Updated on 11 November 2025, adding a video: Why have markets and economies been so resilient and is this likely to continue?; Updated on 3 October 2025, to reflect recent data

Overview

- Despite high geopolitical and trade policy uncertainty, the global economy and markets have remained remarkably resilient so far this year.

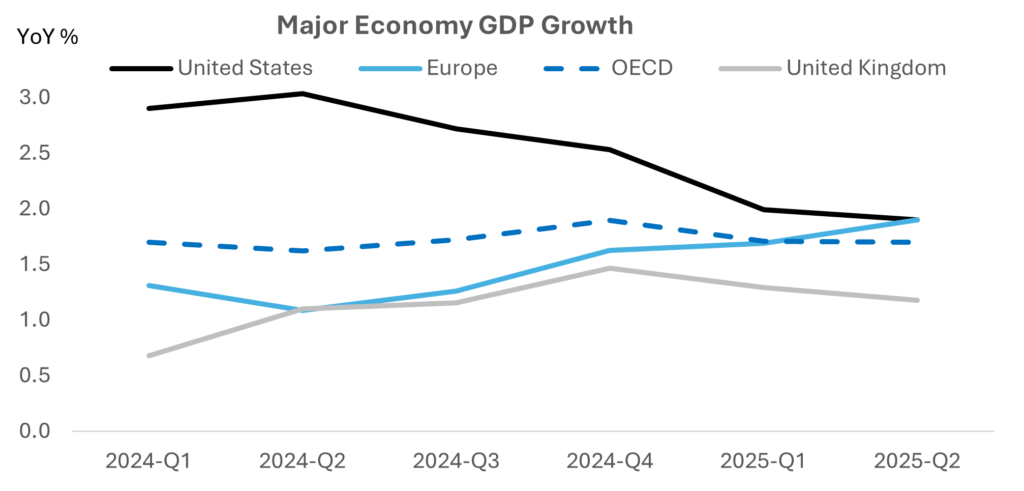

- Against most expectations, developed economy growth in the first half of the year has trended between 1.5% to 2%, in line with its longer-term average, most equity benchmarks are near all-time highs and credit spreads remain tight.

- European and UK growth has proven to be much more resilient than most investors expected, with US import tariffs and policy uncertainty having a much smaller impact on growth than initially feared.

- Although the US economy has been losing momentum, with recently revised US real final sales to private domestic purchasers (a cleaner measure of US growth than GDP which has been distorted by tariff front-running) slowing to 2.4% in the first half of the year from 3.1% in 2H 2024, most lead indicators point to a moderate rather than a precipitous slowdown.

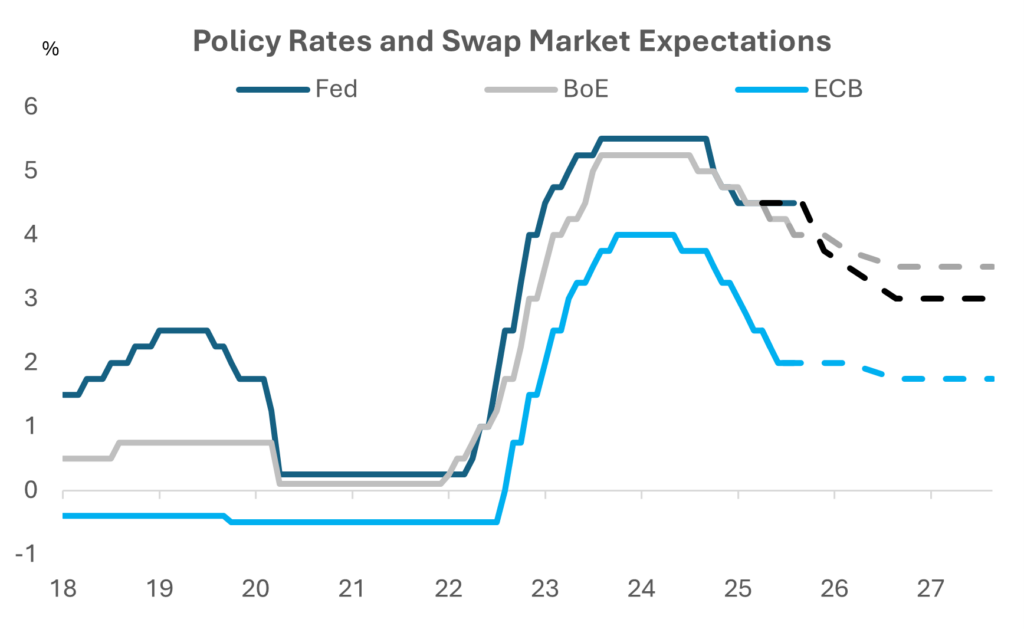

- Monetary policy easing underway, with the Fed resuming rate cuts in September, the ECB having cut its benchmark rate in half over the past year, the BoE expected to start cutting rates again by early next year and China’s central bank also prepared to ease further.

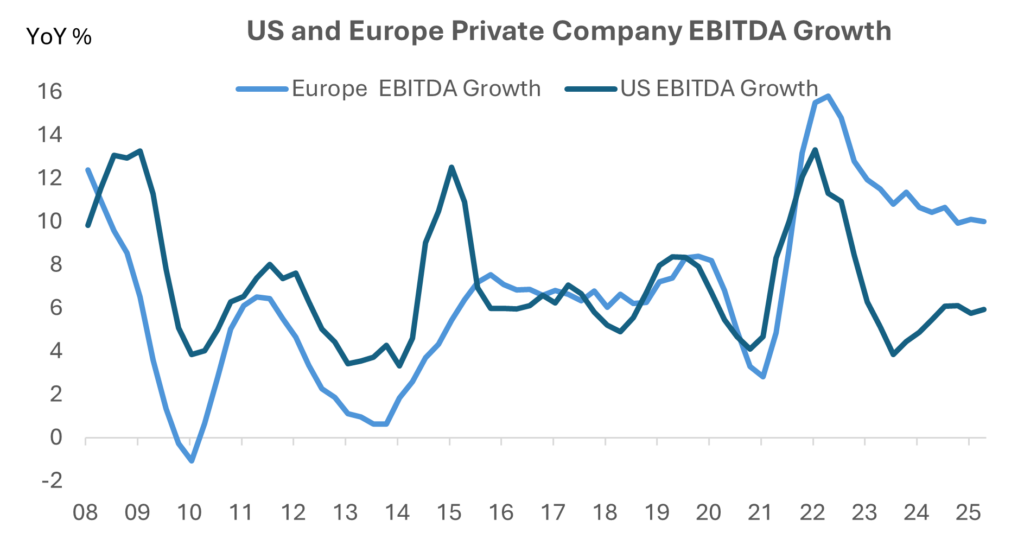

- Private company fundamentals are strong, with ICG proprietary data showing US and Europe private company EBITDA growing at a solid pace through the first half of 2025 (see chart below) and median interest coverage ratios stabilising at comfortable levels.

- The question is whether this resilience will be sustained.

Resilient global growth

Tariff impact more limited than initially feared

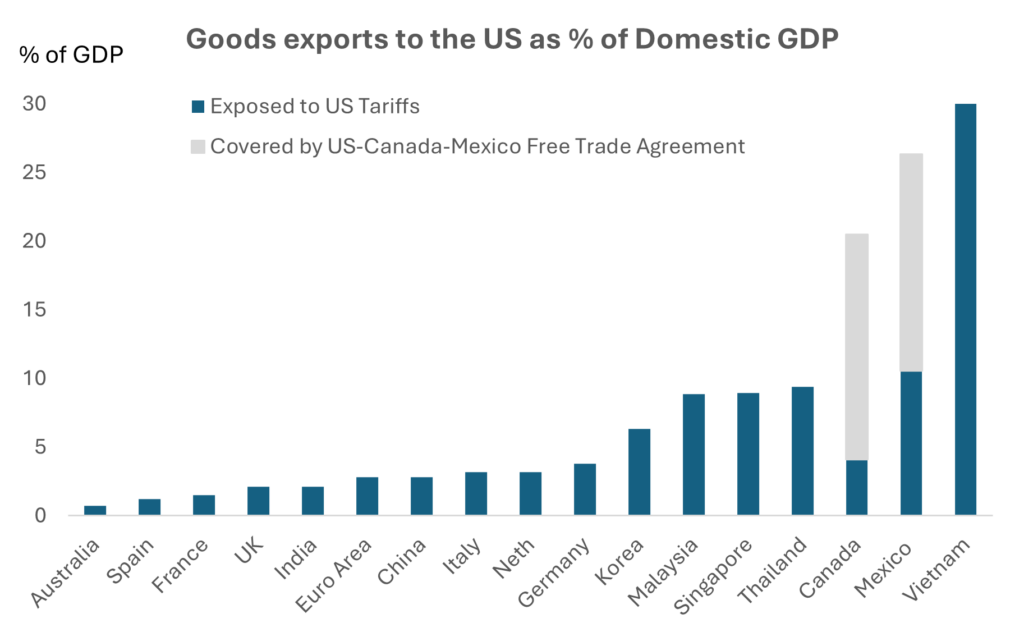

Most major developed market economies should see only limited headline growth damage from the Trump administration’s tariffs, in our view. It remains to be seen exactly where country and sector tariffs end up, though indications are that tariffs for most countries (particularly once carveouts are accounted for) will be much lower than the initial “reciprocal” tariffs announced in early April.

As the chart below shows, most of Europe, the UK and other large, developed economies have only a small direct exposure to the US goods market. Certain sectors such as steel, aluminum, autos, chemicals and potentially pharmaceuticals and semiconductors may see a larger negative impact. But with the services sector making up more than 80% of most developed economies GDP (and where most private markets investors invest), most businesses are expected to see only limited direct impact. The indirect impact through exposures to affected goods exporting companies and potential wider economic disruption will need to be monitored, but bottom-up analyses indicate these effects should be manageable.

US growth is slowing, but not by much so far

We think the US economy is likely to be one of the most negatively affected by the Trump administration’s trade tariffs, with higher across-the-board import costs pressuring company margins and investment capacity and higher goods prices hitting consumers’ real spending power. Higher business and consumer uncertainty may also cause companies and households to hold back on investment and consumption.

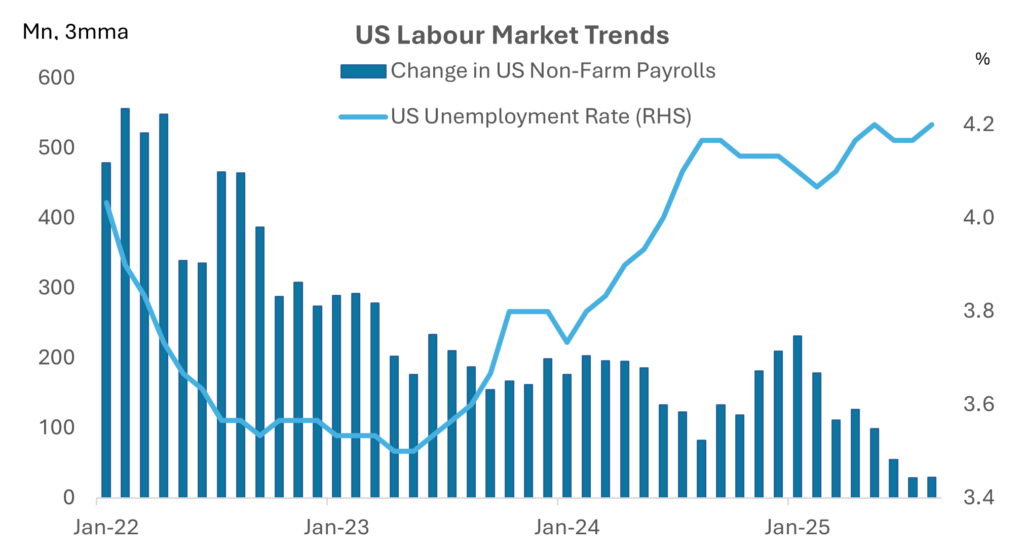

With the US Labour market now appearing to be cooling quite quickly, we think the Fed will start cutting rates more aggressively in the coming months.

US real final sales to private domestic purchasers (a cleaner measure of US growth than GDP which has been distorted by tariff front-running) slowing to 2.4% on a quarterly annualised basis in the first half of the year from 3.1% in 2H 2024, with personal consumption slowing to 1.6% in 1H 2025 from 4.0% in 2H 2024.

Although economic and labour demand growth is slowing, we believe recession risks remain low, with fiscal policy expected to support growth and strong household, bank and corporate balance sheets putting a floor on growth downside.

The Fed is currently forecasting around 1.6% full year GDP growth in 2025 and 1.8% growth in 2026. While recent GDP data revisions indicate growth in 2025 may end up a bit higher than the Fed’s forecast, generally most hard data supports this slower, but relatively resilient growth outlook.

Inflation in the US has been stickier than expected, which has limited the Fed’s ability to lower interest rates, however we think that is now changing. Although tariffs will likely push headline inflation higher, wage and underlying inflation pressures appear to be abating. With the US Labour market now cooling, we think the Fed will be in a position to continue rate cuts in the coming months – though perhaps not quite as quickly as the market is currently pricing.

US labour market is cooling quickly

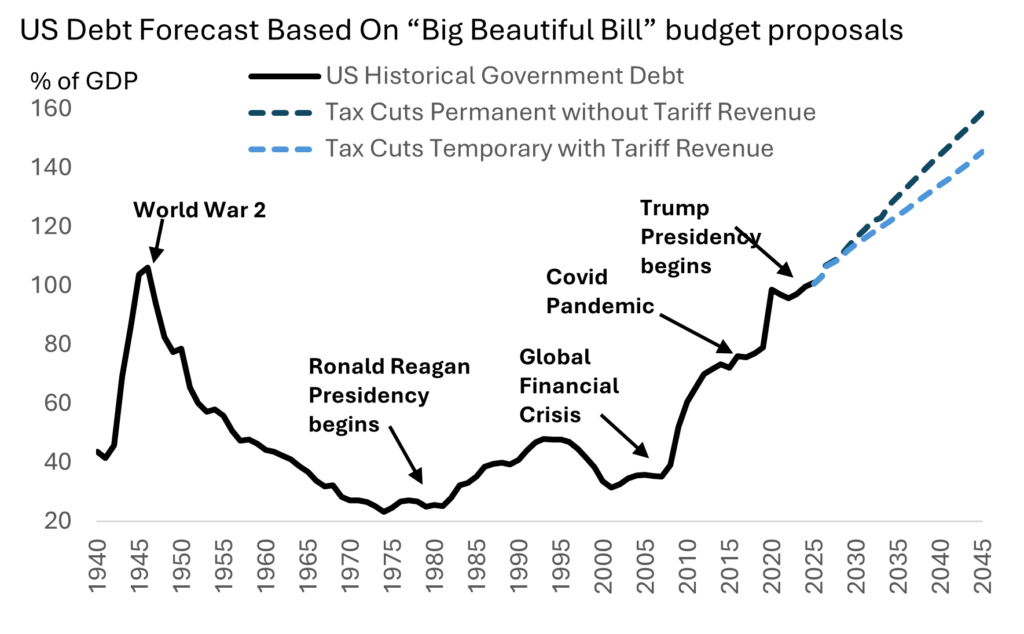

US government debt and US dollar risks continue to simmer in the background

One wild card risk to monitor is a potential disorderly back-up in US government bond yields and faster decline in the US dollar if investors decide US fiscal policy and the government debt trajectory are unsustainable and that Fed independence has been truly compromised. So far, the US government bond market and moves in the US dollar have been relatively orderly, but this could change quickly.

It is likely that a sharp and sustained rise in US government bond yields would be met with aggressive policy intervention by the Fed to stabilise nominal yields. However, quantitative easing into an economy not far off full capacity would likely be viewed by the market as inflationary, pushing down expected US real yields and adding further downward pressure on the dollar.

US government debt risks remain a wild card

Europe to benefit from expansionary fiscal and monetary policy, limited exposure to US goods market

Europe is likely to see the economic recovery that started at the end of 2023 to continue into 2026 and beyond. Changes in German and Europe-wide fiscal policies are expected to provide a medium to long-term fiscal boost to growth and well-behaved inflation allowing the ECB to keep monetary policy easy.

The recent watershed changes in German and EU fiscal policy to allow a significant rise in infrastructure and defence spending, marks a once-in-a-generation shift in fiscal policy. The European Commission estimates that its proposal to exempt defence spending from EU fiscal rules will open the way to a potential additional EUR650bn in new spending over the next four years on top of the proposed EUR150bn Common Borrowing Facility.

In all, on proposals so far, the increase in Europe defence and German infrastructure spending could be as large as EUR1.7trillion, equivalent to around 10% of EU GDP. This should provide a medium to long-term boost to Europe growth – and at the very least provide downside growth protection. This shift in policy may also help offset any potential secondary effects from the ongoing global tariff turmoil.

A pivotal moment for European fiscal policy

With Europe exports to the US equivalent to less than 3% of GDP, the impact of higher US tariffs is expected to have only a limited negative impact on headline economic growth, with most independent estimates putting the one-off hit to growth at between 0.3-0.5% of GDP over two years.

The recent watershed changes in German and EU fiscal policy to allow a significant rise in infrastructure and defence spending, marks a once-in-a-generation shift in fiscal policy.

The ECB has been well ahead of the curve, cutting interest rates by 200 basis points over the past year as inflation has neared its 2% medium-term target. While we think the ECB is largely done with rate cuts, we think the lagged impact of monetary easing will help support economic growth as we move in 2026.

Interest rate cuts ahead

Political stalemate in France likely to drag on, but limited impact on real economy expected

A vote of no confidence in the government forced French Prime Minister Bayrou to resign in early September. President Macron appointed ally and former defence minister Sebastien Lecornu as the new prime minister, tasked with cobbling together sufficient votes to pass the 2026 budget by year-end.

While the political noise level is high, neither the extreme right or left have sufficient votes to implement their respective agendas. Therefore, the most likely scenario is continued muddle through, with government policy staying mostly on autopilot and the fiscal deficit remaining in the 4.5-5.5% of GDP region until new presidential elections are held (likely in 2027).

Although policy gridlock may limit the upside potential of France’s economy, it also means damaging extremist policies will not be implemented. Recent business surveys indicate company executives continue to see a positive operating environment into the third quarter, with economic growth likely to continue to trend in the 0.5%-1% range.

The markets have taken recent political developments in stride, with French government bond yields declining and the stock market rising in the run-up to and after the vote.

Although policy gridlock may limit the upside potential of France’s economy, it also means damaging extremist policies will not be implemented.

UK to see limited negative impact from trade war, but policy constraints limit near-term growth upside

With only around 2% of UK GDP exposed to the US goods export market, the UK is likely to see a relatively small negative impact from US tariffs. However, fiscal constraints and sticky inflation give policymakers less leeway to support growth than in Europe. Therefore, while GDP growth in 2025 is expected to remain positive, it is likely to slow to around 1% in 2H 2025 after growing 1.6% in the first half of the year.

Lower interest rates in 2026 as inflation starts to fall again later in 2025 and continued strong real household income growth should help support a pick-up in growth in 2026 and into 2027. Consensus forecasts are for around 1.2% GDP growth in 2025, 1.4% in 2026 and longer-term growth of around 1.5%.

China and developed Asia holding up well

China growth has held up much better than many expected, with GDP currently on track to meet the government’s target of 5% this year.

China’s direct exports to the US are equivalent to less than 3% of GDP and estimates are that China production in third countries sent to the US are less than 2% of GDP. While this is not insignificant and will have an impact on specific sectors and companies, the overall impact on China’s economy is expected to be manageable. In addition, China has substantial fiscal and monetary firepower to support growth if needed.

China growth has held up much better than many expected, with GDP currently on track to meet the government’s target of 5% this year.

Developed Asia is experiencing a similar dynamic. While specific sectors and companies will likely be negatively affected, the rise of domestic demand – and services in particular – as a key driver of economic growth, has reduced these countries vulnerability to higher US import tariffs.

Implications for private markets investors

Overall, we think the macro context described above provides a constructive environment for private markets investors. While the risk of public market volatility remains elevated, with think private markets investors will remain relatively sheltered. In the first half of 2025, the around 400 companies in the US, Europe and the UK tracked by the ICG database saw median EBITDA grow at a solid pace (see chart below). Slower, but still resilient economic growth, the continued outperformance of the less-cyclical services sectors that most private markets investors are exposed to, and tailwinds from lower interest rates should continue to provide a positive investing environment for private markets investors through the rest of 2025 and into 2026 in our view.

Private company EBITDA growth has remained firm

Watch video

Why have markets and economies been so resilient and is this likely to continue?

In this short film recorded on 29 October 2025, Nick assesses current structural macro and credit market fundamentals, key risks to the outlook and what current conditions may mean for investors broadly and private markets investors in particular.