Overview

- Developed economies and markets outperformed expectations in 2025—robust growth, falling inflation, and lower interest rates despite geopolitical shocks and higher US tariffs.

- Europe to benefit from fiscal expansion, monetary easing, lower energy prices, and positive real income growth; impact of US tariffs limited and manageable.

- Economic resilience set to continue in 2026, supported by strong household, corporate, and bank balance sheets, as well as easier fiscal and monetary policy.

- Biggest threat: potential turmoil in US government debt market amid high deficits and no credible plan for stabilisation; possible ripple effects through risk assets but likely offsetting central bank interventions.

- Sustained US government debt concerns could trigger further US dollar weakness and gold price upside, as investors grow uneasy with the US fiscal trajectory.

- Private market investors remain well positioned—solid company fundamentals and less-cyclical sector focus insulate against public market volatility, but careful selection is crucial as idiosyncratic risks rise.

Strong economic and market performance in 2025—but will it continue in 2026?

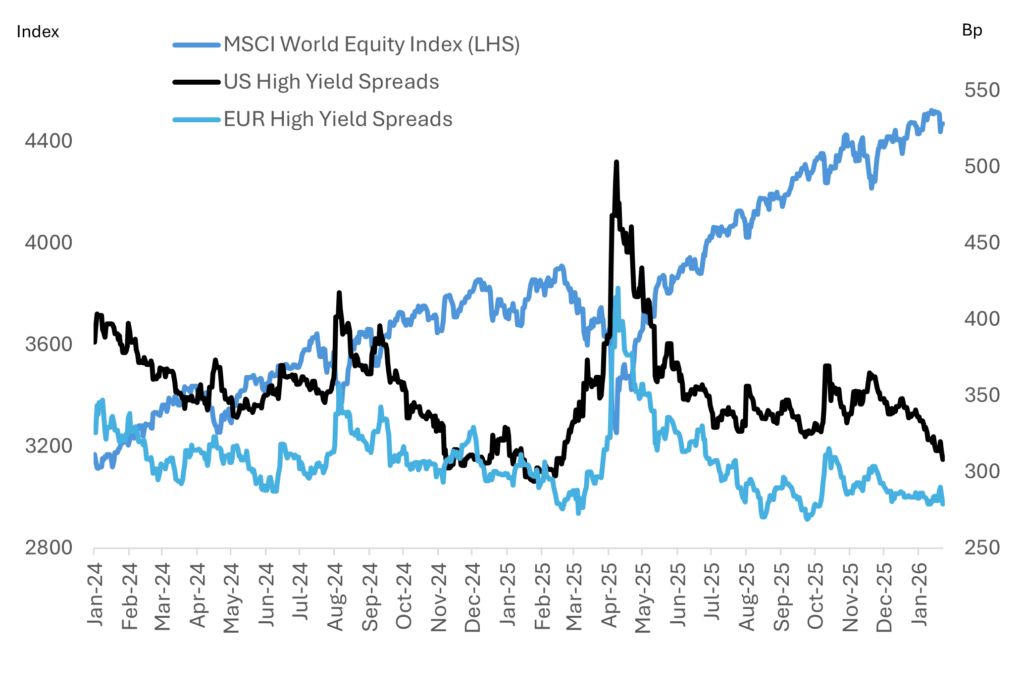

Despite geopolitical upheaval and the sharp rise in US import tariffs, the US, Europe, and UK economies are estimated to have grown by a better-than-expected 2.0%, 1.6%, and 1.4% in 2025, with inflation falling to 2.7%, 2.0% and 3.2% respectively. Resilient growth, resilient earnings and falling inflation and interest rates helped drive risk assets higher, with the S&P 500, Euro Stoxx 600, FTSE 100, and most other major market equity benchmarks ending the year near all-time highs and credit spreads tightening back towards historic lows.

Strong growth and falling rates have supported markets

Although the risk of market volatility remains elevated, we think private markets investors will remain relatively sheltered.

Economic resilience to continue

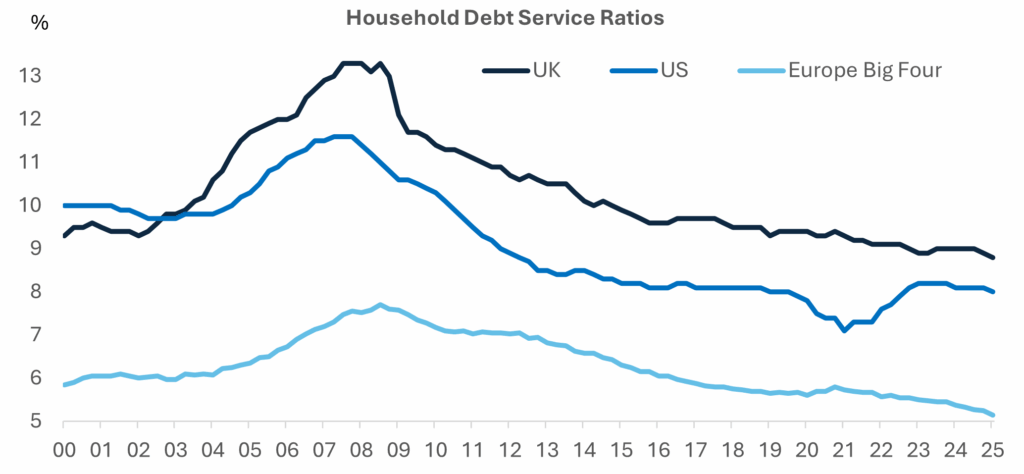

While economic growth across most major economies will likely face headwinds from continued high geopolitical and US policy uncertainty in 2026, we think the economic resilience of last year will continue in 2026. Strong aggregate company, household, and bank balance sheets, together with stimulatory fiscal policy and lower interest rates in the major developed economies should provide strong buffers to downside growth risks and provide a continued stable operating environment for private companies in 2026.

Strong household balance sheets provide downside growth buffer

Potential turmoil in government debt markets biggest risk to markets in 2026

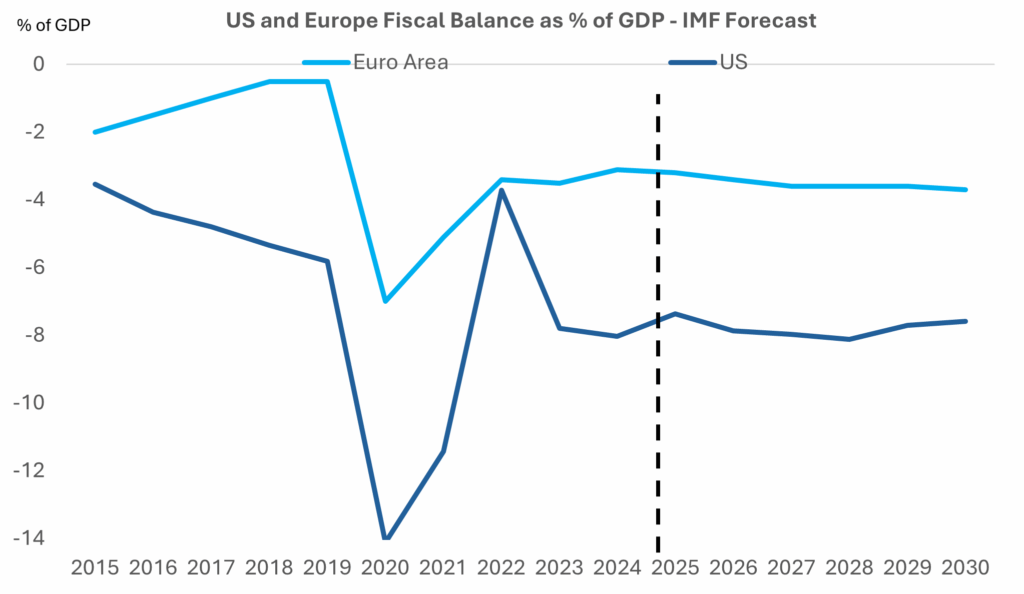

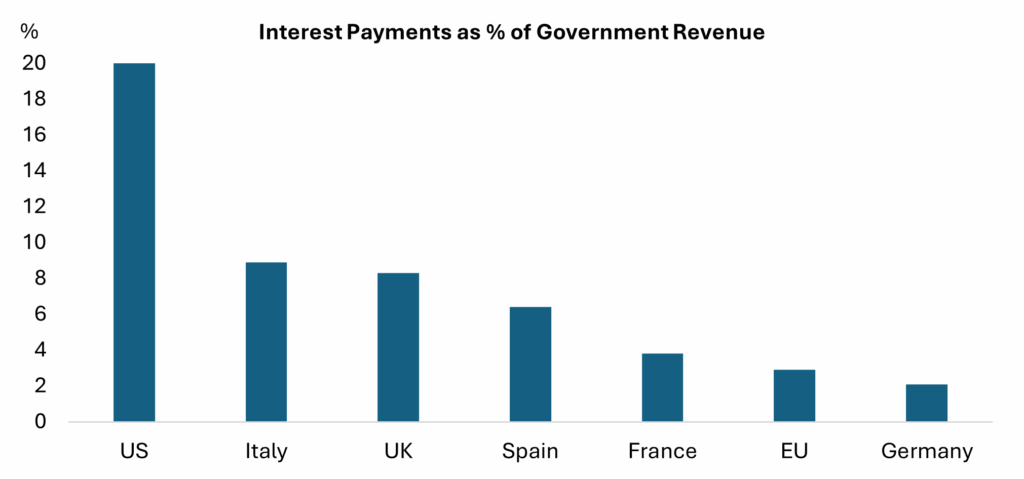

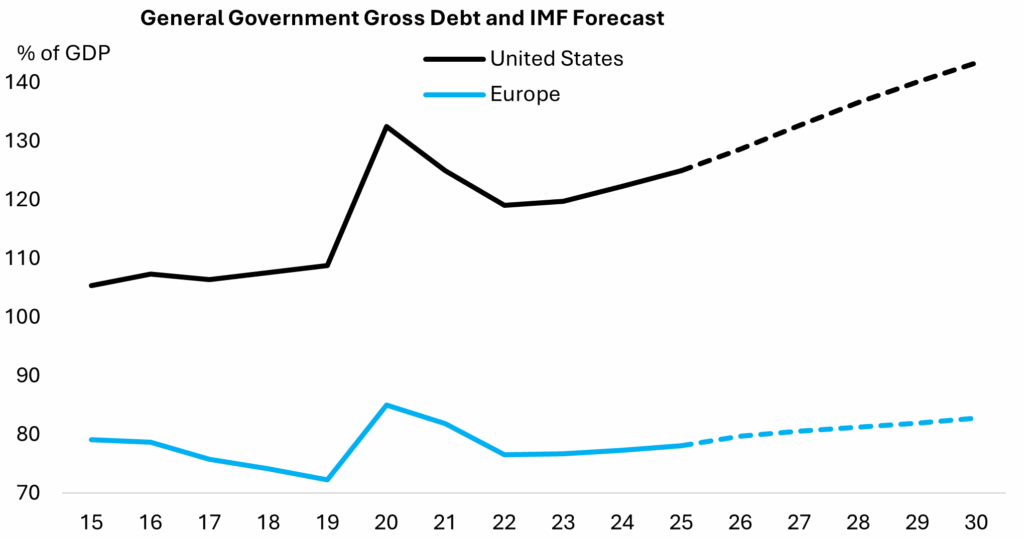

In our view, one of the biggest risks to markets in 2026 is the risk of turbulence in government debt markets that ripples through to other asset classes. The US is a particular risk in our view, given that it has been consistently running fiscal deficits in the 7%–8% of GDP range (based on IMF data) in recent years, debt to GDP is currently at its highest level since World War Two and—most critically—there is currently not a credible plan to rein in US fiscal deficit and the US government debt level.

Unsustainable US fiscal deficits

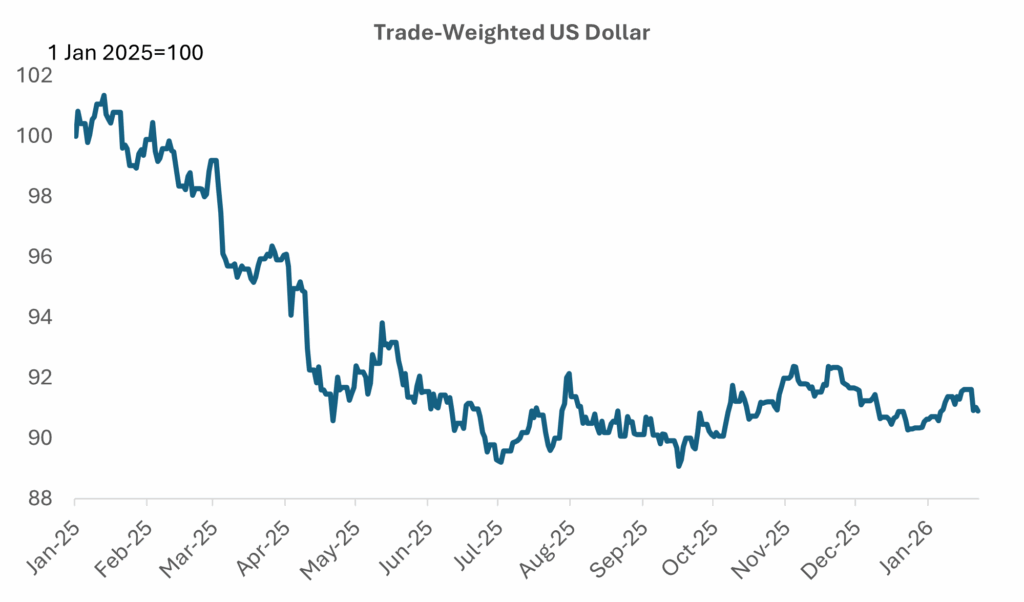

On IMF forecasts most European (and the UK) government debt levels are expected to increase only slightly between now and 2030. The US is a stand-out exception, with the IMF forecasting US debt to GDP to rise by a further 18 percentage points of GDP by 2030. So far, the US government bond market has been relatively stable. However, the weakness of the US dollar over the past year and rise in the gold price indicates not all investors are comfortable with the US government debt trajectory.

More pronounced fiscal expansion, the lagged impact of easier monetary policy in 2025, lower energy prices and increased policy cohesion is expected to drive European growth higher.

Interest payments taking up increasing share of government revenues

Although a potential upset in sovereign bond markets is one of the greatest risks to markets in 2026 in our view, we think the market disruption caused by sustained US government bond selling would likely lead to a resumption of Fed buying of US treasuries and other interventions that would ultimately stabilise markets. The cost of such intervention would likely be further US dollar weakness (and gold price upside).

A number of Trump administration officials have advocated a weak US dollar as a way to boost US export competitiveness and to bring manufacturing back to the US. One of the more notable advocates of a weak US dollar has been Stephen Miran, Chairman of the Council of Economic Advisors under Trump and recently appointed member of the Federal Reserve Board of Governors (A User’s Guide to Restructuring the Global Trading System).

US dollar at risk as debt rises and Fed independence under threat

Therefore, while we think the risk of public market volatility remains elevated, we think private markets investors will remain relatively sheltered. Resilient global economic growth, the continued outperformance of the less-cyclical services sectors that most private markets investors invest in, and tailwinds from easier fiscal and monetary policy should provide a continued supportive investing environment for private market investors in our view.

Corporate balance sheets (in aggregate) remain strong

While aggregate balance sheet and EBITDA trends are solid, idiosyncratic sector and company risks appear to be rising, putting a larger than usual premium on careful investment selection and downside protection.

US growth to remain resilient in 2026 as tax cuts support consumer and business spending, with sustained high government bond yields a negative wild card

Growth support from the lagged impact of tax cuts in last year’s One Big Beautiful Bill Act and still healthy aggregate household and corporate balance sheets should provide growth support in 2026. Non-tech related US business investment and private consumption may continue to be negatively affected by the lagged impact of higher import tariffs on prices and supply chains and sustained high government bond yields. However, we think these potential growth drags will be offset by expansionary fiscal policy, continued strong technology-related investment and spending growth by middle and higher income consumers benefitting from tax cuts and the wealth effect.

Europe will likely see strong performance in 2026

More pronounced fiscal expansion, the lagged impact of easier monetary policy in 2025, lower energy prices and increased policy cohesion is expected to drive growth higher. Although France, Italy and the UK are in the process of reducing fiscal deficits in order to stabilise debt levels, Germany, and most of the rest of Europe are in a position to further expand fiscal policy—with defence and infrastructure two key areas of focus.

Europe has ample space to boost fiscal stimulus

The recent watershed changes in German and EU-wide fiscal policy to allow a significant rise in infrastructure and defence spending, marks a once-in-a-generation shift in fiscal policy. This should provide a medium to long-term boost to Europe’s growth rate – and at the very least provide downside growth protection. More recently, the announcements of the shift in policy led to a discernible improvement in business and consumer sentiment. This shift in policy should help offset any secondary effects from the ongoing global tariff turmoil.

While some companies in manufacturing and industrial sub-sectors may be negatively affected by higher US tariffs (e.g. autos, industrial machinery, chemicals and pharmaceuticals), private markets investors tend to have very limited exposure to these areas—with the bulk of investments in less cyclical services related businesses that are well-insulated from the direct effects of the trade war.

The UK will benefit from falling interest rates and continued positive real income growth

The UK will have to contend with the impact of higher taxes, but healthy household balance sheets, positive real income growth, more aggressive BoE rate cuts, and declining government bond yields should keep a floor under growth and sustain a stable company operating environment in 2026. Although the UK government has been criticized for raising taxes in its latest budget, the move to reduce fiscal deficits and stabilise the country’s long-term debt profile has paid off, helping to further reduce the UK government debt yield premium over equivalent US rates. Lower government bond yields (assuming no further disorderly moves in US and/or Japan government bond markets) should provide further support to household and corporate balance sheets and support growth later in 2026.

Will Trump’s latest tariff threats derail growth?

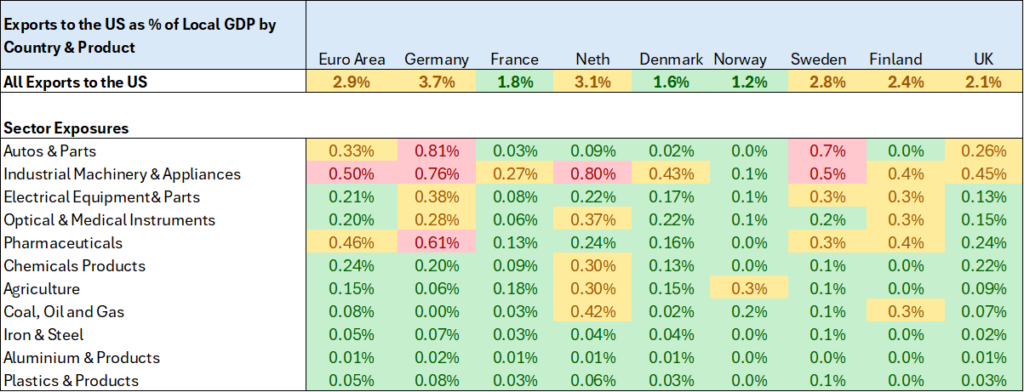

In late January 2026, US President Donald Trump threatened an additional 10% tariff on the imports of eight countries that sent troops to Greenland, including Germany, France, Sweden, Denmark, Norway, Finland, the Netherlands, and the UK. A few days later he retracted the threat. However, fears linger that he may bring tariffs back if he doesn’t get what he wants in Greenland. Therefore, below we present an updated table of the potential target countries and their exposure to the US goods market. As we highlighted in our trade war analyses last year, for most countries in Europe and the UK goods exports to the US are relatively small as a percent of GDP.

Higher US tariffs manageable for most countries

Country and sector exposure to the US market

Therefore, even if the threatened tariffs are implemented, the direct economic impact is likely to be quite small, as was the case when the US imposed tariffs in 2025. Of course, certain sectors such as the auto sector and some segments of the chemical, pharmaceutical and industrial machinery sectors, and US-exposed companies operating in those sectors could be affected. But at a headline GDP growth level the direct impact is estimated to be small, with most estimates putting the impact of an additional 10% tariff on US goods imports from Europe at around 0.1%-0.2% of GDP. If Europe were to retaliate strongly (not our base case), higher domestic costs, supply chain disruptions and potential higher financial market volatility could add to the impact, but our base is that any European response will be calibrated to minimise domestic disruption.

As we highlighted in our trade war analyses last year, for most countries in Europe and the UK goods exports to the US are relatively small as a percent of GDP.

ECB monetary easing should support European growth in 2026

Fiscal and monetary policy will support growth in 2026, but government bond yields are likely to remain high, putting pressure on some companies and households

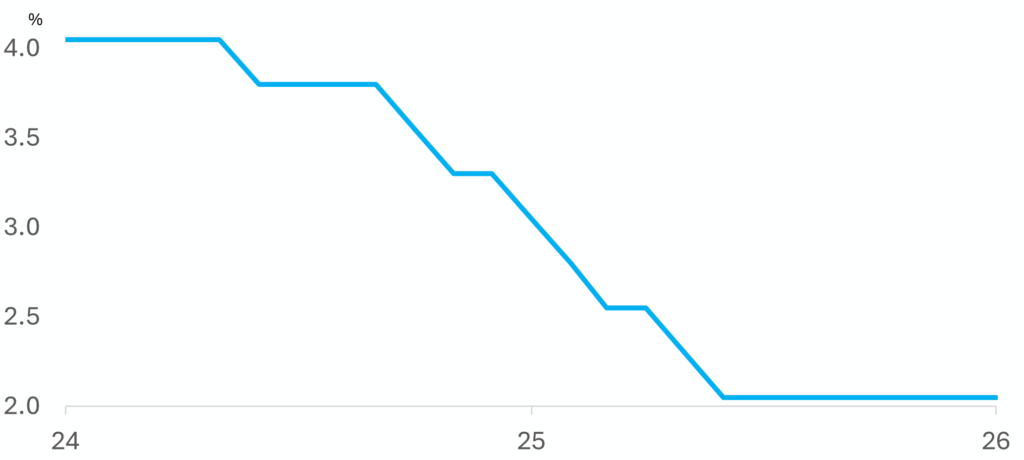

The Fed cut its benchmark interest rate 75bp in 2025. Further rate cuts are likely in the coming months, but perhaps not quite as many as the nearly 100bps swap markets are currently pricing, given the continued stickiness of services inflation and the continued impact of tariff increases on goods prices.

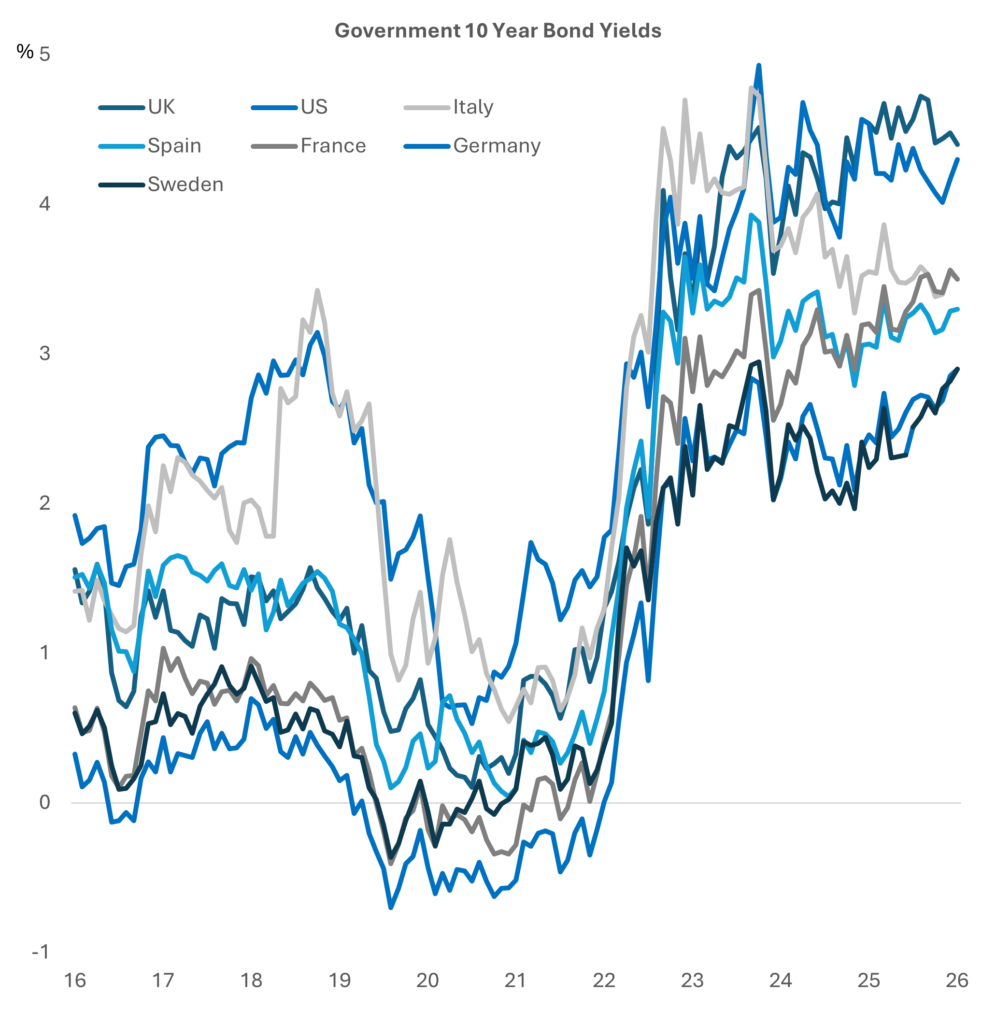

The ECB has been able to cut rates by 200bp over the past year as inflation has moved quickly down to its 2% target. With the ECB’s benchmark rate now at 2%, on our base case that economic growth holds up on more expansionary fiscal policy, lower energy prices and the lagged impact of the past year’s monetary easing, rates are probably at or near bottom.

The BoE, like the Fed, has been grappling with stubbornly sticky services inflation. Despite the stickiness of inflation, it managed to push through 100bps of cuts in 2025. Given the more-fiscally-prudent-than-expected government Budget announced in November, signs of cooling in the labour market and a likely faster decline in inflation later in 2026, larger BoE cuts than the 50bp currently priced into the swaps market for 2026 and a further narrowing of the UK government bond yield premium over equivalent US bonds seem likely.

Government bond yields likely to stay higher for longer

Private company fundamentals remain strong, systemic crisis risks are low, but idiosyncratic risks on the rise

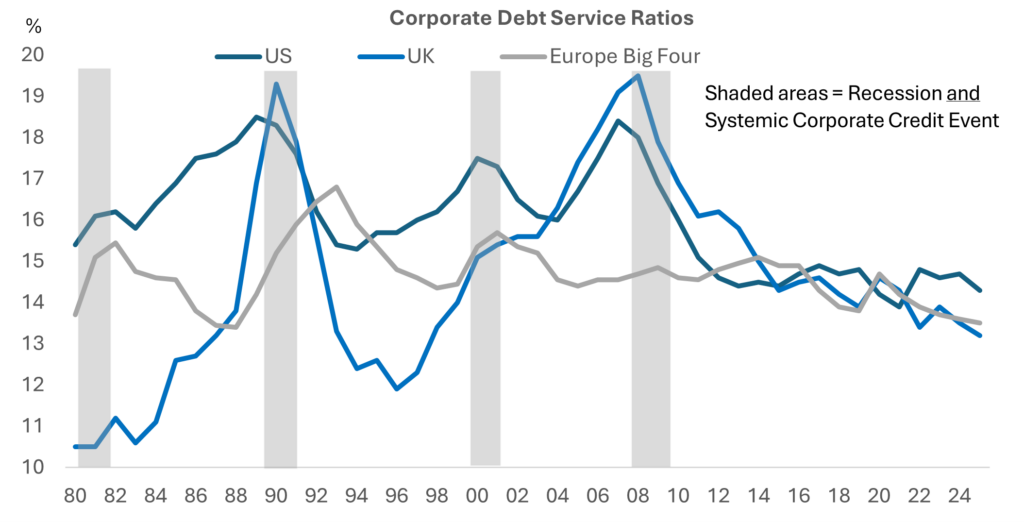

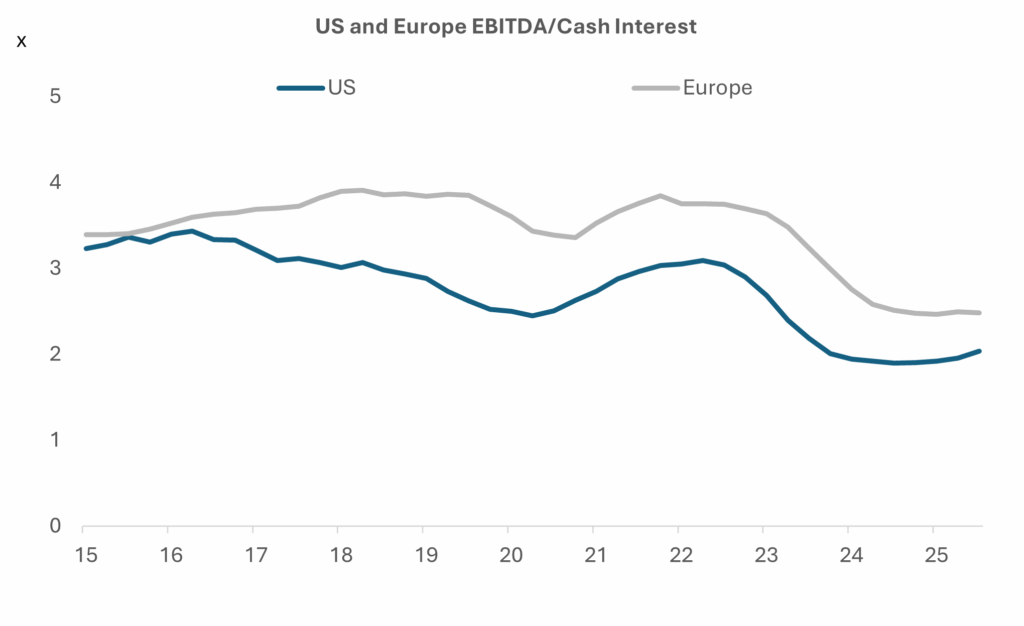

Data from the Bank for International Settlements (BIS) shows that corporate debt service ratios in the US, Europe and the UK are falling and remain well below 2008 levels. On their analysis (Aggregate debt servicing and the limit on private credit), corporate debt service ratios provide ‘highly accurate early warning signals’ for systemic financial crises. On their most recent data this risk appears low (see chart above).

ICG proprietary data also shows relatively healthy private company fundamentals, with median EBITDA growth in the US and Europe (including the UK) holding up well and interest coverage ratios stabilising at comfortable levels on our most recent aggregated data through Q3 2025. While aggregate balance sheet and EBITDA trends are solid, idiosyncratic sector and company risks appear to be rising, putting a larger than usual premium on careful investment selection and downside protection.

Private company fundamentals at an aggregate level remain strong

Implications for private market investors

Given relatively high equity valuations, tight credit spreads and potential risks in major developed economy sovereign bond markets—particularly in the US given its current debt trajectory and concerns about Fed independence—we think the risk of higher for longer, longer maturity government bond yields, volatility in global public markets and further US dollar weakness remain high. Although the risk of market volatility remains elevated, we think private markets investors will remain relatively sheltered. Resilient global economic growth, the continued outperformance of the less-cyclical services sectors that most private markets investors are exposed to, and tailwinds from easier fiscal and monetary policy should provide a continued constructive operating environment for private market investors in our view.

Go deeper

- Follow us on LinkedIn or sign up to our email newsletter to receive notification of future macro and private markets research

- Watch or read ICG CEO & CIO Benoît Durteste’s September 2025 interview on Bloomberg’s Opening Trade, where he commented that Europe has a relatively favourable environment for investment

- Find out about the proprietary ICG Private Company Database, for which the next edition will be available in the coming weeks via the ICG Client Lounge