Base case

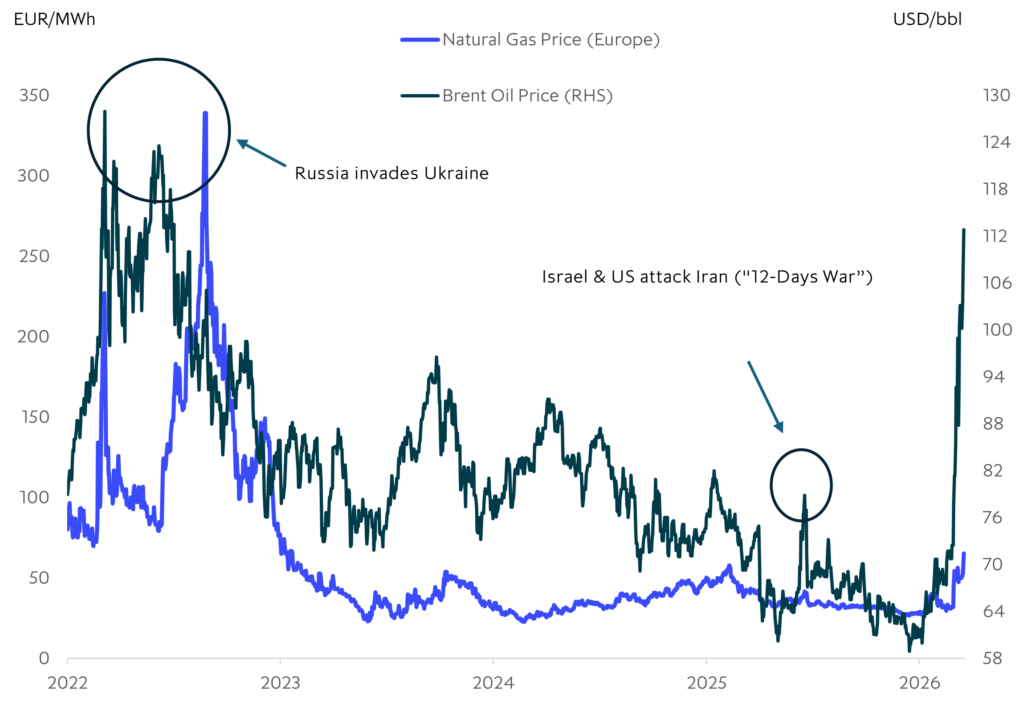

Middle East conflict testing global economy’s resilience

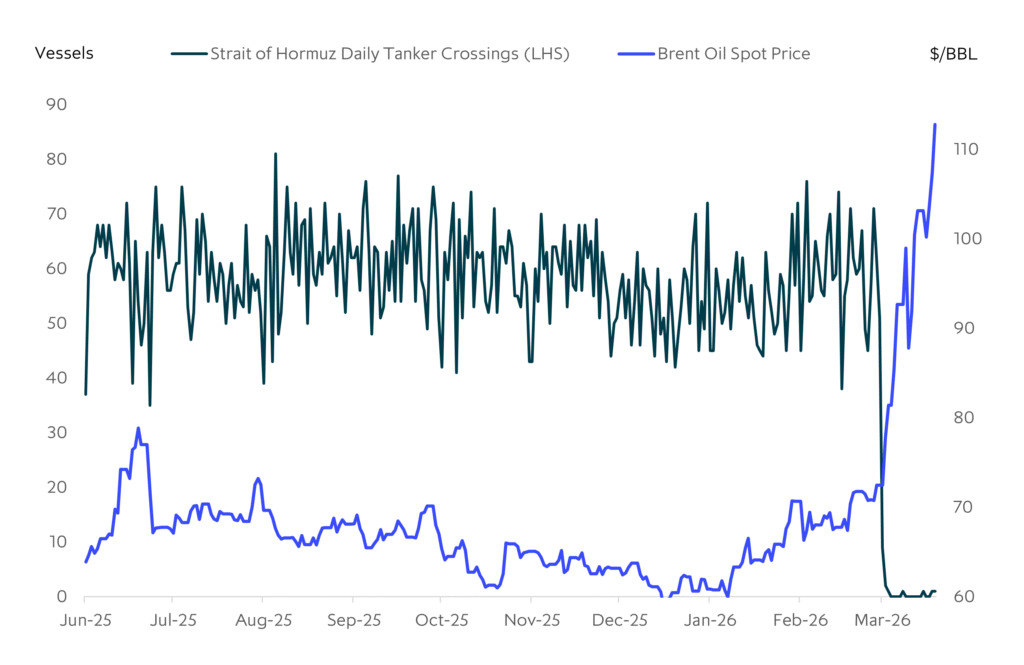

- The ability of the US and partners to quickly restore flows through the Strait of Hormuz is critical and remains uncertain.

- Prolonged disruption to shipping and/or regional production would keep oil and gas prices higher for longer, weighing on global growth and keeping inflation elevated.

- Even in this downside case, we view the probability of a global recession as low with most estimates putting sustained Brent oil price of around $100/bbl taking around 0.5 percentage points off global growth and adding around one percentage point to inflation. But clearly there is a lot of uncertainty and country variation around these estimates.

Macro outlook

Why our base case remains that US/Israel attacks on Iran will be short-lived with limited lasting impact on energy and the macro outlook:

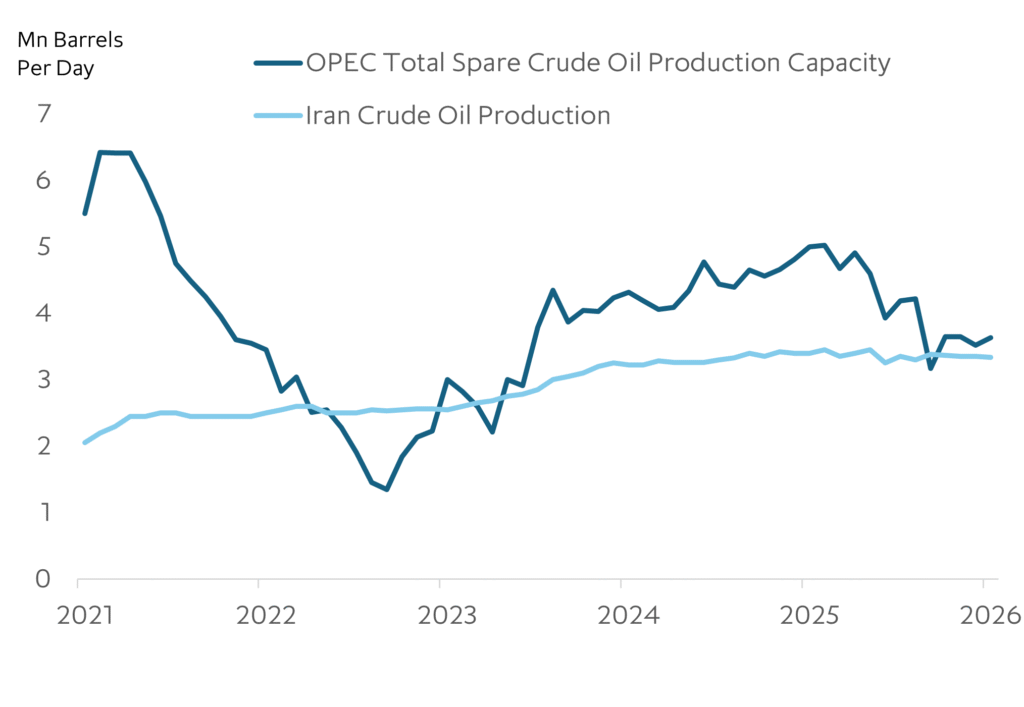

- OPEC has substantial spare capacity (there is not an oil supply problem) and is sufficient to compensate for a full loss of Iran’s oil supply.

- Most public pre-war analyses indicate the US military has the resources, capability and will (once the initial attacks on Iran are complete) to prevent an extended closure of the Straits of Hormuz.

- Trump is laser-focused on not losing the Republican’s congressional majority in the November mid-terms as it would hobble the last two years of his presidency. He will not want to see a sustained rise in oil and gasoline prices that will hurt his popularity with the electorate.

- A prolonged conflict and sustained high energy prices would push inflation higher making it difficult for the Fed to cut interest rates and would likely keep government bond yields high. A sustained rise in energy prices (ie, months rather than weeks) would hurt US and global growth and push unemployment higher.

- This goes against Trump’s key stated goals of bringing down the cost of living and lowering interest rates.

OPEC Production Capacity and Iran Crude Oil Production

Iran’s response

The hardest part of the analysis is assessing Iran’s medium-term response:

On one side of the equation, Iran will want to make the US, Israel and Middle East states supporting the US feel enough pain that they will think twice before attacking again in the future. On this basis there are incentives to keep the Strait of Hormuz closed for an extended period through periodic drone, missile and other attacks on vessels attempting to traverse the Strait.

On the other side of the equation, currently Iran is being allowed to ship oil near pre-war levels and its energy infrastructure has been mostly left intact. A large portion of Iran’s government budget is financed by energy revenues.

For the long-term survival of the current regime they need these revenues. How this balance of priorities and US capacity to unilaterally keep the Strait open play out, will determine how long energy prices stay high and the severity of the damage to the global economy.

Re-opening the Strait of Hormuz key to outlook