- The proposed US-EU trade deal announced 27 July was better than expected and will help reduce policy uncertainty and downside risks to Europe growth. Although there are still a number of details to be worked out and a legally binding text still needs to be agreed upon, the announced policies give much-needed clarity to the likely landing point of the final agreement.

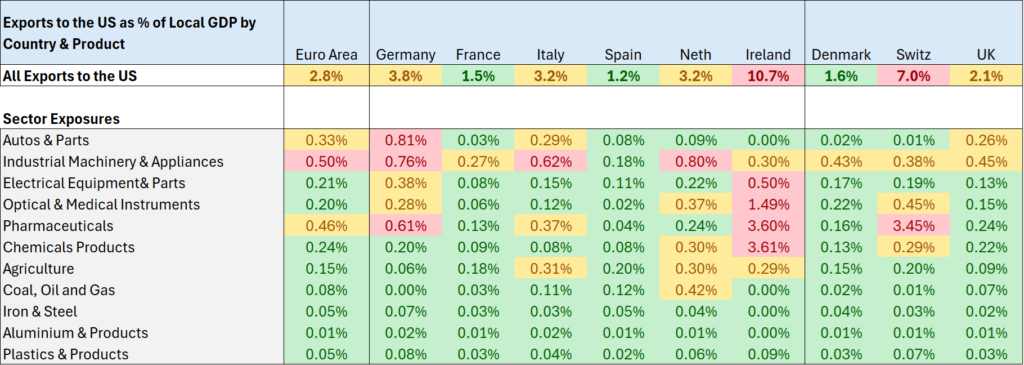

- The announced 15% tariff on most EU exports to the US is expected to have minimal negative impact on EU GDP growth. EU goods exports to the US are equivalent to less than 3% of EU GDP and the bulk of Europe’s economic activity is in the service sector (see table below).

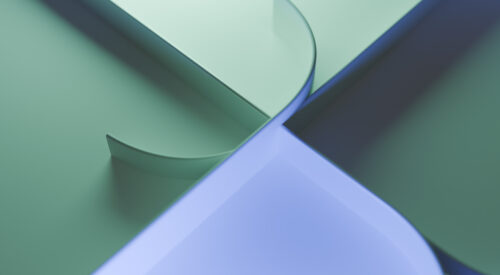

- Based on data from the ICG Private Company Database, most private markets investments are focused in services businesses which are not directly affected by US import tariffs, limiting the impact of US trade tariffs on private markets investors (see chart below).

- Most independent estimates put the one-off hit to the EU economy from the trade tariffs at around 0.3%-0.5% of GDP, with Germany seeing a larger hit, France and Italy seeing a more limited impact and Spain seeing little to no impact (see table below for individual country and sector exposures). The impact is expected to be highly sector specific (e.g. the automotive, chemicals, metals and parts of pharma sectors, with most other sectors unscathed).

Mild growth impact, with US most negatively affected

The negative impact of higher global tariffs on the US economy is estimated to be larger than the impact on the EU, with most estimates putting the hit to the US economy at around 1% of GDP and the (likely one-off) boost to US headline inflation around 1.5% percentage points above where it would be without the announced tariffs.

With the overall impact of the tariffs on EU growth expected to be relatively small, the more critical implications for investors are at the sector level where there are some large divergences in exposures (and still some unresolved issues).

Europe economic recovery to resume after brief lull

Under the agreement as first announced, most goods exports from the EU to the US will see a 15% tariff rate. This is up from an average of around 2% pre-Trump’s inauguration. Although a large increase, most sectors exposures to the US goods market are low (see table below).

The proposed US-EU trade deal announced 27 July was better than expected and will help reduce policy uncertainty and downside risks to Europe growth.

Automotive sector likely to remain under pressure

Automotive imports will see their tariff level fall to 15% from the rate of 25% announced in April. However, with tariffs still much higher than the pre-Trump rate of 2.5%, Europe’s automotive sector (along with much of the rest of the world’s auto sectors) will likely remain under pressure.

Pharmaceuticals still awaiting conclusion of US Section 232 investigation

Many pharmaceutical exports will also incur a 15% tariff to access the US market (though certain generic drugs will be excluded and the timing of implementation is still unclear). While this is lower than the up to 200% tariffs Trump threatened earlier this year, it will represent a hit to EU pharmaceutical exporters historically used to 0% tariff access to the US market. There is also still uncertainty about whether a higher tariff rate may be implemented further down the line once the US Section 232 investigation by the US Department of Commerce into pharmaceutical imports (with a focus on concerns of over-dependency on foreign supplies of critical medicines and ingredients) is completed.

Semiconductor manufacturing equipment to remain tariff-free

Semiconductors are also included as part of the agreement and will be covered by the 15% tariff rate according to European Commission president Von der Leyen. As with pharmaceuticals, while this is lower than previously threatened rates, it is a large rise from their previous tariff-exempt status, and it is still unclear whether a higher rate will be imposed at the conclusion of the ongoing 232 investigation. Although details are not yet available, it appears semiconductor manufacturing equipment will be excluded from the new tariffs as will aircraft and component parts.

Steel and aluminium exporters may benefit from a new quota system

Steel and aluminium tariffs will stay at 50% for now but it was agreed that a quota system would be implemented that will allow a certain amount of the metals to be sent to the US at a lower tariff rate.

Other EU sectors with relatively large exposures to the US market that may be negatively affected by the 15% tariff rate are industrial machinery and appliances, optical and medical instruments, chemicals and some agricultural products. However, outside of these areas EU exposure to the US goods market is small relative to GDP.

Most private markets investments are focused in services businesses which are not directly affected by US import tariffs, limiting the impact of US trade tariffs on private markets investors.

Therefore, while the proposed US-EU trade agreement will have a disruptive effect on certain sectors and companies, the broader macroeconomic impact is expected to be small.

Resilient European growth

Looking forward, we think after a brief lull in growth over the next quarter or so, Europe growth will rebound and resume the growth recovery that began in late 2023 (see chart below). While we do not expect a strong V-shaped recovery, we think European growth remains solidly supported, providing a continued constructive investing environment.

The announced 15% tariff on most EU exports to the US is expected to have minimal negative impact on EU GDP growth. EU goods exports to the US are equivalent to less than 3% of EU GDP and the bulk of Europe’s economic activity is in the service sector.

A supportive growth environment across most of Europe

Strong private sector balance sheets, fiscal and monetary expansion to provide a continued constructive investing environment

Strong household and company balance sheets, rising real incomes, easing monetary policy and –significantly – a watershed shift towards a more expansionary fiscal policy should, in our view, provide downside protection to European growth and support private company fundamentals going forward. As always, bottom-up sector and company selection will be critical as tariffs and shifting global macro policies increase performance dispersion. For a broader macro view of the global consequences of the trade war please click here: Trade War Views: Implications for the Economic Outlook and Business Operating Environment.

Europe economic exposure to US tariffs is low, with a few vulnerable sectors

ICG Private Company Database: Limited private markets exposure to sectors affected by US tariffs