications for private company fundamentals

On the above scenarios, the operating environment for many companies will likely become more difficult but should be manageable. Top lines may see some pressure later in 2026 as growth slows and, depending on the nature of the business, margins may also see some pressure as costs are more difficult to pass on than in 2022. Despite the likely more difficult operating environment, even in the “severe” situation outlined above, in our view, overall structural fundamentals should remain resilient.